Will Bell’s 300MW AI Campus Redefine Canada’s Data Center Market?

Pre-leased demand, sovereign alignment, and power access converge to redefine how AI data centers are underwritten, financed, and positioned in developed markets

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Bell’s 300MW AI campus in Canada is not about scale but about sequencing how AI infrastructure is built, funded, and governed.

The project is fully pre-committed, with CoreWeave and Cerebras taking all capacity, while Bell provides infrastructure and national positioning.

Canada is the test case, and if this model holds, it could reshape how investors evaluate data center opportunities across developed markets.

Canada as a Structuring Environment

Canada’s relevance is less about traditional colocation demand and more about aligning infrastructure with national priorities while attracting global compute operators.

Saskatchewan offers what constrained U.S. and European markets cannot: scalable power with a clear path to expansion.

This allows for a different approach to underwriting, where developers anchor projects in manageable supply areas instead of chasing saturated demand hubs.

Canada emerges as a controlled environment for large-scale AI infrastructure, providing regulatory clarity and strategic flexibility.

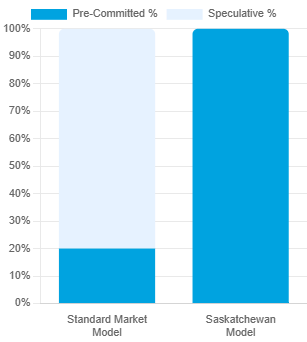

Demand Is No Longer Assumed. It Is Contracted.

The full pre-commitment of 300MW shifts underwriting, starting with secured utilization rather than speculative absorption.

CoreWeave brings GPU-driven workloads, while Cerebras delivers a distinct architecture for large-scale training and inference.

This ensures immediate load certainty and changes the infrastructure model. Assets are now built to meet contracted demand, not to attract tenants.

The approach reduces early cash flow volatility and lets capital providers evaluate performance based on contracts rather than forecasts, creating a more stable investment framework.

Capital Enters at a Different Point in the Lifecycle

Committed tenants change how capital is deployed in AI infrastructure projects. In prior cycles, institutional investors waited for stabilization, while development capital carried higher risk and demanded higher returns.

With demand secured upfront, development-stage assets start to resemble stabilized infrastructure, compressing the traditional risk premium of construction and lease-up phases.

This shifts the timing of capital participation, allowing infrastructure investors to engage earlier if demand is verifiable and counterparties are credible.

As a result, the gap between development and institutional ownership narrows, creating a more continuous and predictable investment lifecycle.

Tenant Composition Is a Strategic Variable

The pairing of CoreWeave and Cerebras is deliberate, not interchangeable.

CoreWeave drives broad GPU-based AI demand across training, inference, and enterprise workloads, while Cerebras focuses on large-scale model efficiency with wafer-scale architecture.

This mix creates a resilient demand profile, combining breadth and depth. One tenant delivers volume, the other specialized throughput, reducing reliance on a single demand type.

For investors, tenant composition is a key underwriting factor, influencing how capacity is allocated and utilized over time, beyond just tenant creditworthiness.

Sovereign Capacity Introduces a Parallel Demand Layer

Part of the campus is dedicated to domestic users needing in-country processing and regulatory compliance, creating a second demand channel alongside commercial workloads.

Government agencies, research institutions, and regulated enterprises are less price-sensitive, more stability-focused, and aligned with policy objectives.

Integrating this sovereign layer provides structural advantages, broadening the customer base, reducing exposure to commercial cycles, and embedding national priorities into the asset.

Power Determines Feasibility

Site selection is driven by energy availability, not geographic proximity. Saskatchewan can support 300MW with room to expand, a capability rare in mature data center markets.

AI workloads intensify the demand, requiring reliable, predictable power for high-density racks and sustained compute loads.

Underwriting must focus on power delivery, interconnection certainty, and long-term energy sourcing. Power is not just a line item it is the core determinant of feasibility.

The Economic Center of Gravity Has Shifted

The financial scale of the project extends beyond the infrastructure itself.

The compute equipment deployed within the campus is expected to represent a significantly larger capital base than the physical facility. GPUs, wafer-scale systems, and associated hardware dominate the total investment.

This redefines the hierarchy of value.

The data center becomes the enabling layer for a higher-value compute ecosystem. Its role is to provide the environment in which that capital can operate efficiently.

For investors, this introduces a layered exposure. Infrastructure returns are tied to the performance of assets that sit above them in the stack.

This inversion where compute capital outweighs the physical asset aligns with the broader stack shift described in Meta’s $135B Capex Signal: Ads Are Becoming an Infrastructure Product.

Competitive Positioning Is Defined by Access, Not Capital

The competitive landscape is shifting from capital availability to control over scarce inputs. Power access, policy alignment, and early tenant commitment now determine which projects advance and which stall.

Capital remains necessary, but it is no longer a source of differentiation. Once demand and infrastructure inputs are secured, financing follows with relative ease.

As a result, competition is being redefined. The advantage now lies in positioning securing power, aligning with policy, and locking in tenants early rather than simply deploying capital at scale.

This shift from capital-led competition to input control is consistent with the structural dynamics explored in What Most Investors Misprice in Data Centers.

The Takeaway

Bell’s 300MW Saskatchewan campus highlights sequencing over geography, showing that Canada’s role is strategic, not simply about location.

AI infrastructure is shifting to demand-secured, power-constrained, and policy-aligned models, with tenants committing earlier and reshaping when and how capital enters the market.

Canada sets the template, and if successful, the model could expand to other aligned markets. Early engagement brings risk but offers strategic advantages in pricing, positioning, and governance.

Timing is no longer secondary; it has become the primary strategic variable for AI infrastructure investment.