Tenant Concentration: The Credit Divide Repricing Data Center Risk

Neocloud counterparty risk, lease-debt duration mismatch, single-tenant REIT exposure, credit enhancement structuring, emerging-market replacement liquidity

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Tenant credit quality has become the primary determinant of whether a data center investment survives its own lease term.

The old paradigm underwrote concentration risk on asset quality, location, and power access, then treated the anchor tenant as a fixed input.

That paradigm no longer holds, and the cost of applying it is a facility that finances against a counterparty which cannot service the lease for its full duration.

The Intermediation Layer Nobody Priced

The AI buildout created a new intermediation layer that most underwriting models were never designed to price.

Neocloud providers lease long-dated capacity from operators, populate it with GPU clusters, and resell compute on short-duration contracts.

The capital is moving toward this layer at scale, and a widening share of new colocation demand now sits with tenants whose credit profile bears no resemblance to the hyperscalers who anchor the sector’s financing architecture.

The question is not whether these tenants are growing.

The question is whether they will be capable of paying rent for the full term of a fifteen-year lease, given every competing claim on their cash over that period.

How the Constraint Works

Here is how the constraint works.

A hyperscaler tenant carries an investment-grade rating, diversified revenue, and direct access to public debt markets.

A sub-hyperscaler tenant carries none of these.

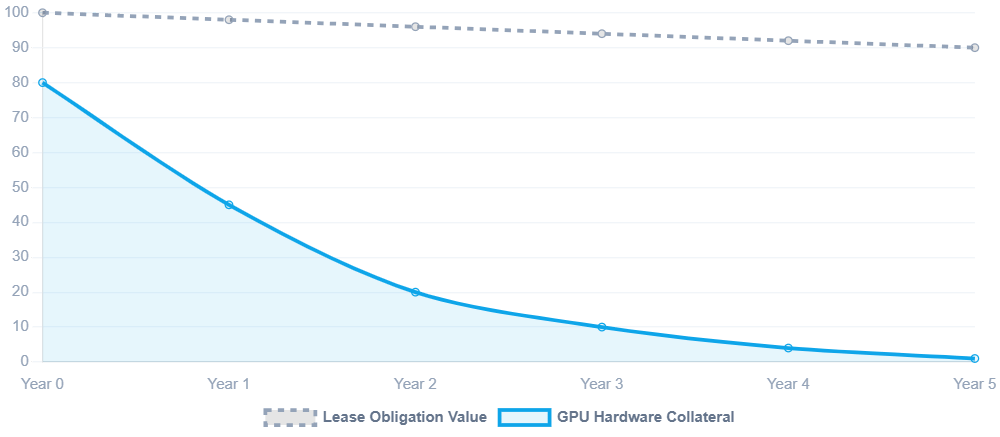

It runs a duration mismatch at the center of its model: client compute contracts run four to five years, but the data center lease that houses them runs fifteen or more.

The tenant’s ability to service that lease depends on two things holding simultaneously. GPU hardware must retain residual value as collateral.

Compute rental rates must stay high enough to cover debt. Both are under pressure at once.

Peak GPU rental rates have compressed sharply as newer architectures cut per-token costs, and each hardware generation erodes the collateral value of the last.

A regional operator that accepted a fast-growing neocloud at premium pricing to lock in capacity ahead of a power moratorium now holds a fifteen-year obligation underwritten against a business whose margins compress faster than the lease resets.

A Lease Is Only As Long As Solvency

The industry has long assumed that a signed long-term lease is a credit-equivalent instrument.

That assumption held when the universe of tenants capable of signing a fifteen-year data center lease was small, investment-grade, and cash-generative.

It does not hold now, because the tenant pool has expanded downward into a tier of counterparties whose contractual commitment far outlasts their demonstrated ability to honor it.

A lease is only as long as the tenant’s solvency.

Concentration risk also propagates vertically.

A neocloud tenant may rely on a single customer for most of its revenue, meaning a landlord who appears diversified may still have indirect exposure to the same hyperscaler whose lease pause caused the original stress.

Default Is Not Clean

The supply side hardens the problem, and it does so through time.

Data centers are among the most capital-intensive real estate assets in existence.

A facility built to a specific tenant’s power density and cooling specification cannot be re-leased quickly when that tenant fails.

Backfilling a specialized asset commonly runs twelve to eighteen months in secondary markets, and debt service must be covered from reserves or sponsor support throughout.

The asset that looked like commodity real estate at underwriting reveals itself as a bespoke industrial facility at the moment of default. Power scarcity compounds the sequencing pressure.

Operators who might have waited for a tenant’s financials to season instead accepted the tenant early, because the capacity had to be committed before the interconnection window closed.

Where It Binds

For independent operators, the binding variable is tenant qualification.

A single-asset facility leased entirely to one below-investment-grade counterparty is not comparable to a multi-tenant building where diversification absorbs an individual default.

The operator underwrites the whole asset against one balance sheet.

When that balance sheet is speculative grade, the facility inherits the tenant’s credit as its own.

For private equity and infrastructure investors, the binding variable is the financing cost differential and its effect on returns.

A hyperscaler-anchored project finances at materially tighter spreads and higher loan-to-cost than a neocloud-anchored one.

The same asset, in the same location, with the same power contract, requires substantially more equity per megawatt when the anchor tenant is speculative grade.

That equity requirement compresses the internal rate of return directly and constrains how much the sponsor can deploy.

Poor tenant credit does not merely raise the cost of capital. It caps the velocity of the entire strategy.

For public equity investors, tenant concentration drives valuation.

Single-tenant vehicles often trade at persistent discounts because the market prices counterparty risk before fundamentals.

REITs heavily dependent on one tenant typically underperform those backed by diversified or investment-grade tenants, making valuation dispersion a lasting feature of the sector.

Emerging Markets Tighten Every Rule

In emerging markets, every one of these disciplines tightens.

The replacement tenant pool is thinner, so a default that a primary US market absorbs in months can strand an asset for far longer.

You anchor with an investment-grade cornerstone before financing, you build longer vacancy reserves, and you treat sovereign or telco offtake as a credit floor where private investment-grade tenancy does not exist.

The Direction Is Set

The rating agencies have already moved.

The direction of institutional underwriting standards is set, and it points toward progressively excluding the weakest tenants from institutional capital access.

Underwrite tenant credit for the full duration of the lease, at the portfolio level, and you convert a mispriced risk into a source of advantage.

Wait for further confirmation, and you will hold the assets the disciplined capital declined.