The Hidden Constraint in Emerging Market AI Infrastructure

Capacity is surging, but without inland fiber, projects stall, costs spike, and AI infrastructure fails to scale.

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Event: Capacity Is Landing, But Not Scaling

Over the past five years, global capital has surged into subsea cables, hyperscale campuses, and AI-driven infrastructure. New systems have expanded international bandwidth across Africa, Southeast Asia, and Latin America, creating the perception that connectivity constraints are easing.

Yet capacity expansion is not keeping pace with expectations. The constraint is no longer access to international bandwidth. It is the inability to distribute that capacity inland at scale.

In Sub-Saharan Africa, terrestrial fiber has only recently surpassed one million kilometers, while mobile infrastructure has absorbed roughly 60% of investment compared to about 20% for fiber.

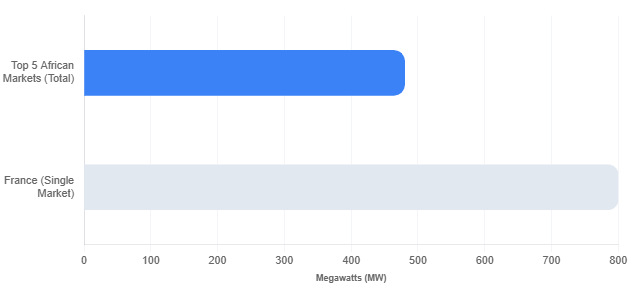

The imbalance is clear: the five largest African data center markets together account for less than 500 MW, versus approximately 800 MW in France alone. This is not a demand problem. It is a distribution problem.

Cause: Structural Gaps in Fiber Economics and Deployment

The fiber bottleneck is not driven by a single issue. It is the result of overlapping structural constraints.

Cost is the first barrier. Fiber deployment in emerging markets is heavily weighted toward civil works, often exceeding 50% of total project cost. In complex geographies, this cost escalates sharply. In Indonesia, terrestrial fiber deployment can exceed $600,000 per kilometer, making backbone expansion capital intensive before demand risk is even considered.

Regulation is the second constraint. Fiber deployment requires coordination across multiple layers of government, including transport, utilities, and municipal authorities. Fragmented right-of-way policies and permitting delays extend timelines and increase uncertainty.

Market structure is the third issue. In many markets, fiber infrastructure is controlled by incumbent telecom operators with limited incentives to provide open access. This restricts the availability of dark fiber and reduces competition, forcing data center operators into higher-cost connectivity arrangements with limited route diversity.

Physical vulnerability adds another layer of complexity. Fiber networks in several emerging markets are exposed to vandalism, accidental damage, and weak maintenance regimes. Reliability becomes difficult to guarantee, particularly for hyperscale workloads that require strict uptime standards.

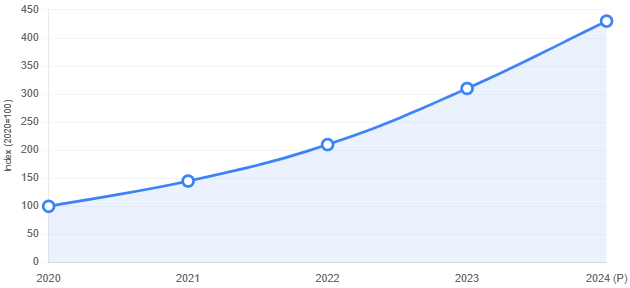

The final and most recent driver is AI. AI infrastructure is fundamentally more network-intensive than legacy enterprise workloads. Training clusters now require transmission speeds of 800 Gbps to 1.6 Tbps and depend on 24 to 48 fiber pairs for redundancy. Global bandwidth demand tied to data centers increased by approximately 330% between 2020 and 2024. This demand surge is colliding with already constrained terrestrial networks.

These operational fragilities are not isolated to emerging markets but reflect a broader structural risk embedded in fiber infrastructure, as examined in The Hidden Risk Inside U.S. Fiber Networks.

Impact: Fiber Constraints Are Destroying Economics

The financial consequences of limited fiber are direct and material.

Bandwidth costs are significantly higher in emerging markets. Transit pricing in Africa is approximately 14 times higher than benchmarks in Europe and North America, while South America reaches roughly 17 times. In Latin America, operators spend around $2 billion annually on international bandwidth, reflecting both cost inefficiencies and limited traffic localization.

Timelines are also affected. Fiber supply constraints and deployment delays have extended project schedules. During the 2022–2023 period, fiber lead times reached approximately 60 weeks, and fiber prices increased by up to 70% between 2021 and 2024. In less developed markets, interconnection delays can push revenue realization out by three to five years.

Returns deteriorate quickly under these conditions. A one-year delay in leasing can reduce MOIC by 0.2x to 0.4x over a ten-year hold period. This is particularly significant in emerging markets, where projects are typically underwritten to higher return thresholds of approximately 17% to 20% IRR, compared to 12% to 16% in developed markets.

Tenant dynamics reinforce the problem. Hyperscale and AI-driven tenants require dense, redundant, low-latency connectivity. Markets that cannot meet these requirements struggle to attract anchor tenants, leading to underutilized facilities.

Valuation follows. Data centers command premium EBITDA multiples, often in the range of 20x to 25x, compared to approximately 7x to15x for fiber infrastructure. However, these premiums depend on scalable connectivity. Where fiber is constrained, exit certainty declines and valuation compresses.

Investor Response: Fiber-First Underwriting and Platform Control

Leading investors have adjusted their strategies to reflect the centrality of fiber.

Site selection has shifted. Proximity to cable landing stations, internet exchange points, and dense metro fiber corridors is now a primary criterion. Investors are prioritizing locations where connectivity is already concentrated or can be expanded with lower marginal cost.

Control over fiber has become a strategic priority. Investors are securing indefeasible rights of use, leasing or building dark fiber, and forming partnerships with local network operators. Multi-carrier access and route diversity are treated as non-negotiable requirements rather than optional enhancements.

Vertical integration is gaining traction. Investors are combining fiber, power, and data center assets into unified platforms to control both cost and reliability. This reduces dependency on third-party infrastructure and improves operational predictability.

Blended finance is being deployed in more challenging markets. Development finance institutions have committed more than $9.6 billion to digital infrastructure over the past decade.

Government policy is beginning to align with these efforts. India’s BharatNet targets connectivity across 250,000 rural administrative units. Nigeria’s Project Bridge aims to deploy 90,000 kilometers of fiber. The Philippines has secured approximately $287 million to strengthen its national backbone. These initiatives signal a shift toward recognizing fiber as critical infrastructure rather than a secondary telecom layer.

This convergence toward integrated infrastructure platforms aligns with the strategic direction explored in Does Digital Edge’s $4.5B Indonesia Campus Change the Global Hyperscale Map?.

Investor Lesson: Fiber Determines Market Winners

The emerging-market data center narrative is being reframed. Power remains critical, but it is no longer the sole constraint. Fiber has become the gating variable that determines whether a project can scale, attract tenants, and achieve target returns.

The implication is straightforward. Investors must treat fiber as a primary underwriting factor, not a downstream consideration. This requires detailed mapping of fiber routes, assessment of redundancy, evaluation of carrier neutrality, and analysis of long-term bandwidth costs.

Markets that solve inland connectivity will capture disproportionate share of AI infrastructure investment. Markets that do not will remain capacity-constrained regardless of demand or power availability.

Fiber is not a supporting layer. It is the infrastructure that determines whether the rest of the stack works.