Will Microsoft’s $50B India AI Bet Reshape Data Center Capital?

Microsoft’s $50B Global South strategy, anchored in India, marks a capital re-sequencing moment for AI infrastructure and emerging-market data center investment.

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Microsoft’s trajectory toward $50 billion in AI investment across the Global South by 2030, anchored by more than $20 billion in India alone, is not simply a regional expansion story. It is a capital re-sequencing event for global data center infrastructure.

India is the proving ground.

If this deployment model works at scale pairing hyperscale balance sheet strength with sovereign alignment and ecosystem buildout it will reshape how institutional capital allocates into emerging-market AI infrastructure for the next decade.

India as the Anchor Market

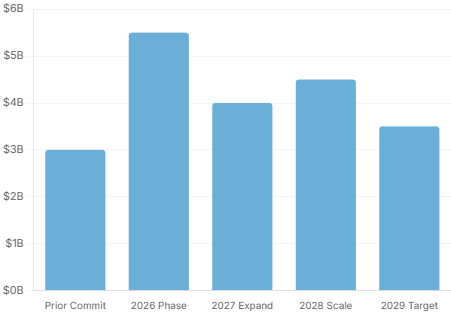

India anchors Microsoft’s program, with roughly $17.5 billion committed over 2026–2029 on top of a prior $3 billion, signaling multi-cycle confidence in demand growth and regulatory stability.

Its advantages are structural: one of the world’s largest developer bases, accelerating enterprise digitization, central policy support for AI and data localization, and a young demographic profile driving long-duration compute demand.

The deeper signal is ecosystem underwriting. Microsoft is not just adding capacity; it is investing in compute, skills, multilingual AI, and adoption measurement.

From an investor lens, this is ecosystem underwriting, not real estate expansion.

The Shift in Capital Formation

Historically, institutional capital entered emerging markets after stabilization. Hyperscalers leased, developers pre-leased, and funds acquired operating assets at yield. Capital followed certainty.

That sequencing is shifting. Microsoft’s balance sheet is absorbing early development risk land, power, construction where investors once required de-risked cash flow. A three-stage model is emerging: hyperscaler deployment, sovereign co-investment, then institutional rotation after utilization stabilizes.

Investors who wait for the final stage will face compressed auctions. Those who enter earlier assume execution risk but gain governance influence and pricing leverage.

India demonstrates that sovereign-aligned early capital can be strategic, not speculative.

Investment Structures Emerging in India

Distinct structures are becoming repeatable in the Indian market, reflecting a shift from speculative development toward contract-driven deployment.

Platform equity joint ventures between hyperscalers and local strategic partners align regulatory navigation with operational execution. Build-to-suit programs tied to long-term AI workloads from enterprises and public institutions improve revenue visibility and demand certainty.

Staged development financing where modular capacity ramps are triggered by utilization thresholds reduces stranded capital risk. At the same time, sovereign cloud configurations with localized governance controls address data residency and cybersecurity requirements.

Collectively, these structures shift underwriting away from lease-rate assumptions toward regulatory durability, power certainty, and ecosystem depth.

Power as the Primary Underwriting Variable

If India reshapes capital flows, it will be because investors recalibrate how they underwrite risk. The dominant constraint is not capital. It is power.

AI workloads increase rack density and intensify load profiles, making transmission bottlenecks and generation alignment the true gating factors. Underwriting a facility without firm interconnection timelines or stable procurement structures is insufficient.

Investors must prioritize grid certainty, energy mix stability, behind-the-meter optionality, and state-level utility alignment. A 20MW campus without secured power is not infrastructure it is a development liability. When power becomes the core asset, valuation frameworks and capital structures adjust accordingly.

Demand Underwriting Beyond Headlines

India’s developer density implies strong demand elasticity, but installed capacity does not guarantee utilization.

Institutional capital should anchor underwriting to measurable signals: enterprise AI adoption across key sectors, growth in domestic AI startups and open-source output, and public-sector digital budget commitments. Compute supply must align with application-layer expansion.

Microsoft’s five-part program reflects this reality. Without ecosystem density, assets underutilize and returns compress. India’s edge is not population scale alone it is usage velocity.

Sovereign Alignment and Digital Control

India’s regulatory stance on data localization and digital sovereignty has directly shaped investment structures. Sovereign cloud configurations and localized governance frameworks are not optional they are prerequisites for market access.

Foreign investors must recalibrate control expectations. Hybrid governance models, transparent compliance systems, and alignment with national AI strategies reduce regulatory volatility and political friction.

While hyperscalers with scale can negotiate from strength, mid-market operators and infrastructure funds must structure partnerships deliberately. In AI-sensitive sectors, purely foreign-controlled models will face structural resistance.

Competitive Capital Dynamics

Microsoft is not operating in isolation. Other hyperscalers and regional platforms are expanding across India and Southeast Asia, while infrastructure funds evaluate minority equity, preferred structures, and private credit exposure.

The competition is no longer centered on capacity alone but on power access and policy alignment. Capital that can move decisively, structure joint ventures, and align with sovereign frameworks will secure premium positions.

Those that hesitate will inherit secondary sites and thinner spreads.

Risk Allocation Framework

Investing alongside hyperscale AI expansion in India introduces layered risk: high-density construction execution, currency exposure, regulatory evolution, power price volatility, and monetization pacing.

These risks are investable when structured deliberately. Indexed pricing can mitigate currency mismatch, take-or-pay agreements reduce demand uncertainty, layered capital stacks absorb construction volatility, and political risk insurance buffers regulatory shocks.

Phased capacity deployment limits overbuild. The distinction between speculation and infrastructure lies in contract architecture.

The Takeaway

Microsoft’s $50 billion commitment is less about India itself and more about capital sequencing. Hyperscalers are absorbing early-stage development risk in sovereign-aligned AI markets, shifting the traditional entry point for institutional infrastructure capital.

India is the template. If utilization and regulatory durability hold, similar models will extend across other high-growth markets. Power security, ecosystem depth, and sovereign alignment will determine where capital flows.

Funds that wait for stabilized yield will face compressed spreads. Those that enter during hyperscaler-led buildout assume greater execution risk but gain governance leverage and pricing advantage. Timing is the strategic variable.