Turkey Engineers a $13B Catalytic Bet on Sovereign Compute

Catalytic capital design, data localization as demand driver, the 1 GW target, grid sequencing, EU adequacy optionality, hyperscaler positioning

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Türkiye has committed $3 billion in public funding to mobilize $10 billion in private data center and AI investment by 2030.

The capital design is the signal.

This is a deliberately engineered leverage structure aimed at building sovereign compute capacity, and the sophistication of the design is what separates it from the announcement-driven programs it will be compared to.

The Capital Structure Is Engineered, Not Announced

The $3 billion is not a procurement budget.

The Ministry of Industry and Technology structured it as anchor capital intended to crowd in roughly $10 billion in private investment, a 3.3x leverage target.

The mechanism underneath it is the HIT-30 program, a $30 billion high-tech incentive umbrella that allocates a dedicated $1.5 billion tranche to hyperscale and AI-compatible infrastructure.

Eligibility is gated with precision: minimum 30 MW IT load, at least 50 percent AI hardware compatibility, PUE at or below 1.4, and mandatory integration with cloud or AI platforms.

The state is not buying data centers.

It is underwriting the conditions under which private operators build them, and it is reserving the incentive for facilities at hyperscale density only.

This is disciplined capital-formation design.

The 2 percent mandatory allocation of public investment programs to AI projects manufactures a domestic demand baseline, which gives private operators a predictable state revenue anchor.

Türkiye has built a structure that de-risks private capital at the entry point and guarantees it a floor of demand at the exit.

That is the part institutional readers should study, because it is more sophisticated than the headline figure suggests.

Localization Has Already Converted Policy Into Demand

The clearest evidence the design works is that it has already pulled a hyperscaler commitment.

Data localization rules enacted in late 2024 require platforms with more than one million daily Turkish users to process data domestically.

That mandate converted a policy preference into a physical infrastructure requirement, and it compelled Google to commit $2 billion to a Turkcell cloud region rather than serve the market from Frankfurt.

Türkiye engineered captive demand through regulation and then attached incentives to it.

The localization mandate is doing exactly what capital-formation policy is supposed to do: it created the demand the capital now funds.

The structural advantages sit underneath this. Istanbul sits within 50 ms of Europe, MENA, and Central Asia.

Power runs at $0.08 to $0.10 per kWh, roughly 40 percent below European averages, and construction costs run below Gulf markets.

Türkiye is not competing on raw scale against Gulf programs.

It is competing on geography, latency, and cost, and that is a defensible position for the workloads it is built to serve.

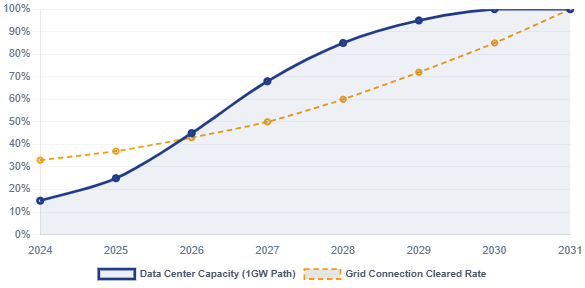

The Grid Is the Sequencing Variable

The 1 GW installed-capacity target for 2030 sits against a current operational baseline of 160 to 471 MW, depending on methodology.

The gap is real, and the variable that governs how fast it closes is power.

Two-thirds of new renewable energy projects currently face grid connection approval delays, and the $10 billion national transmission upgrade is scheduled for completion in the early 2030s.

This is the sequencing question every allocator should track: not whether Türkiye can build the grid, but in what order the grid and the data centers arrive.

Grids get built, and Türkiye’s nominal generation capacity of 115 GW is not the constraint. Transmission timing is.

Renewable generation concentrates in central and eastern Anatolia and the Aegean coast, while demand concentrates in the industrial northwest, and the interconnection to bridge that gap is what paces conversion.

This does not make the roadmap fail.

It makes the roadmap a timing question, and timing questions reward the allocators who track interconnection milestones rather than announcement cadence.

The state is already responding, with operators testing liquid immersion cooling and feasibility work underway on naturally cooled sites to reduce the power draw per facility.

The Adequacy Question Is Optionality, Not a Ceiling

Türkiye does not yet hold an EU data adequacy ruling, and the divergence in hyperscaler behavior reflects it.

Google has committed $2 billion. AWS and Microsoft have not committed full cloud regions.

That split is the market pricing an open question rather than a settled verdict.

Read correctly, the adequacy gap is optionality: domestic and regional demand supports the buildout today, and an adequacy ruling would unlock the EU-regulated workload pool on top of it.

The base case does not depend on the ruling. The ruling is upside the current entrants are positioned to capture first

Investor Action

Private capital should treat this capital-formation framework as a reason to begin diligence now. The HIT-30 program improves project economics through tax incentives and energy subsidies, materially de-risking the capital stack for facilities exceeding the 30 MW threshold.

The variable to underwrite is interconnection timing.

The cost of waiting for the grid to visibly clear is entry at a repriced basis once the sequencing resolves. The window to structure at current land and power cost is open now.

Public Markets investors holding Turkish telecom and infrastructure equity should benchmark exposure against the state-linked operators carrying this buildout, which sit inside the sovereign wealth portfolio.

The 25 percent-of-revenue capital expenditure commitment from the anchor operator and the multi-billion concession pledges from the incumbents are the public-market expression of this roadmap.

Calibrate position sizing to grid execution milestones.

Operators and hyperscalers evaluating market entry should sequence on the adequacy question as an optionality trade.

The operator that structures land and power agreements now captures the latency arbitrage at the lowest basis, with an adequacy ruling as upside rather than a precondition.

The asymmetry favors early structuring for operators whose workloads are domestic or regional, and the adequacy ruling extends the addressable market on top of a case that already clears.

The Verdict

The capital commitment is credible and the leverage design is genuinely well-engineered.

Türkiye has built a capital-formation structure and a regulatory demand driver that most sovereign compute programs announce but do not deliver.

Whether $13 billion converts into 1 GW by 2030 is a sequencing question, governed by grid timing and adequacy positioning, and both are variables an allocator can track rather than risks that sink the case.

The market inflection arrives when the first hyperscale facility energizes at full load against a resolved interconnection.

Allocators should position for that moment now, while the basis is low.

The open question is the pace of conversion, and the next twelve months of grid-queue data will tell you whether to accelerate or wait.