China Funded The AI Grid. The Chips To Fill It Do Not Yet Exist.

The $295B sovereign program, the SMIC fabrication ceiling, HBM packaging yields, the 80% domestic mandate, carrier-operator idle risk, the supply gap the capital cannot close

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

The Binding Constraint Is Fabrication, Not Capital

China has committed roughly $295 billion dollars over five years to a sovereign AI computing grid, and the capital is the part everyone is watching.

The capital is not the constraint.

The constraint sits one layer down, in a single domestic foundry running above 93 percent utilization at a node two generations behind the frontier, and in a domestic high-bandwidth memory packaging base that cannot yet yield at volume.

The program guarantees the money and guarantees the market. It cannot guarantee the silicon.

That gap, between funded demand and constrained supply, is the entire investment question, and the headline figure is built to obscure it.

Guaranteed Demand Is Not The Signal Investors Think It Is

The first read is that demand-side certainty has been engineered to an unusual degree.

State policy now requires any state-funded data center project to source at least 80 percent of its underlying technology domestically.

The May 2026 Anke certification converted that mandate into a procurement catalog, listing nine processors from seven domestic entities, with provincial bureaus and state-owned enterprises legally restricted to certified silicon.

This manufactures a captive market. It also concentrates risk.

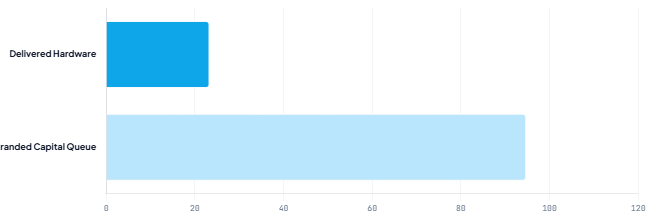

Demand certainty is only an asset if supply can meet it, and a guaranteed buyer for a chip that cannot be fabricated at volume is a queue, not a market.

For the next 12 to 24 months, the binding question is not whether demand exists.

The state has legislated that it does. The question is throughput.

The Anke List Is A Map Of Winners And A Map Of Exclusions

The second read is in who the certification names and who it omits. The Anke catalog certifies Huawei Ascend, Alibaba T-Head, Biren, Hygon, Iluvatar, MetaX, and Moore Threads.

It omits Cambricon and Baidu-backed Kunlunxin. Because state-owned facilities are legally restricted to certified silicon, omission is not a delay. It is exclusion from the procurement channel that drives the majority of high-end domestic demand.

Cambricon reported first-quarter 2026 revenue of 423 million dollars and strong growth, and is still outside the catalog.

The signal is that the certification list, not the market, now allocates demand.

For an investor in Chinese chip designers, the diligence question has changed: financial performance is secondary to catalog inclusion, because inclusion is the licence to sell into the only buyer that matters at scale.

Position on the list, not on the income statement.

Carrier-Operators Are A Structural Source Of Stranded Capacity

The third read is who builds and operates the grid. The state has tasked telecom carriers, China Mobile and China Telecom, with constructing and operating the bulk of the national facilities.

S&P Global Ratings notes that traditional carriers often lack experience building the high-power-density, low-PUE facilities that generative AI training requires.

The operators with a proven record of delivering optimized facilities for the private AI labs, the carrier-neutral providers, sit largely outside the sovereign funding flows.

This is a structural mismatch between who holds the capital and who holds the capability.

The consequence is concrete: state capital may fund facilities that cannot host the workloads they were built for, leaving local governments with debt against idle infrastructure.

The risk is not theoretical demand softness.

It is capable demand routed to incapable supply by the funding structure itself.

Investor Action

Private Capital. Infrastructure and private equity allocators evaluating exposure to China’s domestic chip and data center layer should underwrite the supply chain, not the program size. The diligence sequence runs through SMIC wafer allocation, HBM packaging yield, and Anke catalog position, in that order. A certified designer with no secured wafer allocation is a brand with a licence and no product.

The cost of underwriting the 295-billion-dollar figure as a proxy for deliverable capacity is that an allocator funds a queue and books it as an asset.

Price catalog inclusion and secured fabrication capacity as the value drivers; treat the headline program as context, not thesis.

Public Markets. Public equity investors hold the cleanest instrument to express this view, because the bottleneck is observable. SMIC capacity utilization, HBM packaging progress, and Anke catalog revisions are trackable signals, and they lead the buildout. Benchmark certified designers on secured wafer allocation rather than order books, because an order the foundry cannot fill is not revenue.

The Cambricon case is the template: strong reported growth, catalog exclusion, and a step-change in risk that the income statement did not show.

Position on the spread between certified-and-supplied and certified-but-unsupplied names and watch the certification list as the event that moves it.

Operators. Data center developers and the carrier-operators themselves face the execution risk directly. A facility built without the power density and PUE that AI training requires is a facility built into the idle tier, regardless of how much state capital funded it.

The carrier-neutral operators with the delivery record have the capability the sovereign grid needs and the funding access it does not extend to them.

The structural read is that capability and capital are misaligned by design, and the operators that close that gap, through partnership, mandate, or acquisition of capability, capture the workloads the carrier builds cannot host. Underwrite delivery capability as the scarce input, not capital.

The Verdict

China's sovereign computing program is the most fully funded and most fully mandated AI infrastructure buildout in the world, and that is precisely why the supply constraint is the story.

When demand is legislated and capital is guaranteed, the only variable left is whether the physical supply chain can deliver, and this one runs through a single foundry above 93 percent utilization, an immature HBM packaging base, and operators who may not be able to build what the workloads require.

The program targets full operational capability by 2031, a date chosen as strategic insurance against the decoupling it anticipates.

The open question for the next 24 months is whether SMIC and domestic packaging can scale fast enough to convert funded demand into delivered compute.

Or whether physical infrastructure outpaces the certified silicon available to fill it, leaving the grid as a funded promise waiting on chips.

Underwrite the bottleneck until the fabrication numbers say otherwise.