The Pass-Through Tariff Is the Real Asset in the Anthropic-TeraWulf Lease

MISO energy risk transfer, brownfield interconnection inheritance, single-tenant control premium, investment-grade rent, execution-window exposure

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

The Risk Transfer Is The Signal, Not The $19 Billion

The structural signal in the Anthropic-TeraWulf lease is not the $19 billion headline.

It is the pass-through tariff filed with the Kentucky Public Service Commission, under which TeraWulf and Anthropic bear all MISO energy and capacity market risk while Big Rivers Electric and Kenergy carry none.

Mainstream coverage has read this deal as a revenue event and a crypto-to-AI pivot story.

The consequence of that read is a mispriced risk profile: the market is underwriting $950 million in average annual rent as if it were utility-grade cash flow, when the underlying power cost sits on the tenant and landlord as a floating wholesale exposure with no margin buffer.

Brownfield Interconnection Is The Scarce Asset Being Monetized

The first read is that the campus monetizes an interconnection, not a building.

The Justified Data site inherited grid access from a retired 600-job aluminum smelter a load already sized for utility-scale industrial draw.

Greenfield projects in this power category wait years for interconnection queue clearance.

TeraWulf calibrated its entire strategy around acquiring legacy high-power sites and building to an anchor tenant, and this lease validates that the interconnection is the value, not the concrete.

Over the next 12 to 24 months, expect competing developers to underwrite retired smelters, steel mills, and coal plants at a premium to greenfield, because the queue position is the moat.

The scarcity is regulatory, not physical.

The Pass-Through Structure Converts Landlord Yield Into Tenant Exposure

The second read is that the pass-through mechanism reallocates who absorbs the volatility that utility-grade cash flow is supposed to eliminate.

Power is delivered with no mark-up on wholesale cost, and the customer is responsible for all transmission and delivery costs and entitled to all MISO node revenues and credits.

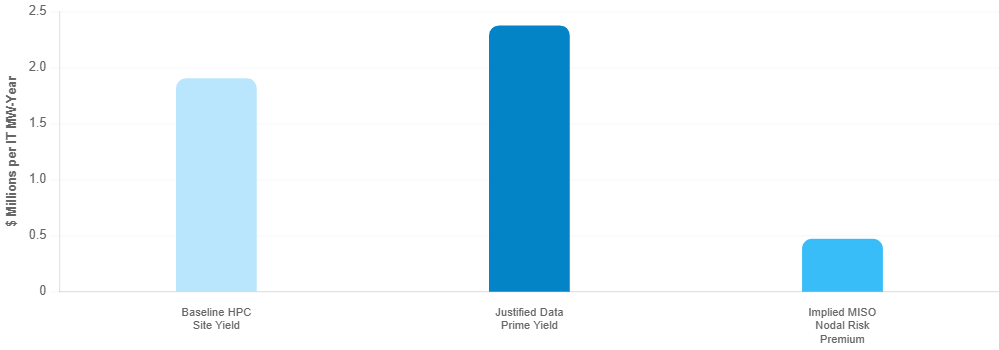

This is what produces the premium unit economics approximately $2.37 million per critical IT megawatt-year against a prior industry assumption near $1.9 million but the premium is compensation for risk the tenant and landlord retain, not a free re-rate.

An investor benchmarking this yield against a triple-net utility lease is comparing two different instruments.

The MISO node exposure is the difference, and it does not disappear because the tenant is investment grade.

Rent Commencement Timing Exposes An 18-Month Funding Window

The third read is a liquidity structure hiding inside a revenue story.

Rent commences only as each phase is delivered and commissioned, which protects Anthropic from paying for unenergized capacity but leaves TeraWulf funding a $3.5 billion to $4.0 billion build across an approximately 18-month window with no offsetting lease cash flow.

The Abernathy divestiture $530 million in three installments timed to site preparation, long-lead procurement, and commissioning is not incidental.

It is the bridge across that window.

The proposed $3.5 billion debt package expected to be led by Morgan Stanley completes it.

The signal is that this deal’s execution risk is front-loaded into the pre-revenue period, and the capital stack has been engineered specifically to survive it.

Investor Action

Private Capital. Infrastructure and real estate funds evaluating brownfield conversion should re-benchmark interconnection queue position as a standalone underwritable asset, separate from the physical build.

The diligence action is to price the MISO pass-through exposure explicitly rather than accepting the headline per-megawatt yield as utility-equivalent.

The cost of waiting is that the premium sites retired smelters and coal plants with inherited transmission get bid away by developers who underwrite the queue position first.

Position now on legacy high-power industrial sites or accept greenfield timelines.

Public Markets. Equity investors in TeraWulf and comparable converted miners should separate the contracted-revenue narrative from the pre-revenue funding exposure.

The diligence action is to model the 18-month construction window against the disclosed debt raise and the Abernathy installment schedule, not against the $19 billion aggregate.

The cost of inaction is holding through a dilution or refinancing event mispriced as a pure re-rate. Verify the investment-grade credit reference against actual lease terms, because Anthropic is a private company and the language warrants confirmation.

Operators. Data center developers and hyperscalers acting as tenants should read the single-tenant direct-lease structure as the strategic move it is.

Anthropic secured dedicated, controlled 401 MW capacity outside the cloud metering model, at roughly 4% of its total planned capacity, as part of a deliberate multi-provider strategy.

The diligence action for operators competing for anchor tenants is to structure pass-through tariffs that transfer market risk cleanly, because that transfer is what makes the premium yield financeable.

The cost of failing to do so is losing anchor mandates to developers who can.

The Verdict

This lease is a template, not an outlier.

It decouples high-density compute from the public cloud and binds it directly to a utility-scale energy asset with the market risk pushed onto the counterparties best able to contract around it.

The inflection is the emergence of the brownfield-plus-pass-through structure as the repeatable unit of AI infrastructure development inherited interconnection, single-tenant anchor, wholesale risk transfer, phased rent commencement.

The open question for the next 24 months is whether the tenants signing these leases hold investment-grade credit that survives a training-economics downturn, because the entire structure rests on rent obligations that do not begin until capital has already been spent.