Why Microsoft's $329M in South Africa Is a Grid Underwriting, Not Capacity Growth?

Hyperscaler capital allocation, power and water resilience underwriting, sovereign AI infrastructure, emerging market DC sequencing, Johannesburg and Cape Town buildout, Global South compute architect

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Microsoft is not expanding South African cloud capacity.

It is underwriting grid risk at hyperscaler scale.

The line item sits inside the $329 million disclosure from last week.

The market is reading it as capacity growth.

The reading is wrong.

The investors who keep pricing South Africa on sovereign grid reliability will watch hyperscaler capital sequence into markets they already wrote off.

Timeline matters.

Brad Smith committed ZAR 5.4 billion in March 2025 alongside President Cyril Ramaphosa.

Microsoft detailed the allocation last week.

Three categories surfaced: land for future campuses, expanded capacity in Johannesburg and Cape Town, and power and water readiness for existing regions.

The third category is the story.

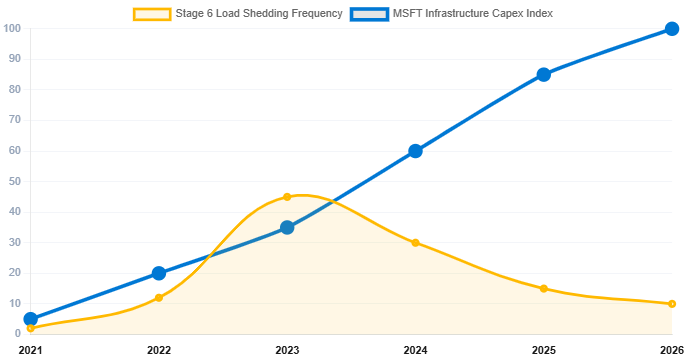

Three Years Pricing Eskom

Microsoft entered South Africa at scale in 2022.

It stood up the continent’s first enterprise-grade cloud regions in Johannesburg and Cape Town.

The prior ZAR 20.4 billion commitment funded the buildout across three years. Eskom’s grid crisis ran the same three years. Stage 6 load shedding peaked in 2023.

National blackouts persisted for months.

Every serious operator in the country spent that period pricing grid risk into capital plans.

Microsoft is the first hyperscaler to allocate a visible external-facing line item to solving it upstream.

Why the Allocation Is Asymmetric

Calibrate the figures.

Microsoft’s global data center capex ran approximately $80 billion across fiscal year 2025.

Its Global South commitment totals approximately $50 billion. The targets include India, Brazil, and Africa.

South Africa is the smallest by absolute capital.

It is also the only one where the binding constraint is grid reliability rather than land, permitting, or sovereign risk.

The allocation to power and water readiness is therefore asymmetric. It confirms the decision.

Microsoft will solve the constraint directly. It will not wait for Eskom. It will not wait for the sovereign.

The Market Is Reading This Wrong

The narrative has focused on Microsoft as a gateway investor in African AI infrastructure.

That framing misses what the capital is doing.

The capital reality is a new template.

In the old template, the sovereign delivers power. In the new template, the hyperscaler funds resilience directly and lets sovereign capacity catch up.

The shift is durable.

Every competing hyperscaler now has to decide whether to match it.

The ones that do not match will cede the continent for the investment cycle.

This inversion of responsibility between sovereign infrastructure and private capital reflects the systemic breakdown analyzed in Infrastructure Misalignment: The Hidden Crisis Collapsing Data Center Deals.

Three Investor Lenses, One Specification

Start with the independent operator lens.

Teraco. Smaller regional platforms.

Each has spent years diligencing power and water readiness as a qualification constraint and now faces hyperscaler-grade uptime demands against an unreliable grid.

Microsoft just set the specification.

Operators that cannot match site-level resilience investment will lose the tenant mix funding AI workloads.

The qualification bar has moved.

The private equity and infrastructure lens sharpens underwriting.

Sovereign grid risk was priced as a discount to returns.

If hyperscalers fund the resilience layer directly, risk shifts.

Sponsors underwrite revenue against resilient capacity, not Eskom reliability.

The constraint moves to co-investment against hyperscaler specs changing deal structures, returns, and counterparties.

The public equity lens becomes competitive.

NTT, Equinix, Digital Realty.

Each must decide: match the capital commitment and compete for the next wave of African expansion, or cede and accept hyperscaler primacy across South Africa, Nigeria, Kenya, and Egypt.

The market has not priced this yet.

Demand-Side Infrastructure, Not CSR

The AI skills layer is the second-order signal most analysts are missing.

Microsoft’s January 2026 partnership with the South African Broadcasting Corporation integrated AI fluency modules into SABC Plus.

The platform reaches 1.9 million users.

The Lelapa AI partnership builds multilingual language models for African languages.

These are not corporate social responsibility line items.

They are demand-side infrastructure.

Microsoft is building the consumption base for the AI workloads the new capacity will run.

Hyperscalers that compete on infrastructure alone without the demand-side ecosystem will find compute sitting idle against a market that has not learned to consume it.

This integration of demand creation with infrastructure deployment reflects the broader strategic shift outlined in The Neocloud Is Not Overflow. It Is the Third Pillar of AI Infrastructure.

The Sequencing Is Already Set

Sequencing is what happens next.

Nigeria, Kenya, and Egypt all have enterprise demand sufficient for hyperscaler-scale capital, but each faces different constraints:

Nigeria has power scarcity and FX volatility, Kenya has grid stability with connectivity limits, and Egypt carries sovereign and currency risk.

The South African template shows hyperscaler capital only enters where the investor funds the resilience layer directly.

Investors assuming sovereign infrastructure will mature first will miss the capital window.

Microsoft moved first.

Those waiting for further confirmation in South Africa will pay 2028 prices for 2026 positions.

Capital is already sequencing, and the template is already set. The only question is who matches it and who gets priced out for the rest of the decade.