Power Contracted Is Not Power Delivered

Interconnection queue collapse, renewable intermittency, SLA penalty exposure, availability-based underwriting, behind-the-meter generation, the megawatt gap that breaks IRR

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Power availability now decides which data center investments work and which quietly fail.

The old underwriting paradigm treated power as a line item, secured through a renewable PPA and assumed to be continuous once the megawatts were contracted.

That assumption is now one of the most expensive mistakes in digital infrastructure, because the gap between contracted and delivered megawatts is where returns disappear.

The market reached this point because AI-grade compute demand outpaced what aging transmission systems can energize.

Capital flooded into data center development just as the grid lost the ability to absorb it.

The question is no longer where demand is strongest, but where power can be delivered on time at AI scale.

That is where capital is moving, and most underwriting has not caught up.

A PPA Is a Price, Not a Guarantee

The mechanics are simple once you separate two things the market still conflates.

A power purchase agreement contracts a price for energy, but it does not guarantee power arrives when a training cluster needs it.

Renewable generation makes this worse, not better. Solar produces during daylight.

Wind produces when the weather cooperates. Neither produces on demand. An AI cluster does not tolerate a generation shortfall as a commercial inconvenience. It treats interrupted delivery as a workload failure.

So a project can hold a PPA covering 100 percent of its nameplate load and still face hours where contracted power and delivered power diverge sharply.

Consider a hyperscale project in a high-renewable market that treated its PPA as continuous supply. The financing assumed firm power, but the grid delivered intermittent power.

The difference surfaced as diesel burn and emergency grid draw, both unbudgeted.

The Market Is Wrong About Contracted Megawatts

The industry has long assumed that contracting megawatts is the same as securing power.

That assumption held when grids carried ample dispatchable baseload and interconnection took under two years. It does not hold now.

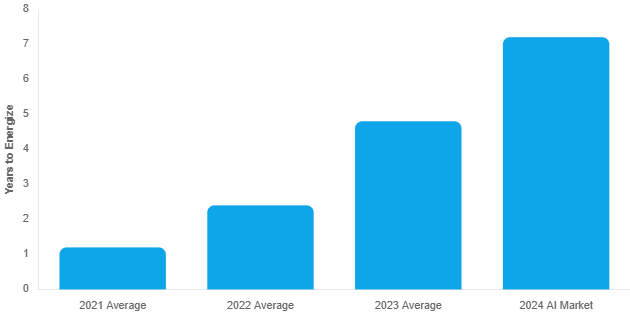

Interconnection queue times have stretched toward five years in major markets, with some projects waiting far longer.

The typical timeline from request to energized power in the United States has moved from roughly one year to more than seven over the past three years.

Power is no longer a procurement step. It is the binding constraint on the entire development schedule.

Transmission Is the Bottleneck

The supply-side friction compounds the problem and time is the scarce resource, not money. Transmission and distribution, not generation, form the true bottleneck.

Utilities can often produce enough power. They cannot move it across networks that were never built for gigawatt-scale point loads.

Substation upgrades in prime markets are now scheduling into 2030 and beyond. A single substation constraint can hold back new supply in a major metro for years.

Then layer in the episodic risk. A transmission line failure can disconnect dozens of large data centers from the grid at once, shifting them to backup generation and forcing the grid operator into emergency action.

Regulators have taken notice. Reliability authorities now categorize large AI loads alongside other facilities capable of destabilizing the bulk power system.

This carries compliance and liability weight that did not exist in prior underwriting.

Three Lenses, Three Binding Constraints

For independent operators, the binding constraint is site qualification. A site with cheap land and a willing utility means nothing if the interconnection study returns a 2031 energization date.

The discipline is to qualify power delivery before anything else, because every other site attribute is subordinate to whether the megawatts arrive.

For private equity and infrastructure investors, the binding constraint is schedule risk priced into IRR.

A one-month delay alone can erase double-digit millions through lost lease revenue, overruns, and penalties. Schedule risk is no longer a construction footnote. It is the decisive underwriting variable.

For public equity investors, the binding constraint is dispersion between positioned and exposed assets. Operators that secured firm power ahead of the market will hold pricing power and uptime.

Operators that bet on grid availability they never locked down will miss service commitments. That divergence will widen as the supply-demand imbalance persists, and the market has not fully repriced the operators on the wrong side of it.

The Penalty Hiding in the Lease

There is a second, under-modeled exposure sitting inside the lease itself. Service level agreements convert reliability failures directly into cash flow volatility.

Uptime penalties scale aggressively, and severe breaches can trigger termination rights.

A short outage at a large facility under a standard hyperscale SLA can wipe out a meaningful share of annual cash flow through automatic service credits that apply without negotiation.

For lenders, that exposure feeds straight into debt service coverage.

Underwriting that ignores SLA mechanics is underwriting blind to its own downside.

How Disciplined Capital Underwrites Power

The disciplines that separate resilient capital from exposed capital are clear.

Make power delivery the first site-selection filter and complete power diligence before investment approval.

Underwrite to availability, not nameplate capacity. Model the gap between contracted and delivered power, and stress-test returns against energization delays and uptime risks.

Secure power ahead of the market through ownership or firm long-term contracts.

Leading investors lock in reliable baseload through nuclear and behind-the-meter solutions rather than relying solely on PPAs.

Deploy storage as a commercial asset to improve reliability and economics. Grid-scale solutions remain years away, so operators who treat power as the first underwriting variable will hold the advantage. Disciplined power underwriting is the edge.