What Anthropic's $100B AWS Commitment Signals For AI Infrastructure Capital

Anchor tenant economics, 10-year spend tenor, 5GW ceiling, Trainium validation, Project Rainier expansion, hyperscaler anchor competition, emerging market inference corridors 11

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

The $100B Is The Signal

Anthropic’s $100 billion pledge to spend on AWS over the next decade is the structural signal.

Amazon’s $33 billion equity commitment is the distraction.

The market has fixated on the check Amazon wrote and missed the contractual demand Anthropic agreed to deliver in return.

Capital allocators underwriting AI infrastructure on speculative demand will pay later for capacity already absorbed.

The Valuation Discount Is The Price Of Contractual Demand

Amazon negotiated the $5 billion fresh equity at a $350 billion pre-money valuation.

Anthropic’s February 2026 funding round closed at $380 billion. Other investor offers reportedly exceeded $800 billion.

Amazon priced its position below market and well below the highest reported bid.

The discount is not accidental.

It is the structural compensation Anthropic accepted in exchange for AWS being designated the primary provider for mission-critical training workloads under a ten-year, $100 billion commitment.

The structural read is that contractual demand at this scale is now a more valuable currency than equity premium.

Over the next twelve to twenty-four months, frontier labs may negotiate similar discount-for-anchor arrangements with hyperscalers.

The relevant evaluation is no longer equity into a frontier lab against equity into the next frontier lab.

The relevant evaluation is equity into a frontier lab against contractual compute commitments at hyperscaler scale.

This trade-off between valuation and contracted infrastructure access mirrors the financial logic outlined in Is CoreWeave’s $8.5B Deal the GPU Asset Class Moment?.

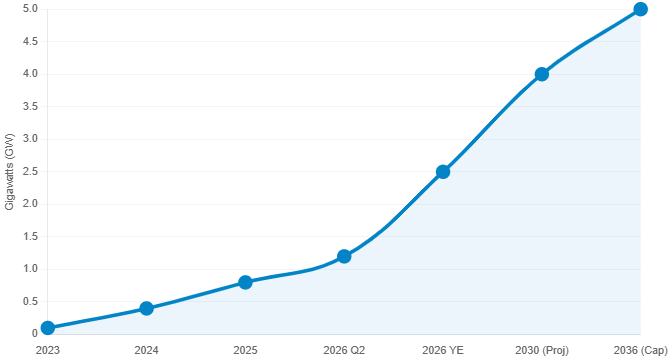

The 5 Gigawatt Figure Is A Contractual Ceiling, Not Deployed Capacity

The 5 gigawatt commitment covers Trainium2, Trainium3, Trainium4, and future silicon not yet designed.

Trainium4 does not yet exist commercially.

TSMC has not yet fabricated all required chips.

Power facilities, cooling systems, networking infrastructure, and physical data center buildings are forward deliverables.

Near-term capacity is concrete. Meaningful Trainium2 by Q2 2026. Nearly 1 gigawatt combined Trainium2 and Trainium3 by end of 2026.

The full 5 gigawatts is a ten-year contractual envelope, not an operational asset.

The structural read is that the deal has effectively pre-sold the next decade of AWS AI infrastructure capacity at the largest single-customer scale ever recorded. Over the next twelve to twenty-four months, AWS capacity available to other enterprise AI workloads will be priced against a contractual scarcity that did not exist before April 2026.

Anchor Book Depth Replaces Model Performance As The Hyperscaler Frontier

Microsoft and Nvidia committed $15 billion to Anthropic in late 2025 against a $30 billion Azure compute purchase commitment.

Amazon committed up to $33 billion against a $100 billion AWS commitment.

The Amazon arrangement runs deeper than the Microsoft arrangement by an order of magnitude in tenor and dollars.

Google has held a multi-billion-dollar Anthropic investment since founding without structuring a comparable anchor.

The structural read is that hyperscaler competition has shifted. Model performance was the leaderboard, and the leaderboard moves quarterly.

Anchor tenant book depth is the new frontier, and contractual commitments lock in capex utilization for a decade.

Over the next twelve to twenty-four months, public equity valuations of named hyperscalers should re-rate based on contracted AI revenue visibility rather than announced capex headlines.

This shift toward contractual demand as the primary competitive lever aligns with the structural transition analyzed in The Neocloud Is Not Overflow. It Is the Third Pillar of AI Infrastructure.

Investor Action

Data Center Operators. Independent operators face a qualification problem this deal makes explicit.

Hyperscalers are now building at a scale and tenor single-asset developers cannot match.

The 5 gigawatt multi-site commitment presumes contractual demand spanning a decade.

Operators competing on spec-built capacity without anchor tenant coverage will not be evaluated on AWS underwriting terms.

The action is to sequence anchor tenant procurement before site activation.

Secure a frontier lab, a hyperscaler, or a sovereign as a contractual counterparty before breaking ground.

The cost of inaction is direct.

Spec-built capacity without anchor coverage trades at a discount to hyperscaler-anchored comparables.

Power, land and capital are now solved.

Counterparty access is the remaining binding constraint.

PE and Infrastructure Funds. Anchor tenant models compress the return profile.

Lower risk. Lower yield. Longer duration.

The Anthropic-AWS structure functions economically like a triple-net lease with a ten-year initial term and chip-generation escalators.

For infrastructure funds with mandates calibrated to GDP-plus returns, this is a structurally attractive asset.

For private equity funds targeting mid-teens net IRRs on value-add strategies, this is the wrong asset.

The action is to evaluate mandate fit against the asset class the deal defines.

Funds positioned for core infrastructure exposure should calibrate underwriting models to anchor-tenant-backed AI infrastructure.

Funds positioned for value-add should not bid on this asset class without restructuring their mandate. The cost of inaction is competitive irrelevance.

The capital that wins AI infrastructure allocation over the next cycle will look more like core infrastructure than opportunistic real estate.

Public Markets Equity Investors. Amazon is running approximately $200 billion in 2026 capital expenditure, almost entirely directed at AI infrastructure.

The Anthropic commitment de-risks that capex at a scale Microsoft and Google cannot easily replicate without comparable anchor arrangements.

The action is to re-evaluate hyperscaler equity positioning based on anchor book depth, not announced capex headlines.

An investor benchmarking Amazon, Microsoft, and Google on capex announcements will misread the relative competitive position now that contracted demand has become the binding scarcity.

The Verdict

Amazon wrote a $33 billion check to secure a contractual counterparty for $200 billion of annual capital expenditure.

Equity ownership is a secondary feature of the structure.

The primary feature is the $100 billion AWS spend commitment that turns Anthropic into the largest single anchor tenant in the history of AI infrastructure.

That is a different asset class than the market has been pricing.

The market inflection is the redefinition of what frontier AI labs are.

They are no longer compute customers.

They are infrastructure co-investors writing ten-year demand commitments at the scale of sovereign capital flows.

The forward question is which hyperscaler signs the next $100 billion anchor, in which geography, and against which silicon generation.

The investors who recognize the asset class shift first will structure differently.

Those investors will win the next cycle.

frontier labs need to be good for the money too, though