Why Hut 8 $3.25B Bond Becomes The AI Data Center Debt Template

Construction-stage investment grade, hyperscaler credit anchor mechanics, non-recourse SPV economics, NNN lease structure, project finance for AI capacity, emerging market replicability

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

The Signal Is The Structure, Not The Size

The $3.25 billion at the top of the press release is not the structural signal in this transaction.

The structural signal is that Hut 8 priced an investment-grade construction-stage bond on a single-sponsor data center asset by routing the credit risk through Google.

The market read this as a Hut 8 milestone.

The structural read is that the cost of capital for AI infrastructure has just bifurcated.

Assets with hyperscaler-grade backstop on the offtake side now access long-duration IG debt at construction. Assets without that backstop do not.

Read as a Hut 8 milestone, the transaction is the credit-market expression of the infrastructure shift that already priced most investors out. Hyperscaler-backstopped assets access long-duration IG debt at construction. The rest do not.

What Was Underwritten Was Google Credit, Not Hut 8 Credit

Both S&P and Fitch assigned BBB- to a project that has not energized a single megawatt.

The rating rests on two layered mechanics. The 15-year triple-net lease with Fluidstack carries a Google guarantee that includes novation rights inside the first six years and a springing Alphabet guarantee that activates if Google revenue falls below 50% of consolidated Alphabet revenue.

The financial product the bond market priced is Google credit dressed in a project finance wrapper. This compressed required DSCR to 1.32x average, far thinner than traditional infrastructure project debt would tolerate without a credit anchor of that quality.

The replicable lesson is not that data center construction can reach investment grade.

The replicable lesson is that hyperscaler-grade lease guarantees can underwrite construction-stage IG paper. Anyone diligencing the next AI data center bond should evaluate the offtake credit before evaluating anything else.

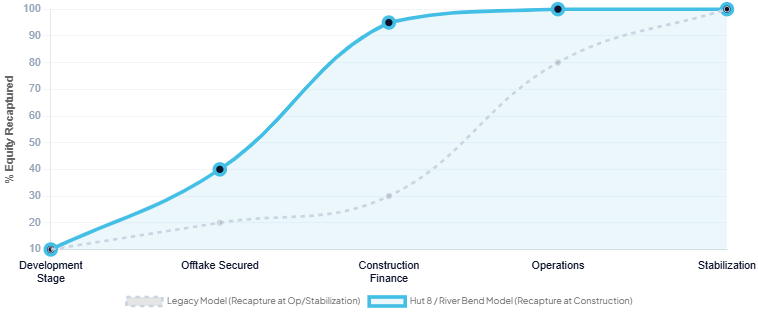

The Equity Recovery Distribution Reveals A New Developer Economics Model

Approximately $184 million of bond proceeds returned to Hut 8 Corp. as reimbursement of prior equity contributions.

This is the structural feature most likely to be missed in coverage focused on the headline figure.

The non-recourse SPV structure allowed Hut 8 to underwrite construction risk with equity, secure a hyperscaler-grade lease, monetize the contracted cash flows in the bond market at construction stage, and recover equity at financing rather than at operations.

The capital recycling cadence collapses by years. Developers no longer need to hold assets through stabilization to recover equity.

The implication for institutional capital structuring AI infrastructure deals is that developer equity becomes a 12-to-24-month bridge rather than a 5-to-7-year hold. Funds calibrated to the longer hold need to recalibrate underwriting and benchmark allocations.

The 1.32x DSCR Is The Floor That Required A Hyperscaler Anchor

Fitch’s rating case forecasts an average DSCR of 1.32x and a minimum of 1.31x across the lease term.

Traditional infrastructure project finance for greenfield assets typically requires 1.40x to 1.60x coverage to clear IG without a credit anchor.

The 1.32x at this rating level signals what the credit committees actually rewarded. The strength of the Google guarantee compressed the coverage requirement by approximately 8 to 28 basis points of DSCR cushion.

Markets and counterparties without an equivalent backstop should expect higher coverage requirements, shorter tenors, or higher coupon spreads. The 6.192% coupon, approximately 213 basis points above benchmark, is therefore a benchmark for assets backed by AA+ offtake credit. It is not a benchmark for assets backed by anything else.

Counterparties without equivalent backstops face higher coverage, shorter tenors, or wider spreads. The 6.192% coupon (~213 bps above benchmark) prices only AA+ offtake credit. The rest of the $121 billion US data center lending pool reprices against a different standard.

Investor Action

Private Equity and Infrastructure Funds should re-benchmark cost of capital assumptions for contracted AI data center assets. The River Bend structure now sets the pricing ceiling for hyperscaler-backed construction debt, and funds holding pre-template return assumptions will be outcompeted.

Public Markets Equity Investors should re-rate operators with IG-eligible pipelines. Contracted infrastructure cash flows now trade in a different valuation regime than legacy compute or mining exposure, and blended multiples are increasingly misaligned with asset reality.

Data Center Operators should reassess whether to hold assets or recycle capital through recap-and-return structures. Those with hyperscaler-grade leases can return equity at construction; those without face structurally higher capital costs and longer hold periods.

The Verdict

The Hut 8 transaction marks the point at which AI data center capital formation enters the investment-grade infrastructure debt market.

The market inflection is the bifurcation of cost of capital between assets that can produce a hyperscaler-grade lease backstop and assets that cannot.

Over the next 12 to 24 months, expect a wave of single-sponsor IG construction bonds priced against the River Bend template, concentrated in OECD markets where Google-equivalent guarantees can be assembled.