Land Is No Longer the First Question in Data Center Development

Site control structures, power deliverability, entitlement value, zoning moratoria, and the diligence sequence that decides which sites are real

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

This article is the 5th article in the series: Ground to Grid: A Free 21-Lesson Guide to Mastering Data Center Development

Power deliverability now determines whether land is a viable data center site or just speculative real estate.

Many projects still prioritize land before power, but without a credible energization path, the site isn’t an asset it’s only an option on an infrastructure constraint.

The shift happened quickly.

Transmission constraints are now the top grid bottleneck, with utilities quoting 4–10 year connection timelines and up to 12 years just for studies.

While capacity is expected to grow ~14% annually through 2030 (adding ~100 GW and doubling footprint), demand is outpacing the grid.

The core question has shifted from where to build to where power is available, reshaping the entire acquisition process.

The Sequence That Worked for a Century Stopped Working

Start with the history, because the inversion is recent.

For most of commercial real estate, developers identified land first and engaged utilities second.

That worked when grid capacity was abundant and a connection was a formality.

It stopped working when hyperscale and AI load collided with a transmission system that takes seven to eleven years to permit new regional lines.

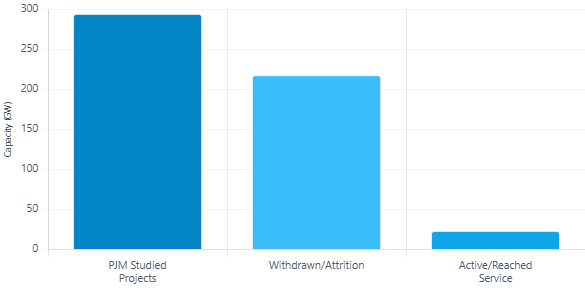

The PJM interconnection queue tells the story in two figures that measure different things.

One is scale: PJM studied 294 GW of projects between 2020 and 2026, of which only 23 GW reached service.

The other is attrition: 74% of studied projects ultimately withdrew. Scale reflects demand, but attrition shows how little survives the process. Both figures point to a system where land was never the constraint.

What a 9x Move in Eighteen Months Actually Priced

The value of solving for power shows up directly in land prices.

In Stafford County, Virginia, Peterson Companies assembled 504 acres for $32.25 million across 2023 and 2024, roughly $64,000 per acre.

The firm secured data center entitlements in September 2024, then sold the entitled site to Stack Infrastructure in January 2025 for $302.3 million, approximately $600,000 per acre.

That is close to a 9x move in eighteen months. The land did not change.

What changed was certainty entitlement and a power path converted raw acreage into a deliverable site.

More broadly, entitled, power-ready land now trades at two to four times the value of standard industrial parcels, and power-ready land in Ashburn exceeds $3.5 million per acre.

Site Control Is the Entry Ticket, Not the Purchase

This is where the acquisition process has to be understood as a structure, not a purchase.

Site control comes first outright purchase, ground lease, option, joint venture, or land banking and it is the prerequisite for everything downstream.

Utilities will not study a load application without proof of site control.

Lenders will not advance pre-development capital without it.

Under PJM’s first-ready, first-served rules, a developer must demonstrate continuous, exclusive site control or face non-appealable removal from the study queue.

Control is no longer a real estate step. It is the entry ticket to the power process.

The Scarcity Is Not Where the Market Thinks It Is

The narrative has focused on land scarcity in Tier 1 markets.

That misses the actual constraint. The capital reality is that scarcity is not about acreage at all.

Northern Virginia carries roughly 2,745 MW across more than 150 facilities with core Loudoun County vacancy below 1%.

Developers are pushing into Stafford, Spotsylvania, Culpeper, and secondary markets in Iowa, Ohio, and West Virginia.

They are not chasing land. They are chasing power and permission.

The parcels exist. The deliverable parcels do not.

Three Lenses on the Same Parcel

Independent operators face the qualification problem first. Sites must meet soil capacity for heavy loads, usable buildable area after constraints, water availability, and fiber diversity before even reaching tenant discussions.

Many fail late because power, land, environmental, and community risks were assessed separately.

The discipline that prevents this is concurrent evaluation assess all constraints together before committing capital.

Private equity and infrastructure investors face a different issue: underwriting power that does not yet exist. Power must be segmented into four buckets existing capacity, confirmed expansion, queued capacity, and developer-controlled supply.

Only the first two are bankable. Investments based on queue positions are exposed to withdrawal risk.

The key question is not potential power, but defensible power in underwriting.

Public equity reflects a structural shift in financing. Joint ventures now dominate hyperscale development. Meta’s Hyperion campus (~$27B) brought in Blue Owl Capital with an 80% stake while Meta became a tenant, supported by PIMCO debt.

Equinix applies a similar 80/20 xScale model, and Digital Realty has shared billions in development with partners across major markets.

The signal is clear: hyperscale infrastructure is too capital-intensive and power-constrained to finance alone.

Regulation Is Tightening the Screw Power Already Turned

The regulatory environment is now tightening the screw that power already turned.

Permitting has become the stage where projects die one analysis attributes 77% of project delays and cancellations to the permitting and regulatory phase.

Since 2025, at least twenty moratoria have been proposed across local, state, and federal levels.

Georgia’s HB 1059 proposes a development moratorium running from July 2026 through December 2028.

Public opposition blocked or delayed an estimated $64 billion in US developments between 2024 and 2026.

The DATA Act of 2026 moves the other direction, proposing to exempt off-grid data centers from federal oversight so they can build their own power and bypass the queue entirely.

The legislative picture is unsettled, and unsettled regulation is itself a cost.

You Are Underwriting Timing Now

You are underwriting timing now, not land. The developer who secured Stafford acreage before entitlement captured the 9x.

The investor who waits for a confirmed interconnection agreement before committing will pay the entitled price, not the raw one.

Grid connection delays alone stretch launch timelines by an average of one and a half to two years, and in a market where being twelve to eighteen months late can cede a hyperscaler tenant to a faster site, that delay is the whole contest.

The land will still be there.

The power, the permission, and the position will already belong to whoever moved first.

Part 6 examines the two lines that decide if a site is real: Power and Fiber Now Lead Data Center Siting Decisions