Water Constraints: The Underwriting Risk AI Infrastructure Can’t Outrun

Cooling architecture, water-stressed siting, permit risk, basin-level underwriting, AI-grade thermal density, capital impairment

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Water is becoming a growing constraint on AI-grade data center investment.

The old paradigm ranked power first. Fiber second. Water last, if at all.

Capital deployed on that ranking can meet permit refusals, stranded sites, and valuation discounts that did not exist three years ago.

The Shift Is Structural

AI workloads cluster where the power is cheap and the land is permittable. The same map applies to water stress.

A significant share of recently sited AI campuses now sit in basins where water competition is already acute.

Capital is moving regardless, with multi-hundred-billion-dollar buildouts underway in water-stressed regions.

The question is no longer whether water belongs in underwriting.

The question is whether your model is sized for the consequences of getting it wrong. Most are not. And the discipline gap is opening fast.

Water belongs in underwriting now. The question is whether your model can absorb the cost of error. Most cannot, and the discipline gap, mapped across the five constraints that decide every data center site, is widening fast.

The Physics Are Simple. The Footprint Is Not.

Evaporative cooling has been the cheap workaround because it compresses power usage effectiveness (PUE) ratios.

So you trade water for power.

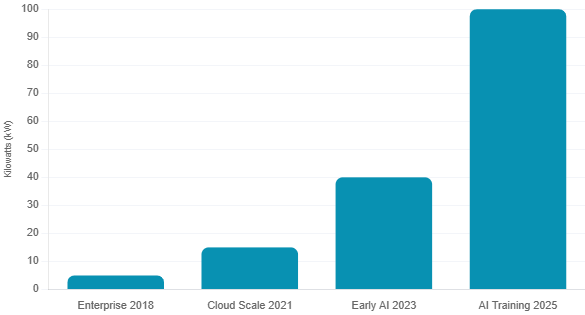

At AI-grade rack densities, the water draw is substantial.

Rack densities have moved from 5 to 15 kilowatts in the legacy enterprise era to multiples of that for AI training clusters.

The thermal physics no longer work with air alone.

The direct draw is the obvious part. The indirect footprint is what most investors miss.

Thermoelectric power generation uses water in its own cooling cycle. So at the basin level, your hydrological exposure is your own withdrawal plus the share embedded in your grid supply.

Basin regulators are starting to count both. Investors should too.

A hyperscale project in a secondary US market was site-pinned for power. The land was secured. The grid interconnect was secured. Mid-construction, the regional utility refused to expand its water withdrawal.

The cooling stack had to be redesigned. Commissioning slipped by more than a year.

The indirect grid exposure was the leverage the developer had not modeled. And it was the leverage that broke the deal.

Water Has Stopped Being a Line Item

The industry has long assumed water was a manageable operating cost. Scaled with electricity. Absorbed at municipal rates. A line item in the model.

That assumption held when racks ran at 5 to 15 kilowatts and tower draws were small relative to local supply. It may not hold now.

AI-grade rack densities push thermal loads past the threshold where evaporative cooling at scale becomes politically and regulatorily costly.

The math that worked for a 10-megawatt enterprise facility does not scale to a 500-megawatt AI campus.

State legislatures across the US are introducing bills that require water disclosure, restrict large water users, and tie tax abatements to cooling architecture.

Federal legislation is following. The European Union is already binding. So the regulatory floor is rising, and it is rising in every major market at once.

Water has stopped being a line item. It has become a permit veto. And in a growing number of basins, it has become a deal-killer.

The Friction Is Time. Not Cost.

Liquid cooling components have lead times measured in quarters. Immersion infrastructure, the same. Qualified mechanical contractors, the same.

So you can write the check. You cannot accelerate the calendar.

Permitting compresses the window further. Community engagement compresses it more. And once a basin organizes around opposition, the political cost of approval rises faster than the operator’s ability to negotiate.

A regional operator secured land, power, and fiber for a flagship AI campus. Late in the permitting cycle, the host municipality refused to approve the projected water withdrawal.

The redesign added more than a year to commissioning. The cooling stack got rebid at higher capex. The tenant LOIs slipped.

Reclaimed water infrastructure requires utility coordination that was usually not in scope when the site was selected.

Municipal treatment plants are not engineered to handle high-mineral data center blowdown. So you co-invest in dedicated industrial reuse infrastructure. A procurement question becomes a multi-year capital project.

Three Lenses on Basin Exposure

Independent operators face the cooling specification problem first.

The choice between evaporative, direct-to-chip liquid, and immersion architectures binds the asset for its operational life. Water Usage Effectiveness (WUE) is fixed at design.

The retrofit path from evaporative to closed loop is technically possible. Almost never economic.

If you chose evaporative cooling in 2022 for 2025 delivery, your asset is now structurally less competitive for AI tenants than liquid cooled peers. Retrofitting requires major capex which competitors are instead deploying into new greenfield builds.

Tenant LOIs for AI workloads now ask for liquid cooling specifications upfront. If you cannot deliver, you cannot bid. The operator without a liquid path is competing on the secondary market for legacy enterprise workloads.

For private equity and infrastructure investors, basin exposure can become a decisive underwriting variable.

Site selection filters that rank power and fiber over water stress can produce IRR-impairing surprises late in the development lifecycle. Capital is already committed.

Exit is conditional on commissioning. So schedule risk from permitting and community opposition can compress fund-level returns by 200 to 400 basis points on affected assets.

Development debt sized to a commissioning date that water risk pushes out 12 to 24 months creates covenant stress the original capital structure never contemplated.

For public equity investors, valuation dispersion is opening. Operators with verifiable cooling transitions and reclaimed water agreements on one side. Operators concentrated in evaporative legacy assets in stressed basins on the other.

The EU disclosure framework is binding. The US is legislating toward it. The repricing will not be subtle.

For public equity, dispersion is already opening between operators with liquid cooling and reclaimed water rights, and those stuck in evaporative legacy stock in stressed basins. With EU disclosure binding and the US legislating toward it, the repricing compounds the retrofit problem facing legacy data centers and will not be subtle.