Egypt's Tenth Data Center License Is the Real Signal

Egypt's tenth data center license signals a market being built ahead of hyperscale demand, where interconnection rights, not construction costs, are emerging as the scarce asset.

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

The License Count Is the Signal, Not the Dollar Figure

The number that matters in Egypt is not $400 million.

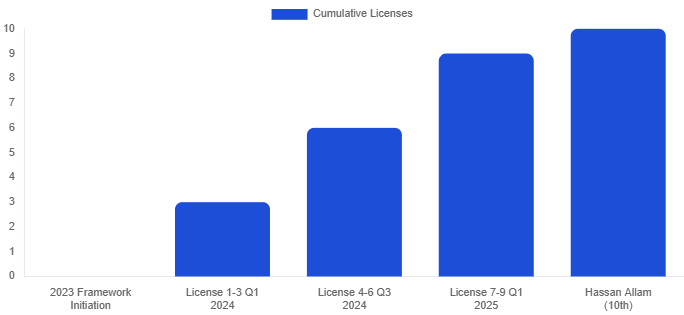

It is 10.

The National Telecommunications Regulatory Authority has issued 10 data center licenses in two years, and the Hassan Allam and A15 authorization on June 15, 2026 is the tenth.

Mainstream coverage anchored on the capital figure and the conglomerate name.

The structural signal is the cadence.

A regulator that formalized its Public Data Center Provider framework only in 2023 is now clearing licenses at roughly one every ten weeks.

Allocators reading the headline figure are pricing a single facility.

Allocators reading the cadence are pricing a market that is being licensed into existence ahead of the demand that will fill it.

The Platform Is Built to Own a Position, Not to Operate a Building

The Hassan Allam and A15 structure is the first read. This is not a pure-play operator and it is not a hyperscaler captive.

It pairs Hassan Allam Holding, an engineering, procurement, and construction conglomerate with utility-scale delivery history, against A15, an Egyptian technology and venture capital firm.

The EPC parent brings the capacity to build power-dense facilities at cost. The venture partner brings cloud commercialization and the tenant relationships that convert whitespace into contracted revenue.

The structure underwrites a vertically integrated position: land, build, power, and lease held inside one platform.

This is a model that developed markets recently introduced and is now finding its way into frontier digital infrastructure markets.

The pure-play colocation operator carries construction risk it cannot control. The hyperscaler captive serves one tenant.

The EPC-plus-venture platform captures the build margin and the lease margin and diversifies the tenant book.

Where the source material does not disclose the debt and equity split or any lender syndicate, that structure is not read here. What is confirmed is the platform composition, and the platform composition is the signal.

The License Is the Asset, Not the Facility

The second read is the license itself.

Under the NTRA framework, a Public Data Center Provider license runs 15 years and carries the right to contract directly for submarine cable capacity and fiber paths without case-by-case regulatory approval.

In a market where an estimated 17-20% of global internet traffic transits the country and 15 or more submarine cable systems land on its coasts, the direct-interconnection right is the scarce asset.

Hassan Allam and A15 have acquired a 15-year position on the transit corridor before the hyperscale demand that monetizes it has fully arrived.

The party that holds the interconnection right when that demand crystallizes captures the rent. The license is a call option on transit-corridor scarcity, and it was struck ahead of the move.

Localization Law Converts Regulatory Risk Into Captive Demand

The third read is the demand pull that most coverage treats as a compliance footnote.

Egypt’s Personal Data Protection Law restricts cross-border transfer of citizen data, and the executive regulations issued in late 2025 started a compliance clock running to October 2026.

The read most observers miss is directional. A localization regime is not a constraint on this platform. It is the demand engine.

Every multinational, financial institution, and cloud provider serving Egyptian users must domicile that data in-country.

That mandate converts a regulatory requirement into captive, non-discretionary colocation demand that cannot be served from Gulf or European facilities.

The platform that holds licensed in-country capacity when the compliance deadline forces the migration underwrites demand it did not have to win on price.

The localization law is the offtake the source material does not name in contract form but names in statute.

Investor Action

Private Capital. Infrastructure and private equity allocators evaluating frontier digital infrastructure should assess the integrated platform against the pure-play operator model.

A vertically integrated structure captures build and lease margins while controlling construction risk.

The action is to diligence the interconnection rights and the localization-driven demand curve as the underwriting spine, not the single-facility economics.

The cost of waiting is entry after the transit-corridor licenses are allocated, when the scarce asset is no longer available to underwrite and the position must be bought secondary at a premium.

Public Markets. Public equity and credit investors with hyperscaler and cable-operator exposure should sequence Egypt into the regional map now.

The action is to calibrate the localization deadline and the licensing cadence as leading indicators of in-country capacity demand.

The cost of inaction is pricing the region off developed-market comparables and missing the demand inflection the compliance clock forces.

Operators. Data center developers and hyperscalers acting as buyers should read the licensing cadence as a closing window.

Ten licenses in two years signals a regulator moving fast and a corridor position that is being claimed.

The action is to negotiate interconnection and colocation positions before the localization deadline converts optional demand into forced demand and compresses the negotiating leverage of late entrants.

The cost of waiting is leasing capacity at deadline-driven pricing from the platforms that positioned early.

The Verdict

Egypt is being licensed into a market position before the demand that validates it has fully arrived, and the Hassan Allam and A15 authorization is the clearest instance of a private platform underwriting that timing gap.

The market inflection is the point at which the October 2026 localization deadline and the sequenced hyperscaler pipeline convert corridor optionality into contracted rent.

The platforms holding 15-year interconnection rights at that inflection capture the spread between an option struck early and demand priced late.

The open question is whether the power grid keeps pace.

Egypt underwrites this thesis on a surplus-electricity advantage, though its grid is still scaling for hyperscale load. The transit corridor is a durable asset.

The power to support what lands on it is the variable the next 24 months will resolve.