Stranded Glass: Why Older Fiber Is Repricing as a Depreciating Asset

GPON obsolescence, corridor concentration risk, overbuild margin compression, remediation capex, dark fiber repositioning, exit multiple discounts

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Older fiber has stopped behaving like utility infrastructure and started behaving like an operating asset that decays.

The market underwrote fiber as durable, low-touch, and close to permanent.

That paradigm no longer holds, and the cost of holding onto it is a mispriced portfolio.

The reprice is accelerating because three forces arrived at once.

AI-grade tenants reset the performance floor.

Overbuild commoditized the pricing.

Higher capital costs closed the window in which incremental reinvestment was economically tolerable.

The question is no longer where demand is growing.

The question is where capital is quietly getting stranded inside assets that still look healthy on a revenue line.

Obsolescence Is Systemic, Not Structural

Start with what obsolescence actually is.

It is not glass degrading in the ground. It is systemic, and it shows up across three layers at the same time.

Physical plant entropy accumulates as legacy routes absorb splices, field fixes, and undocumented interventions, and each splice becomes an operational dependency rather than a line of optical loss.

Network design fragility means paths that look diverse on paper often share the same physical right-of-way, so assumed redundancy converts into concentrated exposure to a single excavation or flood.

Information decay compounds both, as platforms assembled through acquisition inherit incomplete as-builts and inconsistent records that extend repair times and inflate make-ready costs.

A regional operator that acquired three networks over a decade discovered its “diverse” enterprise routes shared a single corridor under a rail line. One excavation event took down four enterprise clients at once.

That is not a maintenance ticket. That is a capital event the model never priced.

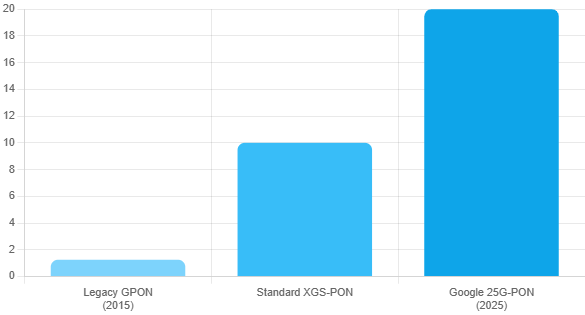

Then there is the technology clock. A network is no longer legacy because it is old. It is legacy because it runs dated technology, even when the build is recent.

The generation shift from GPON to XGS-PON, and now to 25G PON, has moved the acceptable specification.

Google Fiber began deploying 25G PON equipment to enable symmetrical 20-gigabit service across its markets, with installations underway in North Carolina.

When a named operator moves the ceiling that publicly, every network below it inherits functional obsolescence whether or not the glass works.

Build-Once Was Always a Myth

The industry has long assumed fiber was a build-once asset.

That assumption held when bandwidth ceilings rose slowly and lit-service pricing stayed firm.

It does not hold now, because the performance floor is being reset by east-west data center interconnect traffic that older lit networks were never designed to carry efficiently.

AI capacity growth requires a step-change in fiber route miles and total fiber miles, and the traffic is predominantly datacenter-to-datacenter.

Older networks do not fail this test loudly. They fail it commercially, losing the tenants that pay the premium.

Replacement Costs More Than the Original Build

The supply side makes the reprice worse.

Replacing obsolete fiber costs more than laying it did.

Labor runs the majority of deployment cost, and labor costs across the sector have climbed materially since 2020. Underground deployment costs rose again year-over-year.

Full-route refreshes run into the tens of thousands of dollars per mile in constrained contexts.

The asset was underwritten at construction economics that no longer exist.

For a fund holding a network built in the second half of the last decade, the reinvestment cycle lands inside the hold period, not after the exit.

Where the Constraint Binds

For independent operators, the binding constraint is documentation. A network that cannot demonstrate clean GIS data, splice records, and verified corridor diversity cannot be qualified by a sophisticated buyer or a hyperscaler tenant.

Record quality is now a first-order underwriting item.

The operator that treated it as an afterthought discovers the discount at exit.

For private equity and infrastructure investors, the biggest risk is unmodeled replacement capex. A platform can deliver strong demand and revenue but still miss cash flow targets because the physical network requires more rebuilding than expected.

This quietly erodes IRRs as unplanned remediation capex accumulates.

Over 50 percent of European fiber operators also face near-term debt maturities, while lenders increasingly require operational documentation that many legacy platforms cannot provide.

For public equity, the constraint is dispersion. The market is separating fiber businesses positioned for AI transport from those exposed to commoditized consumer access.

B2B backbone operators lighting 400G and 800G fabrics for data center interconnect are being valued on a different curve than lit-service networks competing on price per megabit.

The gap between positioned and exposed assets is widening, and it will not narrow.

Underwrite the Decay

So underwrite differently. Reorder the site and asset filters to put physical condition, splice density, failure history, and corridor correlation ahead of route-mile count.

Model replacement capex as a scheduled certainty inside the hold period, not a tail risk after it.

Convert emergency capex into planned capex by targeting flood-prone sections, heavily spliced corridors, and single-corridor dependencies on high-value routes before they fail.

Reprice the commercial offer around resilience, restoration performance, and certified physical diversity, because one enterprise client with real downtime costs is worth more margin than ten unmanaged dark routes.

Where you can, shift capital toward strategic route control, dark fiber, and long-term IRU structures where you own the duct and the rights-of-way, because exclusivity is the last durable moat in a commoditized market.

Exploit the XGS-PON upgrade path, which reuses the passive fiber plant and replaces only the active electronics, so modernization is a phased cost rather than a greenfield rebuild.

You are not managing a utility. You are managing a depreciating operating asset that requires continuous reinvestment to stay commercially relevant.

The investors who price that discipline into entry will buy the discount others are about to discover at exit.