Meta’s $135B Capex Signal: Ads Are Becoming an Infrastructure Product

How AI, Power, and Gigawatt-Scale Compute Are Transforming Advertising into a Capital-Intensive Infrastructure Business

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Meta’s Q4 2025 results were strong: $59.9B in revenue (+24% YoY), $8.88 EPS (+11%), and $22.8B in net income. Family Daily Active People rose to 3.58B (+7%), while ad impressions climbed 18% and pricing increased 6%, showing AI-driven targeting is lifting both volume and yield.

But the bigger signal was guidance.

Meta projected $115–$135B in 2026 capex, up from $72.2B in 2025 marking a shift toward becoming one of the world’s most capital-intensive AI infrastructure builders, while still expecting operating income to grow year over year.

The Advertising Engine: Industrialized by AI

Family of Apps remains one of the most profitable systems in tech, generating nearly all of Meta’s Q4 revenue and helping drive $115.8B in operating cash flow for 2025.

That liquidity allows the company to fund its AI expansion largely without relying on external capital.

What’s changed is AI’s role inside the ad stack. Model unification, ranking upgrades, and automated creative tools are no longer incremental tweaks. They’re system-level multipliers. Even small gains in prediction accuracy now flow through the funnel, lifting click-through, conversions, and pricing power.

The result is that Meta’s ad platform increasingly behaves like a high-performance compute engine rather than a traditional media marketplace. AI isn’t just enhancing ads, it is compounding monetization at global scale.

Margin Compression as Deliberate Reinvestment

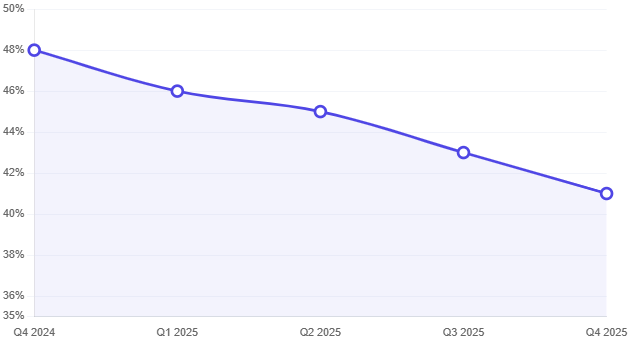

Operating margin compressed to 41% in Q4 from 48% a year earlier, as total costs rose 40% year-over-year. The largest drivers were infrastructure expansion and AI technical talent. This compression should not be read as erosion. It is conversion.

Meta is deliberately redirecting free cash flow into physical capacity data centers, silicon, networking, and power commitments.

In 2025 alone, the company deployed $72.2B in capex. The 2026 midpoint guide of $125B represents one of the largest single-year capex programs in corporate history.

At this scale, infrastructure becomes the strategy.

Capex as Competitive Moat

Meta’s capex plan is focused on massive capacity expansion. Reports cite gigawatt-scale clusters, including a 1GW “Prometheus” in Ohio for 2026 and a ~1GW Indiana campus costing ~$10B projects that resemble mid-sized utilities more than server farms.

To support this, Meta has secured critical long-lead inputs: a $6B multi-year fiber agreement with Corning through 2030 and multi-billion-dollar third-party GPU deals to manage training demand while internal clusters come online.

The pattern is clear. Competitive advantage in AI is being determined by secured power, deployed compute, and network throughput. Meta is locking each of those variables simultaneously.

Emerging Markets: Monetization Density Over Expansion

Meta’s emerging market strategy is no longer about user acquisition. Distribution is already embedded across WhatsApp and Instagram in high-growth regions. The opportunity is monetization density.

AI-driven automation allows Meta to profitably serve long-tail SMB advertisers in markets where manual campaign management would be cost-prohibitive. As ranking models improve and creative tools automate production, incremental advertisers can be onboarded at lower marginal cost.

Infrastructure investment drives this strategy: as AI inference spreads across messaging, commerce, and recommendations, latency and capacity are critical in emerging markets. Capex not only protects U.S. ad yield but also enables global monetization growth without compromising user experience.

Reality Labs: A Managed Optionality

Reality Labs continues to post heavy losses, with $955 million in Q4 revenue against a $6.0 billion operating loss and full-year 2025 losses of $19.2 billion pushing cumulative losses since 2020 past $80 billion. Management expects 2026 losses to remain similar, signaling stabilization rather than escalation.

The focus has shifted: new capital now targets AI infrastructure for the core ad business, not metaverse expansion. Workforce cuts and studio closures show tighter discipline, while AI-enabled wearables are the nearer-term commercialization priority.

In portfolio terms, Reality Labs is a long-duration option. Losses are contained, and upside depends on potential AI-native interface adoption. It no longer drives Meta’s capital thesis but sits alongside the broader infrastructure-focused AI strategy.

Balance Sheet and Capital Structure Implications

Meta ended 2025 with $81.6B in cash and marketable securities and $58.7B in long-term debt, after issuing nearly $30B in new debt during Q4. Free cash flow declined to $43.6B for the year due to elevated capex, but operating cash flow remained robust at $115.8B.

The balance sheet remains strong, but leverage is rising as infrastructure intensity increases. Meta is clearly comfortable augmenting internal cash generation with debt to accelerate buildout timelines. This is a strategic shift from historical conservatism toward capital structure optimization.

The Strategic Inflection

Meta is pivoting from a high-margin digital advertising company to a vertically integrated AI infrastructure platform monetized through ads. The thesis is simple: better AI models improve ad performance, higher-performing ads drive pricing and engagement, and increased monetization funds more compute, creating a self-reinforcing cycle.

Whether this delivers supra-normal returns depends on execution and regulatory stability, but the strategy is clear. Meta is betting that controlling the full stack from models to infrastructure will give it advantages competitors can’t easily match.

At hyperscale, advertising is now an industrial output constrained by compute, power, and network. Meta is internalizing control over these constraints, positioning itself to capture the full value of AI-driven ads at global scale.

The framing of capex as a competitive moat is the right one, but there's a second-order effect that gets overlooked: every dollar Meta commits to gigawatt-scale clusters flows through a finite supply chain — specifically ASML EUV lithography, TSMC advanced nodes, and CoWoS substrate capacity. Meta's $6B Corning fiber deal is a leading indicator of how far downstream these commitments reach. For investors, the more interesting play isn't Meta itself but what this $125B midpoint guidance means for the equipment cycle in 2026–2027: tool orders at AMAT, LRCX, and KLAC tend to lead the buildout by 12–18 months, and that cycle is already in motion. Does the piece's thesis change if the energy constraint (Prometheus Ohio 1GW cluster) turns out to be the binding bottleneck rather than compute capacity?

The part about infrastructure becoming the strategy hits differently when you've experienced even tiny versions of this.

I burned through five hosting providers on my first app before I realized the infrastructure problem wasn't something I could optimize around, it was the bottleneck. That experience completely reshaped how I think about deployment costs.

Seeing Meta convert margin into compute capacity at $135B scale is wild, but the underlying logic tracks: when your competitive advantage depends on model performance, infrastructure stops being a cost center and becomes the moat itself.