The Grid Is the Gatekeeper: Why Most Data Center Pipelines Never Energize

Interconnection queue attrition, behind-the-meter generation, capacity-price inflation, the powered-versus-paper asset split, emerging-market power arbitrage.

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

The constraint moved

Power access now decides which data center projects reach commercial operation and which become stranded capital.

The underwriting model that treated electricity as a utility input no longer holds.

That model assumed power was abundant, available on the developer’s schedule, and priced within a predictable band.

Sponsors who still underwrite a grid connection as a near-certain future event are funding pipelines that will never energize.

Why now

The shift is structural, not cyclical. AI-grade demand has overwhelmed the grid at every layer at once: generation, transmission, and distribution.

Hyperscale campuses that once drew tens of megawatts now request hundreds, and some single connection requests exceed a thousand.

Grid planners across the United States have nearly doubled their five-year load forecasts inside a single planning cycle.

The capital has not slowed. It has changed direction. It no longer moves toward whoever can pour a shell fastest.

It moves toward whoever can prove firm power on a date a counterparty will sign.

The capital has not slowed. It has changed direction. It moves now toward whoever can prove firm power on a date a counterparty will sign the force reshaping the global AI data center map.

How the bottleneck works

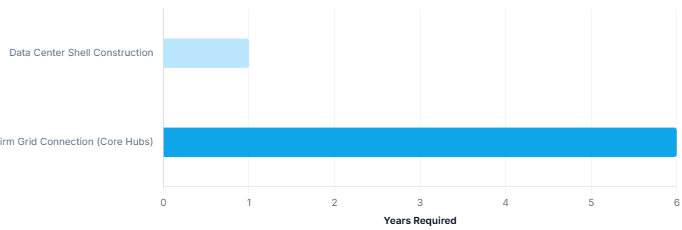

A data center shell can be built in roughly a year. A firm grid connection in a premium market now takes five to seven. That gap is the entire problem.

The interconnection queue is where the gap becomes visible. More generation and storage capacity now sits in United States interconnection queues than the entire installed base of the country’s power fleet. Most of it will never be built.

Withdrawal rates run high enough that queue position, on its own, carries almost no information about whether a project will reach commercial operation.

Every withdrawal forces operators to restudy the projects behind it. The queue does not clear. It compounds.

A developer secures land, signs a creditworthy anchor tenant, and enters the queue with a fully fundable project.

Three years on, the project holds the same queue position with no energization date. Capital remains committed. Financing continues to accrue. The tenant waits.

The asset produces nothing. This is not an edge case. In the most concentrated markets, it is the median outcome.

The asset produces nothing. This is not an edge case. In the most concentrated markets, it is the median outcome and the dynamic already repricing Europe's data center market.

The market is wrong

The industry has long assumed that power constraints resolve themselves.

That assumption held when load growth was incremental and utilities could plan against a predictable curve.

It does not hold now. Demand is arriving in hundred-megawatt increments faster than transmission can be planned, permitted, and built.

A grid connection is no longer a delivery date that slips by a few quarters. In the most constrained corridors, it is an outcome that may never arrive at all.

The supply chain sets the clock

Power is a timing problem before it is a cost problem.

The long-lead equipment that firm capacity depends on is backed up for years.

Large transformers carry multi-year lead times. Heavy turbines run longer still.

An order placed today delivers no usable capacity before the end of the decade. New transmission lines take close to a decade to permit and build, and the planning system was never designed for load arriving at this speed and scale.

Most of the major United States grid operators have already asked regulators for more time to meet transmission directives they cannot currently hit. None of this resolves on an investment committee’s timeline.

Three lenses, one constraint

For the independent operator, the binding variable is site qualification. A site is no longer qualified because it holds land, fiber, and a tax abatement. It is qualified only when power is contracted, with an energization date a counterparty will stand behind.

Operators that still rank sites on the old filters are qualifying sites that cannot be built.

For private equity and infrastructure investors, the binding variable is schedule risk, and schedule risk now drives the entire return. Every month a hyperscale-scale campus sits unenergized costs tens of millions in lost contracted revenue against fixed financing.

A delay measured in quarters does not trim the IRR at the margin. It moves the project from its underwritten return to a marginal one. Time-to-power has become the decisive underwriting input, ahead of location, lease term, and tenant credit.

For public equity investors, the binding variable is the widening gap between operators who control power and operators who do not. The market has begun to price it directly. Operators with secured generation and contracted offtake trade at a structural premium.

Operators holding large pipelines dependent on future interconnection carry a discount that deepens as the queue lengthens. The dispersion is no longer a story about real estate quality. It is a story about power.

Underwriting power now

The discipline is straightforward. The execution is not.

Reorder the site selection filters. Power availability and a contracted energization date come first. Land, fiber, and incentives are secondary screens that matter only once power clears.

Underwrite the queue with real withdrawal data. Developer optimism is not data.

Treat a queue slot as a lottery ticket until a signed interconnection agreement or firm contracted supply exists behind it.

Model schedule risk explicitly. Run the return against a multi-year delay, then confirm the project still clears its hurdle rate. If it only works on the optimistic timeline, it does not work.

Separate the powered from the paper. An operating asset with secured power and a contracted tenant is a different instrument from a pipeline project waiting on the grid. Underwrite them as different asset classes, because the market already does.

Secure power ahead of the market. Behind the meter generation, co-location with power assets, and long term offtake now define how disciplined capital buys development timelines the queue cannot offer.

Roughly a third of planned U.S. capacity now pursues on-site generation, while similar strategies open emerging markets with stranded power and clearer interconnection paths where energization dates remain achievable.

Treat power as the first underwriting decision, and you are no longer managing a risk.

You are buying the scarcest asset in the market before it is fully priced.

Do you think this constraint is evenly distributed among all RTOs or are some worse than others?

Power is everything and data centers need a lot of it. Yes, get power figured out first. Work with local power companies and city leaders. Win them over. Don’t be an adversary.