Why Transmission Bottlenecks Are Rewriting the AI Data Center Playbook

Grid congestion is quietly becoming the #1 reason AI-ready data centers stall, impacting timelines, trapping capital, and stranding energy in every region.

Welcome to Global Data Center Hub. Join 1400+ investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Executive Summary

Grid congestion has become the defining constraint for data center investors globally.

More than 2,600 GW of energy and storage projects are stuck in interconnection queues across the U.S., twice the size of the entire national grid.

AI workloads are outpacing grid readiness, with rack power demands rising from 8–15kW to 80–100kW+.

Transmission, not generation, is the new limiting factor for digital infrastructure.

Even with signed PPAs and leased facilities, many projects can’t go live due to overloaded substations and multi-year transmission delays.

Clean energy is being curtailed. Carbon targets are slipping. IRRs are quietly collapsing under the weight of “invisible delays.”

Smart capital is shifting from “power-secured” to “grid-connected” strategies.

What’s Happening

There’s no shortage of clean energy.

What’s missing is the path to deliver it.

In today’s AI-driven economy, power isn’t useful unless it’s available where and when it’s needed at hyperscale, with reliability, and with transmission already secured.

But here’s what’s breaking:

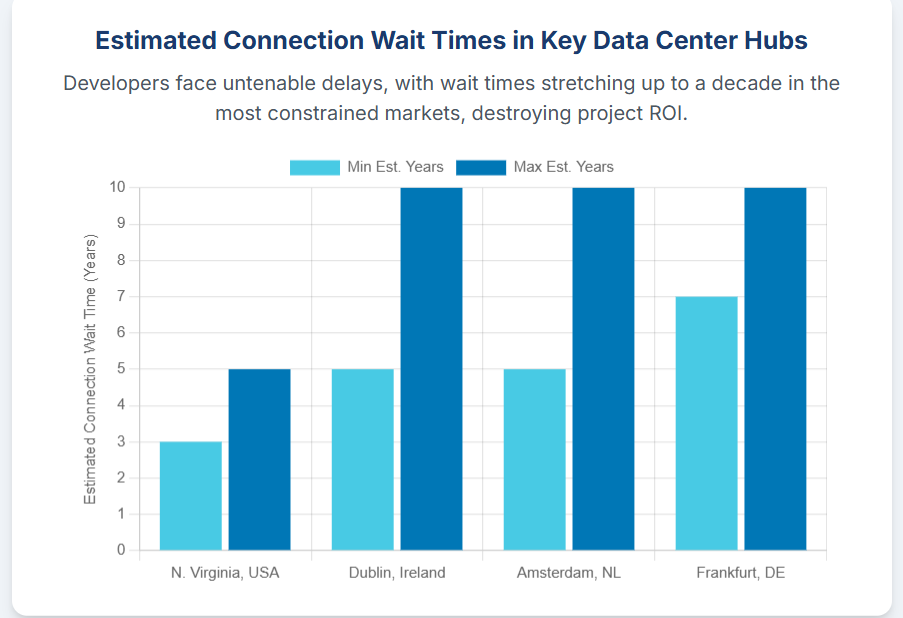

Interconnection delays: 2,600 GW in queue in the U.S. alone. Many projects face 5–10 year timelines.

Curtailment: In 2024, California alone curtailed 3.4 million MWh of solar power, up 29% year over year.

Regional overload: Markets like Northern Virginia, West London, and Amsterdam are turning away new grid applications due to saturation.

Investor confusion: Signed renewable PPAs are being undercut by curtailment, stranded generation, or unfulfilled interconnection.

We are now in a world where you can have land, power contracts, demand, and tenants…but still fail.

Because you didn’t control the wires.

Why It Matters

Grid congestion isn’t just a technical problem, it’s a major financial issue.

For years, investors treated power as a binary: either a site had access or it didn’t. But in the age of AI and clean energy transition, that view is dangerously outdated. The real question is: how soon, how stable, and how scalable is your access? And in more and more markets, the honest answer is: not very.

Here’s what that disconnect is doing to the data center investment landscape:

1. Transmission Bottlenecks Are Silently Impacting Returns

Thousands of data center megawatts are now sitting idle, not for lack of demand, tenants, or equipment, but because they can't plug into the grid. These aren’t theoretical delays. They are measurable, compounding costs that impact internal rates of return (IRR) and push projects outside their original underwriting parameters.

Every month in the interconnection queue means more interest carry, delayed revenue, and eroding confidence among capital partners. And yet most models still assume 24–36 month delivery timelines, ignoring how a single point of failure, like a delayed substation upgrade, can turn a viable project into a write-down.

2. Curtailment Risk Is Undermining the Clean Energy Narrative

A growing number of operators are discovering a hard truth: signing a green PPA is not the same as delivering green power to your racks.

In California, 3.4 million megawatt-hours of solar energy were curtailed in 2024 alone. That’s energy that was generated but never used, wasted because the grid was too congested to deliver it. This breaks the sustainability thesis that many investors, governments, and tenants are relying on. When electrons can't move, your carbon reduction strategy becomes a branding exercise instead of a reality.

For ESG-focused funds, this is particularly dangerous. Portfolios with high exposure to curtailed renewables or grid-constrained zones will start underperforming against their own decarbonization benchmarks and risk losing LP trust in the process.

