Indonesia's Data Center Market Hits Its Power Ceiling

Announced capacity versus deliverable capacity, BDx's 1.2 GW PLN lock-up, the transmission bottleneck, the 2030 shortfall, secured grid as the only moat

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Announced Capacity Is Not Deliverable Capacity

Indonesia’s data center market is running into a hard limit, and the limit is the grid.

The market reads announced capacity as deliverable capacity. It is not.

Operators are announcing gigawatts while grid interconnection runs three to five years and the binding constraint sits in transmission, not generation.

The cost of misreading this is straightforward:

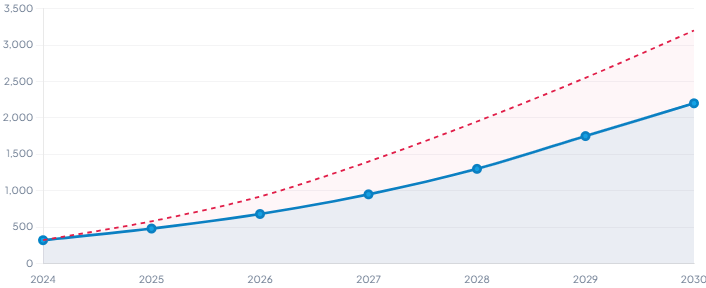

Capacity that exists on a press release but cannot be energized inside the investment horizon, while demand compounds at 19.9 percent annually.

Indonesia is projected to face a 1 GW capacity shortfall by 2030. That shortfall is not a generation problem.

It is a delivery problem.

In that environment, the gap between what an operator has announced and what it can actually energize is the whole analytical question.

Power Pre-Commitment Has Displaced Land And Capital As The Binding Moat

The first signal is the inversion of the competitive hierarchy.

In most markets, capital and land are the gating constraints and power is assumed.

Indonesia reverses this.

Capital is abundant, with hyperscalers and infrastructure funds committing tens of billions.

Land is constrained but solvable through multi-story high-density designs.

Power is neither abundant nor quickly solvable, because the scarcity sits in transmission and distribution infrastructure that takes years to build.

BDx Data Centers’ June 3 agreement with PT PLN illustrates the point.

BDx secured a 1.2 GW power portfolio across three Java campuses, including 788 MVA at CGK4 alone, a figure material against a national market measured in the low single-digit gigawatts.

The operator that secures firm power ahead of the build owns the scarcest input in the value chain.

Over the next 12 to 24 months, expect power allocation, not capital raised or land banked, to become the primary metric institutional underwriters benchmark when evaluating Indonesian operators.

The diligence question shifts from what an operator has built to what it has secured the power to build, and from what it has announced to what it can deliver.

PLN Has Shifted From Utility To Strategic Anchor Counterparty

The second signal is the changing nature of PLN.

A utility sells power on standard terms to all comers.

PLN is not behaving as a utility.

It has a stated 2,970 MVA data center target for 2027 and a 69.5 GW power development plan, and it is selecting which operators receive priority access to scarce grid capacity.

BDx’s 1.2 GW agreement represents roughly 40 percent of PLN’s stated data center target, concentrated in a single operator relationship.

That concentration is the signal.

It indicates PLN is consolidating its data center power around anchor partners rather than distributing allocation broadly.

For operators, the relationship with PLN is now a strategic asset that must be underwritten with the same rigor as the capital stack.

For investors, the operators with early PLN anchor positions hold a structural advantage that later entrants cannot easily replicate, regardless of capital.

The counterparty risk runs both ways.

An operator concentrated in a single grid relationship inherits the utility’s execution risk on transmission buildout.

The JV-Plus-Acquisition Model Is The Replicable Entry Playbook

The third signal is the entry path itself.

BDx’s sequence is a template.

Joint venture formation with domestic telco partners, acquisition of an incumbent telco’s legacy colocation portfolio, debt refinancing at scale, then grid capacity lock-up. Each step de-risks the next.

The JV secures local partners and regulatory standing.

The acquisition secures existing sites and connectivity.

The debt facility funds the high-voltage grid work. The power agreement secures the franchise.

This sequence is replicable across emerging APAC markets where legacy telco-owned infrastructure can be acquired, upgraded, and repositioned for hyperscale.

Over the next 12 to 24 months, expect infrastructure investors entering constrained Southeast Asian markets to favor this acquisition-led path over greenfield, because it compresses the timeline to firm power and regulatory standing.

The greenfield entrant starts the interconnection clock at zero.

The acquirer inherits a head start.

Investor Action

Infrastructure funds and private equity evaluating Indonesian operators should reweight diligence toward secured power allocation as the primary underwriting variable, and toward deliverable capacity over announced capacity.

Benchmark target operators on firm PLN commitments and on the transmission schedule behind them, not on built or announced capacity.

Public equity investors holding or evaluating regional data center and infrastructure names should treat PLN anchor relationships as a durable competitive signal that leads public narratives.

The market prices announced capacity and headline commitments. It does not yet discount for the delivery gap, nor price the optionality of secured-but-undeveloped power allocations.

Developers and operators without firm PLN allocations face a closing window. The competitive moat is being claimed now, campus by campus, and the operators that wait for demand certainty before securing power will inherit the three-year queue.

Sequence the power agreement ahead of the build, not after. Negotiate the grid commitment as the first move, not the last.

The Verdict

Indonesia is the clearest case in Southeast Asia of a market where announced capacity has outrun deliverable capacity, and the grid is the reason.

The operators consolidating firm grid allocations now are building franchises the 2030 shortfall will make impossible to replicate.

This is the inflection: power moves from an assumed input to the priced moat, and the operators and investors who underwrite that shift early hold positions later capital cannot buy at any price.

The open question is whether PLN’s transmission buildout keeps pace with the allocations it is signing, because every announced megawatt is only as real as the grid that delivers it.