Behind the Meter Is the New Frontier in AI Power Procurement

Grid bypass is the structural advantage, stranded-gas monetization, ERCOT queue avoidance, the deliverable megawatt as the priced unit

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

The Grid Bypass Is the Signal, Not the Gas

Project Kilby is not a natural gas story.

It is a grid-disintermediation story, and the distinction governs how it should be underwritten.

The headline reads as a hyperscaler buying fossil power, which invites a carbon debate and a commodity-cycle frame.

The structural signal is that Microsoft and Chevron designed the project to operate entirely behind the meter, sidestepping ERCOT interconnection altogether.

Capital allocators who read this as an energy transaction will misprice it.

The asset being created is not a power plant.

It is a dedicated, dispatchable megawatt that reaches compute without touching a public queue.

Interconnection Avoidance Is Now a Priced Competitive Edge

The first read is that grid bypass has moved from engineering workaround to underwriting advantage.

ERCOT interconnection queues for large new loads are measured in years, and Texas ratepayer-impact politics have made large grid-connected data center loads contentious.

Project Kilby removes both variables by design.

Gustavson was explicit that the project does not compete with local electricity consumers, which is the political cover the off-grid structure buys.

For the next 12 to 24 months, the deals that clear fastest will be the ones that never ask the grid for permission.

Speed-to-power becomes the scarce input, and behind-the-meter structures are the only way to buy it at gigawatt scale.

The investor implication is that interconnection-queue position should now be diligenced as a first-order risk, not a procurement footnote.

The Stranded-Gas Engine Makes the Economics Replicable

The second read is that the supply side of this deal is a stranded-asset monetization play, and that is what makes the template repeatable.

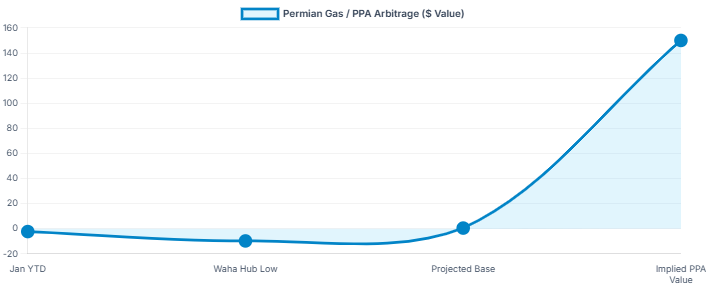

Waha Hub gas prices in the Permian have run negative for a record 47-plus consecutive days in 2026, averaging negative $2.29 per MMBtu year-to-date and reaching as low as negative $9.75.

Producers have been paying to dispose of associated gas that pipeline takeaway constraints cannot move to market.

Chevron converts that disposal liability into a 20-year contracted revenue stream against a creditworthy counterparty.

The structural point is that the input fuel carries a negative or near-zero opportunity cost, which is what supports a mid-teens IRR on a $7 billion to $9 billion build.

Any basin with stranded hydrocarbons and takeaway constraints the Permian, the Bakken now carries a latent version of this same trade. The model travels.

Engine No. 1’s Equity Option Is the Capital-Structure Tell

The third read is that the Joulent equity option is the most under-discussed structural element in the deal.

Engine No. 1, through Joulent LLC, holds a 50 percent equity option in a fossil fuel power project.

An ESG-positioned investor taking an equity position in behind-the-meter gas generation signals that the capital base for this asset class is broadening beyond traditional energy sponsors.

The structuring move bridges the equity gap and reshapes the political optics of a gas project simultaneously.

For the next 12 to 24 months, expect more crossover capital to underwrite these complexes, because the contracted-revenue profile reads as infrastructure, not commodity exposure.

The signal is that the buyer universe for energy-compute equity is wider than the energy-transaction frame assumes.

Investor Action

Private Capital. Infrastructure funds, private equity, and energy-transition vehicles should re-evaluate behind-the-meter generation as a contracted-cashflow asset class rather than a merchant power bet. The mandate fit is strong where a fund can underwrite 20-year offtake against a hyperscaler counterparty.

The action is to build diligence capacity on turbine procurement backlogs and stranded-gas basis economics now, because the first movers are placing turbine orders ahead of FID.

The cost of waiting is that GE Vernova and comparable turbine slots are already backlogged for years, and capital without an equipment position cannot execute on the timeline the model requires.

Public Markets. Public equity investors holding Chevron, Microsoft, GE Vernova, or Caterpillar should recognize that energy-compute integration is becoming a recurring earnings driver, not a one-off announcement.

The action is to benchmark which integrated energy majors have both the stranded-gas inventory and the balance sheet to replicate the structure.

Chevron entered 2026 post-Hess with record production of 3.86 million barrels of oil equivalent per day and debt-to-equity near 0.25, which is the balance-sheet profile that absorbs construction-phase capital.

The cost of inaction is missing the re-rating of energy names that successfully diversify into contracted utility-style earnings.

Operators. Data center developers and hyperscalers should treat Project Kilby as the new power-procurement template. Secure land near stranded-gas basins and generation partnerships before interconnection queues create multi-year delays.

Microsoft positioned the model as replicable, not bespoke.

The cost of waiting is that the best co-location sites large acreage adjacent to negative-basis gas and outside congested grid nodes are finite, and the operators who move first lock up both the land and the equipment.

The Verdict

Project Kilby marks the point where power procurement, not GPU access, becomes the binding constraint on AI infrastructure.

The market inflection is the shift from buying compute to securing the deliverable megawatt that feeds it, and the behind-the-meter structure is the first scaled proof that the deliverable megawatt can be manufactured outside the grid.

The replication risk cuts both ways: if the model travels as fast as its economics suggest, the advantage compresses to whoever secured turbines and acreage first.

The open question is whether the grid operators and regulators respond by accelerating interconnection or by contesting the off-grid model.

The answer determines whether behind-the-meter remains a premium structure or becomes the default one, and that resolution arrives well inside the 2028 first-power window.

I get it. What I don't get it what gets you around the Vernova or Siemens or Mitsubishi or Rolls Royce backlog and gets you a shiny new turbine ahead of everyone else? Can someone please explain...