3. AI Loads Are Forcing a Rethink of Power Planning

The power profile of AI workloads is fundamentally different from what traditional colocation infrastructure was built for. It’s not just about more power, it’s about continuous, high-density, high-availability power with minimal tolerance for instability or dropouts.

This demand curve doesn’t match well with current grid dynamics or renewable generation peaks. And when you combine AI's 24/7 flat load with solar's midday spike and wind’s volatility, the outcome is a structural mismatch that neither utilities nor developers have fully resolved.

The result? More reliance on fossil backups, higher emissions, and greater regulatory risk, right as AI infrastructure becomes central to economic competitiveness.

4. Delays Are Now Embedded in the System

Permitting timelines for new transmission projects can stretch beyond a decade. Grid interconnection studies are backlogged. Even when a project is approved, transformer and switchgear lead times can add 18–24 months of delay.

That means even the best-laid development plans are at the mercy of an overloaded and underbuilt grid and every delay carries cost. But because these are infrastructure delays, not construction delays, they are often invisible in initial models.

This is what makes grid congestion so dangerous: it doesn’t appear on the critical path until it’s too late.

5. Emerging Markets Have Speed, but Face Fragility

In India, Brazil, Nigeria, and Southeast Asia, developers are bypassing legacy designs and going straight to AI-ready builds. That’s a competitive advantage. But transmission infrastructure is often underdeveloped, poorly mapped, or prone to political interference.

Power may be abundant, but the ability to deliver it, especially under hyperscale AI loads, is still constrained. These regions risk becoming “paper hubs”: fully designed campuses with land, plans, and tenants… but no way to turn the lights on.

The lesson for global investors is clear: the old playbook, land, then power, is broken. In this cycle, the power must flow first. Otherwise, you’re not developing a data center. You’re buying expensive dirt with a substation problem.

What This Means

For Investors: Power Access Must Be Priced Like Power Risk

The following sections are for premium subscribers only:

What This Means: Strategic implications for investors, operators, and policymakers.

Already a paid subscriber? Read on below.

Capital has spent the last five years chasing “power availability.” But too often, availability has been confused with accessibility. In this new reality, you don’t just need electrons you need electrons that flow on time, at scale, and without congestion penalties.

This means shifting from “secured PPA” thinking to “deliverable energy” thinking.

Most underwriting models still assume flat, linear access to grid power within 18–24 months. That assumption is outdated. In congested markets like Virginia, California, or São Paulo, that access can stretch beyond 5 years and your IRR gets impacted during that wait.

Transmission risk is now a core variable in:

Discounted cash flow projections

Terminal value assumptions

Sponsor selection

Market entry decisions

Failure to price this risk accurately is the new version of assuming rent escalations in a flat market, it looks good in Excel and explodes in reality.

Smart capital is already shifting to transmission-aware underwriting frameworks: applying curtailment discounts to PPAs, modeling 3–10 year interconnection delays, and assigning value premiums to sites with existing substation headroom or co-located generation.

If your site is in a congested region and doesn't already have a signed interconnection agreement, or at least guaranteed queue position, it’s not worth your 20x multiple. It’s a gamble with no insurance.

For Operators: Design with the Grid, or Get Left Off It

Operators can no longer treat the utility interface as a late-stage checklist item. In a congested grid, your interconnection plan is your go-to-market strategy.

If your facility depends on future upgrades to substations or new transmission lines that haven’t cleared permitting, you are not three years from go-live. You are five to seven. Maybe ten.

This changes how facilities must be designed from day one.

Successful operators are adapting by:

Siting next to generation (solar, wind, hydro, nuclear) and bringing power on-site.

Using modular switchgear and power systems to phase in delivery in 5–10MW increments while waiting on full interconnection.

Building in flexible battery storage (BESS) to ride through curtailment or grid failure events.

Becoming grid assets, not just grid consumers, by participating in demand response programs and ancillary services markets.

The best operators now show up to hyperscaler RFPs with a grid-flex strategy, not just a location map.

If you’re not embedding this into your pitch deck or bid response, someone else is.

For Policymakers: Transmission Is Now National Competitive Infrastructure

This is no longer just a private sector bottleneck. It’s a sovereignty issue.

In the same way that countries once competed for automotive plants or semiconductor fabs, they are now competing to become AI and cloud infrastructure hubs. But if your grid is congested, no matter how much land or fiber you offer, you’re losing.

Capital will flow to where electrons flow.

And yet, in most countries, transmission permitting remains slower than generation buildouts, and grid planning remains reactive rather than strategic.

Governments serious about attracting hyperscale and cloud investment must act decisively:

Streamline permitting for transmission upgrades and interconnections.

Publish grid-readiness heatmaps and queue transparency portals to inform investor decisions.

Introduce “Digital Infrastructure Zones” with bundled incentives for grid, fiber, and land development.

Fund public-private partnerships to develop shared substations or interconnection corridors.

Reclassify AI-ready data centers as strategic energy infrastructure, allowing them access to priority permitting lanes.

Countries that take grid congestion seriously, and treat it as a barrier to national innovation, not just utility expansion, will win billions in private capital and long-term economic leverage.

Those that don’t will simply become markets of last resort.

The Bottom Line

Grid congestion is no longer a niche power issue.

It’s a capital formation issue. A growth bottleneck. A national competitiveness test.

You can’t build the future if you can’t plug it in.

In 2025 and beyond, the most valuable infrastructure won’t be the one with the cheapest land, or the largest campus…it’ll be the one that flows electrons first.

Transmission is the new moat.