Oracle Q4 FY2026: Hyperscaler Capex, No Hyperscaler Balance Sheet

How negative free cash flow of $23.7B, a BBB rating, and an $88B two-year raise made Oracle the cohort's first test of whether capital structure sets the ceiling on AI infrastructure

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

The hyperscaler capex debate spent 2025 fixated on demand.

Whether Amazon could clear $200B, whether Alphabet could sustain $90B-plus, whether Meta could execute gigawatt-scale buildouts.

The four canonical prints answered the question.

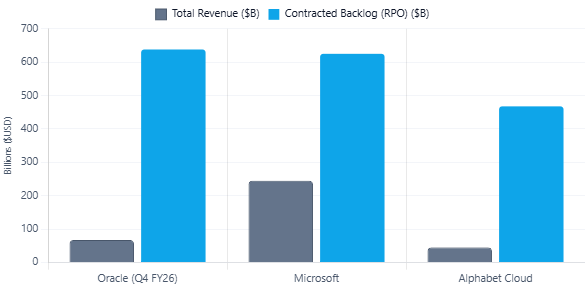

Microsoft backlog reached $625B, Alphabet Cloud backlog reached $467.6B, AWS disclosed roughly $200B.

Demand was never the constraint. Power was the binding one. Capital was the enabler.

Oracle’s Q4 FY2026 print raises a different question.

Remaining performance obligations (RPO) reached $638B, up 363% year over year and now exceeding Microsoft’s backlog.

Demand is no longer in doubt.

The issue is whether Oracle can finance it.

Unlike peers that entered the cycle with AA-rated balance sheets, Oracle is funding a hyperscaler-scale expansion from a BBB-rated balance sheet already generating negative free cash flow.

It is the first major test of whether capital structure can support demand at hyperscaler scale.

The Signal: Demand Confirmed, Structure Exposed

What changed structurally this quarter is not the revenue.

Total revenue of $19.18B grew 21%, with Cloud Infrastructure up 93% to $5.8B.

Strong and accelerating, but not the dislocation.

The dislocation sits in the gap between what Oracle has contracted and what its balance sheet can fund without reaching for external capital.

Free cash flow for FY2026 was negative $23.7B against $32.0B of operating cash flow.

The difference is $55.7B of capital expenditure that surged 162% and overshot Oracle’s own $50B guidance by $5.7B. Depreciation doubled to $7.1B.

Calibrate the posture against the cohort.

Meta funded its 2025 buildout largely from $115.8B of operating cash flow and stayed free-cash-flow positive at $43.6B.

Alphabet deployed two-year spending above $270B while retaining the operating cash generation of Search and YouTube.

Oracle is funding its program from a cash base that does not cover it, and the shortfall is structural rather than transitional, because FY2027 guidance widens the gap before it narrows.

Infrastructure Strategy: Backlog as Anchor, Not as Cover

The RPO trajectory across FY2026 reads as a vertical line. $455B in Q1, $523B in Q2, $553B in Q3, $638B in Q4.

Management points to this anchor when defending the capital intensity, and the anchor is genuine.

A backlog growing 363% does underwrite a buildout the way AWS backlog underwrote Amazon’s.

The key distinction is concentration. Microsoft disclosed that roughly 45% of its $625B RPO was tied to OpenAI, which markets viewed as counterparty risk.

Oracle’s $638B backlog sits against a much smaller $67B revenue base, implying a significantly higher backlog-to-revenue ratio.

Oracle has not disclosed customer concentration, but the structural point remains: a backlog of that scale likely depends on fewer counterparties.

The market sees demand validation.

The unpriced question is how concentrated that demand is and how resilient it remains if major customers re-price or delay commitments.

Capital Allocation: Financing the Gap, Defending the Rating

This is where Oracle diverges from the cohort.

Alphabet, Meta, and Microsoft financed their AI buildouts from positions of balance-sheet strength and substantial internal cash generation.

Oracle is funding a similar-scale expansion from a weaker starting point.

During FY2026, Oracle raised $43B of debt and $5B of equity, including a record $25B bond issuance.

It has since announced another $40B for FY2027, bringing total planned financing across two years to roughly $88B. Meanwhile, FY2027 net capex is expected to reach approximately $70B.

The critical detail is the equity component. Management authorized a $20B at-the-market equity program to protect its BBB rating.

That signals debt capacity alone cannot support the buildout.

The 8.5% after-hours decline was not a reaction to demand.

It reflected dilution risk and a balance sheet increasingly constrained by its own capital requirements.

Competitive Positioning: Joining the Spend, Not the Structure

Oracle’s $70B FY2027 net capex places it alongside Meta and within reach of Alphabet and Microsoft on spending.

On capital structure, however, it remains an outlier.

The key differentiator is not capex volume but balance-sheet capacity.

Oracle is funding a hyperscaler-scale buildout from the weakest financial position in the group, leaving it with the narrowest margin for error if backlog conversion slows or demand timing shifts.

That is the competitive reality the headline backlog obscures. Oracle does not need demand to materialize.

It needs demand to convert to cash on a schedule that its financing plan and its rating can survive.

The others carry the same conversion requirement with years of balance-sheet cushion absorbing any slippage. Oracle carries it with months.

System Pattern: The Constraint Stack Adds a Layer

Across the hyperscaler cohort, the key constraints have been power and component availability.

Oracle introduces a third: financing.

For Microsoft and Alphabet, capital remains an enabler.

For Oracle, it has become a constraint, with its BBB rating increasingly influencing how fast it can scale regardless of power or silicon availability.

The broader signal extends beyond Oracle. For operators below AA, the limiting factor is no longer just megawatts or GPUs.

It is whether the balance sheet can sustain negative free cash flow long enough for backlog to convert into cash flow.

Oracle is the first hyperscaler-scale test of that threshold, and its equity ATM is the clearest sign yet that demand alone does not solve the capital equation.

Forward View: What Resolves Next

Three signals will determine whether Oracle’s structure can support its backlog.

First, free cash flow.

FY2026 free cash flow was negative $23.7B, and FY2027 capex is expected to rise further. The key question is whether operating cash flow can close the gap or whether external capital becomes a recurring requirement.

Second, customer concentration.

The market treats $638B of backlog as demand validation. Any disclosure of concentration or a change in commitments from a major customer could shift that perception from growth to exposure.

Third, the rating.

Oracle’s equity ATM was designed to protect its BBB rating. A downgrade would increase funding costs just as capital needs accelerate, making the rating a critical determinant of future buildout pace.

The demand debate is over. Oracle’s backlog settled it.

The real question is whether the balance sheet can scale fast enough to support the demand already secured.

For the first time in this cycle, the primary constraint is not power, silicon, or demand. It is the capital structure funding the buildout.