Grid Interconnection Delays Repricing Europe’s Data Center Market

How interconnection delays and power scarcity are distorting timelines, compressing returns, and redirecting capital across Western Europe

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Western Europe’s data center sector is undergoing a structural shift. Growth is no longer driven by connectivity, capital, and hyperscale demand, but by the ability to secure grid-connected electricity within viable timelines.

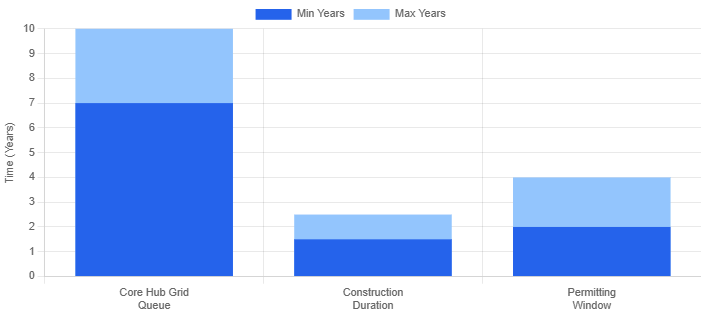

This shift is measurable in timelines, costs, and capital flows. Grid connection queues now span 7–10 years, while construction takes around 2 years, creating a mismatch that is repricing risk, reshaping geography, and redefining high-quality assets.

Event: Demand Concentration Breaks the Grid Model

The immediate trigger is the collision between AI-driven demand and infrastructure built for a different era.

In 2024, European data centers consumed approximately 96 TWh of electricity, equivalent to about 3% of total demand. At a continental level, this appears manageable. At a local level, it is destabilizing. Dublin has approached roughly 80% of electricity consumption from data centers, while Amsterdam, London, and Frankfurt operate in a range of approximately one-third to over 40% of local demand.

This concentration is amplified by the scale and profile of new workloads. Hyperscale deployments and AI clusters are arriving as continuous, high-density loads, often exceeding 100 MW per application. Unlike traditional enterprise IT, these loads cannot be easily staggered or distributed without impacting performance. They require firm, sustained power at scale.

As a result, Western Europe’s primary digital hubs Frankfurt, London, Amsterdam, Paris, and Dublin are facing stress. These markets were optimized for connectivity and proximity to users, not for absorbing multiple gigawatts of concentrated demand within short development cycles. Demand has now outpaced the grid’s ability to respond.

This concentration of high-density demand mirrors the global pattern of AI infrastructure scaling described in Meta’s $135B CapEx Signal: Ads Are Becoming an Infrastructure Product.

Cause: Infrastructure Lag Meets Renewable Complexity

The underlying causes are structural and mutually reinforcing.

First is infrastructure inertia. A significant portion of Western Europe’s grid is aging, with more than 40% of distribution networks exceeding 40 years in service. Reinforcing or expanding transmission and distribution capacity requires permitting, procurement, and construction timelines that often span several years, which are incompatible with the pace of digital infrastructure development.

Second is geographic misalignment between generation and demand. While renewable expansion has been significant, it remains uneven wind is concentrated in the north and solar in the south, while major data center hubs are located elsewhere. Transmission bottlenecks limit the movement of power, creating localized scarcity despite overall system availability.

Third is the evolution of demand itself. AI workloads are not simply larger versions of traditional IT loads; they are structurally different. Higher rack densities, continuous utilization, and rapid scaling requirements turn data centers into grid-defining assets rather than incremental consumers, driving step-change increases in local load profiles.

Finally, interconnection friction. Queue systems across core Western European markets imply connection timelines of seven to ten years. These delays are not marginal they disrupt project sequencing, leaving developers unable to energize assets within commercially viable windows even after securing land, permits, and tenants.

Together, these factors create a system where demand exists, capital is ready, but delivery is constrained by physical infrastructure and regulatory process.

These delays reflect a broader systemic bottleneck in energy delivery that is reshaping AI infrastructure globally, as examined in The Renewable PPA Squeeze Inside America’s AI Buildout.

Impact: IRR Compression and Capital Reallocation

The financial implications are direct and material.

The most immediate effect is timeline distortion. Data center investments are built around predictable development and lease-up cycles, but when grid connection timelines exceed construction, capital becomes trapped. Assets may reach completion without generating revenue, turning deployed equity into a non-yielding position.

This directly impacts returns. Delayed energization lengthens the gap between capital deployment and cash flow generation, compressing IRRs and increasing refinancing risk. Debt structures designed for shorter timelines become more fragile, especially in higher-rate environments.

System costs are also rising. EU congestion costs reached €4.3 billion in 2024, reflecting inefficiencies in power generation and transmission. Ireland’s roughly €1 billion in emergency generation measures highlights the extent of intervention required to stabilize supply, with downstream effects including higher network costs and tighter scrutiny on large-load users.

Opportunity cost is another major effect. Western Europe is expected to attract around €176 billion in data center investment between 2026 and 2031, but grid constraints will determine how much can actually be deployed in core markets. Projects that cannot secure timely power will face delays, relocation, or cancellation.

This is driving capital reallocation and asset stratification. Investors are favoring markets with reliable grid access, while power-secured sites command a premium. Value is increasingly defined by certainty of power delivery, and sites without credible access are viewed as speculative regardless of location.

Investor Response: Power-First Strategy and Geographic Repricing

Leading investors are adapting in ways that reflect a fundamental shift in how data centers are underwritten.

Geographic repricing is emerging as a key shift. Traditional hub dominance is weakening as investors prioritize grid availability over historical market status. The Nordics, parts of Southern Europe, and markets such as Italy are gaining traction due to more credible power delivery timelines, with connection periods in some cases reduced to approximately three years, improving project viability.

This is not a marginal shift. It represents a reordering of the European data center map, where secondary markets are capturing incremental demand due to structural advantages in power availability.

The redesign of the power stack is also underway. Renewable PPAs remain a core tool for managing cost and sustainability commitments, but they are no longer sufficient on their own. Investors are layering PPAs with on-site storage, phased energization strategies, and direct-line or behind-the-meter solutions. The objective is to secure not just energy in aggregate, but deliverable power at the specific location and time required.

Flexibility is becoming embedded in asset design. Non-firm connections, phased load ramp-ups, and demand response capabilities are now standard features in new developments. Rather than insisting on fully firm capacity from day one, investors are accepting structured flexibility in exchange for earlier access to power.

Earlier and deeper engagement with grid operators is also becoming standard. Investors are moving upstream in the development process, integrating grid considerations into site selection and underwriting. Queue positions, substation capacity, and planned reinforcements are now central to investment decisions.

These strategies reflect a broader shift. Power is no longer treated as an input. It is treated as the core asset around which the entire investment thesis is built.

Investor Lesson: Megawatts Define Value

The central lesson is clear. In Western Europe, data center value is being redefined by access to power.

Policy initiatives such as the EU’s Grids Package aim to ease bottlenecks through faster permitting, anticipatory planning, and grid upgrades, but these changes will take years to materialize. In the meantime, investors must operate in a constrained environment where power availability determines what gets built.

This shifts competition: land, connectivity, and capital are no longer sufficient. The key differentiator is the ability to secure reliable, timely electricity, turning data centers into energy-dependent infrastructure assets rather than traditional real estate.

Investors who adapt by prioritizing grid access and power strategy will capture a scarcity premium, while those relying on legacy assumptions risk delays and underperformance. The market is no longer pricing space it is pricing megawatts.