Why Did Nscale Secure a $1.4B GPU-Backed Loan Across Europe?

The Rise of Hardware-Backed Private Credit in Europe’s AI Infrastructure Expansion

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

UK-based AI hyperscaler Nscale signed a $1.4 billion GPU-backed Delayed Draw Term Loan to finance large-scale AI compute deployments across Norway, Portugal, Iceland, and the UK.

This transaction is not simply a capital raise. It marks the institutionalization of hardware-backed AI credit in Europe, signaling that GPUs are no longer just operating inputs they are now balance sheet assets.

The critical question is not why $1.4 billion, but why now, and why this particular structure.

Equity First, Debt Second

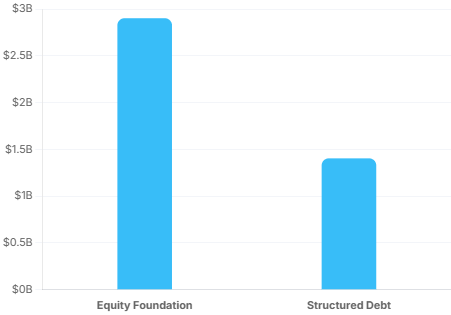

Before introducing GPU-backed leverage, Nscale raised approximately $2.9 billion in equity and SAFE capital across its seed, Series A, Series B, and pre-Series C rounds. This sequencing is deliberate.

Equity absorbed platform formation risk, funding land control, power interconnection rights, joint venture alignment, anchor customer negotiations, and engineering capabilities. These risks are unsuitable for credit capital. Only after partially de-risking the business did Nscale layer in $1.4 billion of structured debt.

This emerging AI infrastructure capital stack follows a disciplined logic: equity absorbs development uncertainty, contracts validate demand, power confirms deliverability, and debt funds hardware deployment. Credit follows discipline it does not create it.

GPUs as Institutional Collateral

Traditional data center underwriting has focused on long-term leases and real estate-backed infrastructure. AI-native facilities shift the collateral focus from shell to silicon.

GPUs are high-value, globally liquid, and increasingly contract-linked assets. They can be monitored in real time, with utilization and operational status verifiable daily. This transforms compute clusters into financeable industrial equipment.

The underwriting framework resembles equipment finance more than stabilized real estate. However, hardware-backed lending only works when revenue is contracted. Without firm offtake, GPU-backed debt becomes exposed to rental rate volatility. Collateral value must be supported by cash flow, not just resale assumptions.

Why the Delayed Draw Structure Matters

The facility is structured as a Delayed Draw Term Loan, meaning Nscale does not receive the full $1.4 billion at closing. Funds are drawn as GPUs are purchased and deployed, materially improving capital efficiency.

For the operator, this reduces negative carry and prevents idle balance sheet drag. For lenders, it aligns funding with revenue-generating milestones and improves loan-to-value monitoring during ramp.

The delayed draw feature embeds risk calibration into the structure itself, tying leverage to execution pacing rather than headline ambition. In a sector prone to overbuild risk, that alignment is critical.

Power Remains the Core Variable

Despite GPU-backed collateral, power remains the main constraint for AI infrastructure. Nscale chose markets with abundant, reliable renewable resources: Norway and Iceland offer hydro and geothermal energy with stable grids.

Portugal provides renewable growth potential under supportive regulation, while the UK adds proximity to enterprise demand and AI policy support.

Investors must evaluate megawatt delivery, interconnection timelines, and curtailment risk. Any shortfall can quickly compress hardware-backed leverage, making AI debt fundamentally energy-constrained.

Investor Fit and Diligence Requirements

GPU-backed lending is not a standard infrastructure product. It fits private credit funds seeking yield, sovereign wealth funds targeting strategic AI exposure, and infrastructure credit platforms with deep technical expertise.

It is less suitable for investors expecting long-term stabilized cash flows or lacking knowledge in hardware depreciation and telemetry enforcement.

Due diligence is critical. Investors must assess chip generation risk, residual value, market liquidity, customer concentration, telemetry systems, and sponsor equity. This is industrial equipment finance layered onto energy-constrained infrastructure, requiring technical underwriting rather than generic credit analysis.

The Obsolescence Risk

The primary structural risk is technological obsolescence. AI chips evolve rapidly, rental rates can compress quickly, and new generations can materially alter residual value assumptions. This volatility must be incorporated into loan structures.

Credit must be calibrated with conservative initial loan-to-value ratios, dynamic monitoring triggers, short tenors, and meaningful sponsor equity beneath the debt. If GPU-backed loans are structured like stabilized real estate debt, risk is mispriced. Treated like commodity electronics, contractual durability is underweighted.

The correct framework is hybrid: these assets behave like industrial machinery with demand cycles closer to software markets than traditional infrastructure.

Strategic Implications for Europe

This transaction has implications beyond a single balance sheet. Historically, hyperscale compute has been US-dominated, leaving Europe dependent on slower capital formation and foreign cloud platforms. Hardware-backed private credit accelerates domestic AI capacity without waiting for hyperscaler pre-leases.

Structured GPU debt acts as a tool for industrial scaling, enabling faster deployment of sovereign compute capacity while preserving sponsor ownership.

If this model becomes standard, Europe’s AI infrastructure expansion will increasingly rely on private credit markets rather than solely on venture equity or hyperscaler balance sheets..

The Broader Capital Stack Shift

Data center finance has traditionally focused on land, shell, and power. AI-native finance is changing that focus, emphasizing chips, clusters, and utilization telemetry as core assets.

Nscale’s $1.4 billion GPU-backed Delayed Draw Term Loan illustrates this shift. The transaction is not just large it signals that hardware itself is becoming a primary anchor for financing AI infrastructure.

Investors who master hardware-backed leverage under power constraints will drive Europe’s next phase of AI infrastructure, while those fixated on headline numbers risk missing the deeper structural shift.