How Private Capital Is Rewriting The Data Center Playbook

Equinix, Digital Realty, DuPont Fabros, CoreSite, the capex-distribution paradox, the post-REIT capital architecture

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

The REIT wrapper is not the permanent capital architecture for data centers.

It was built for office buildings.

It was adapted to data centers.

It was never built for them.

The market reads the data center REIT as the mature form of the asset class.

The read is wrong.

The marginal dollar of digital infrastructure capital has already moved.

Allocators pricing the next cycle against REIT-era comps will miss the velocity of the capital now scaling outside the public market.

The 2017–2021 consolidation wave made the pattern clear.

Digital Realty bought DuPont Fabros for $7.6B.

American Tower acquired CoreSite for $10B+.

Blackstone took QTS private for $10B.

Three deals.

One verdict: the REIT model had run its course.

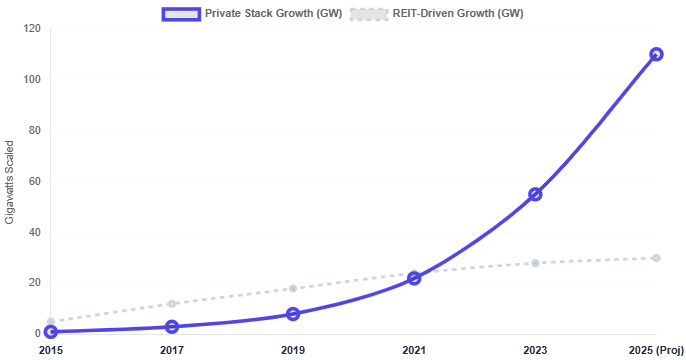

The next capital architecture is already in place.

Hyperscale JVs.

Sovereign-backed funds.

Private credit.

xScale-style vehicles.

Outside the REIT perimeter and scaling faster than the REITs that built the platform.

How The Wave Was Built

The wave was built on dot-com wreckage.

By 2001 the U.S. had a graveyard of purpose-built data centers: bankrupt ISPs, abandoned platforms, and assets trading at 20–40% of replacement cost.

GI Partners saw the arbitrage.

Acquire the physical assets at distressed prices. Stabilize occupancy. Take the platform public.

The public market would pay a premium for an operating REIT over a collection of buildings.

Digital Realty listed in November 2004 (~$240M).

DuPont Fabros followed with a $640M REIT IPO tied to Northern Virginia hyperscale leases.

CoreSite raised $270M in 2010. Equinix stayed a C-corp until converting to REIT status in 2015.

The thesis was simple.

Data centers looked like rent long leases, strong tenants, predictable cash flow.

The REIT wrapper added tax efficiency, institutional inflows, and a valuation premium over tech C-corps.

The cohort scaled it.

Digital Realty kept raising capital.

Equinix acquired IXEurope (2007) and Switch and Data (2010) using public markets while avoiding REIT constraints.

By 2010, data centers were a recognized institutional asset class.

The Capex-Distribution Paradox

The narrative has focused on the REIT as the stable vehicle for institutional data center capital.

The narrative misses the structural constraint.

Data centers depreciate on five- to seven-year refresh cycles.

The REIT requires 90% of taxable income to be distributed annually, leaving near-zero retained earnings.

Every upgrade and expansion must be externally financed. Cost of capital becomes the binding constraint on growth velocity.

2008 was the stress test.

When credit markets seized, DuPont Fabros halted construction simultaneously across every active development site.

Demand was strong. Leases were signed.

The company could not access the capital required to continue building.

That was not a business failure. It was a capital structure failure written into the REIT form itself.

This inability to sustain capex through cycles reinforces the structural constraint outlined in The AI Data Center Crisis No One Is Talking About.

Operators, PE, Public Equity

Independent operators face the specification problem.

AI workloads require 50–100 kW racks, while most REIT-era facilities were built for under 15 kW.

Retrofitting demands capital the REIT structure cannot retain. Operators dependent on public equity cycles fund upgrades at market discretion, not their own.

Private equity and infrastructure investors face a different constraint.

The REIT model compounds, cyclical issuance works above NAV, but shuts in downturns.

Private capital with long hold periods and no distribution mandate compounds through cycles.

The Blackstone $10B QTS take-private is the template, not the exception.

Public equity investors face a structural shift.

Wholesale REITs have consolidated, interconnection is concentrated in Equinix, and AI demand is moving toward private captive builds.

The public REIT is no longer the default entry point for digital infrastructure exposure.

As AI demand shifts toward private, captive builds, the public REIT loses its position as the default access point, a transition explored in The Self-Build Surge Will Not Kill Colocation. It Will Split It.

The Capital Stack The REIT Could Not Provide

The next capital architecture is already visible.

Private hyperscale JVs.

Sovereign funds.

Private credit.

Asset-backed securities.

Hybrid structures keep REIT income assets while routing capex-heavy development into private vehicles outside the 90% mandate.

This is not refinement it is a supplemented REIT model the public market cannot fund alone.

The implication for emerging markets is direct. Southeast Asia, Africa, and Latin America cannot replicate the 2004 to 2010 playbook.

Legal framework does not exist. Public capital depth does not exist.

Distressed asset base that made the original wave possible does not exist.

Capital architecture for emerging market data center development is private from the first dollar.

Development finance institutions, sovereign funds, and deep-pocketed private equity must carry the load that in the U.S. was carried by public REIT markets.

The Velocity Allocators Are Mispricing

The allocators who underwrite the next cycle against a REIT-era template will misprice the velocity.

The allocators who structure private, flexible, long-duration vehicles outside the distribution mandate will capture the scale.

The first movers have already moved.

The cost of waiting is measured in the gigawatts being built, leased, and priced by the capital that does not need to wait for the next equity window to open.