The Five Constraints That Decide Every Data Center Site

Power feasibility, fiber redundancy, permitting hierarchy, water rights, land economics, plus the diligence sequence that actually clears capital

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

This article is the 2nd article in the series: Ground to Grid: A Free 21-Lesson Guide to Mastering Data Center Development

Site selection is not a weighted scoring exercise.

It is a sequential filter.

Most diligence shops still run it as parallel scoring.

Power gets 30% to 40% of the weight.

Fiber gets 20%.

Regulation, water, and land split what is left.

Sites pass the model but they can not attract financing.

That framework worked before 2020. It does not work now.

The five constraints have not changed.

Power. Fiber. Regulation. Water. Land.

The order they filter in has flipped.

Why The Hierarchy Reordered

Before 2020, data center site selection was a real estate problem.

Operators picked submarkets on connectivity.

Then on tax structure.

Power was a check on minimum capacity.

It was not the binding input. Substations had reserve margin.

Queues moved in months.

Then AI training arrived.

Hyperscale facilities began clearing 100 megawatts.

Single AI campuses now contract for 200 to 600 megawatts. The grid sized for the prior decade did not get built for this one.

The numbers tell the rest.

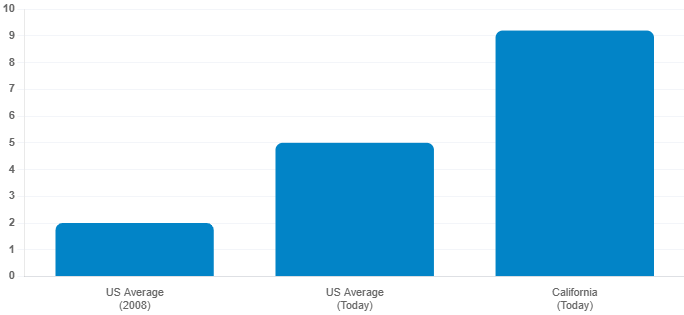

Average US interconnection wait was under two years in 2008.

It is nearly five today. California is past nine.

Around 2,300 gigawatts of generation sit in US queues right now.

That is more than the country’s entire installed base.

The grid did not catch up. The framework had to move.

Tier 1: Power

Power decides whether the project gets built in its window. That is why it sits at the top.

The disqualifying threshold is when interconnection timeline exceeds the project schedule with no behind-the-meter pathway. If the queue is six years and your fund needs commercial operations in three, the site is dead. The rest of the score does not matter.

You diligence Power by asking three questions. What is the available substation capacity at this voltage class? What is the realistic interconnection date? What is the bridge if the date slips?

The rate per megawatt-hour is downstream of all three.

Diligence Power on three questions: substation capacity at this voltage class, realistic interconnection date, bridge if the date slips. The rate per megawatt-hour is downstream of all three, and so is how power is now redrawing the AI infrastructure map.

Tier 2: Fiber

Fiber decides what the site can serve. That is why it sits second.

The disqualifying threshold is a single carrier route or no path to a Tier-1 internet exchange point inside the workload’s latency budget. Hyperscale tolerates moderate latency. Edge and colo do not. The site that works for an AI training cluster does not work for a financial trading colo. Pick the workload first.

You diligence Fiber on carrier diversity, route redundancy, and IXP proximity. In emerging markets, undersea cable landings (2Africa, Equiano, Bifrost) reset the calculation entirely for cities that previously ran on terrestrial backhaul.

Diligence Fiber on carrier diversity, route redundancy, IXP proximity. In emerging markets, undersea cable landings (2Africa, Equiano, Bifrost) reset the calculation and underscore why Fiber is the new bottleneck for AI returns.

Tier 3: Regulation

Regulation moved up to Tier 3 in 2025. That is the change most underwriting models have not absorbed.

Loudoun County, the densest data center submarket on earth, repealed by-right zoning in March 2025. Every project there now needs a public hearing. Kansas City followed. Fairfax County followed. Across Virginia, $900 million in projects has been blocked outright. Another $45.8 billion has been delayed by community resistance.

That is not noise. Permitting risk now sits at the front of the diligence stack.

The disqualifying threshold is by-right zoning revoked, an active moratorium, or a permitting timeline beyond 24 months. You diligence Regulation on zoning status, the full slate of authorities having jurisdiction, and the local political calendar.

Tier 4: Water

Water sits at Tier 4 because the cooling architecture decision is binding at design phase. After design, you cannot fix it cheaply.

A medium facility consumes up to 110 million gallons per year. Larger ones, up to 5 million per day. Industry average Water Usage Effectiveness is 1.8 liters per kilowatt-hour. Amazon best-in-class is 0.19. The architecture that delivers 0.19 is not the architecture that delivers 1.8.

The disqualifying threshold is freshwater stress beyond the cooling stack’s tolerance with no reclaimed water pathway. You diligence Water on rights, regulatory disclosure trajectory, and whether the cooling architecture is air, evaporative, direct-to-chip, or hybrid.

Tier 5: Land

Land sits at Tier 5 because almost every land problem is solvable with capital.

Cost has inflated. US data center land averaged $244,000 per acre in 2024. Loudoun trades above $4 million. Secondary markets are running 20 to 40 percent annual increases. Average campus transactions reached 244 acres in 2024, up 144 percent since 2022.

Land shapes the deal. It rarely kills it.

The disqualifying threshold is hard hazard exposure. 100-year flood plain. Seismic class above the facility tolerance. Insufficient acreage for phased buildout. The rest is a price problem.

What The Market Is Getting Wrong

The narrative still scores the five constraints in weighted parity. Power is just the heaviest input. The rest sit beneath it on a slider.

That misses the binding mechanic. The hierarchy is not weighted. It is sequenced. A site that fails Power cannot be rescued by Fiber, Regulation, Water, or Land. Strong scores below Power compensate for nothing.

The market believes the framework is still parallel. It is not.

Three Investor Lenses

For independent operators, the qualification problem hits at parcel level. Two 50-megawatt sites are not the same asset. One has a five-year interconnection queue. The other has an existing feeder.

The first is a permitting bet. The second is a power asset wrapped in a building. Most operators still underwrite both at comparable multiples. They are not comparable. They will clear at different prices over the next 36 months.

For PE and infrastructure investors, the framework reorders the diligence calendar. The IRR models that sized data center deals from 2018 to 2022 assumed two years from groundbreak to commercial operations. The current floor is three to four years on a clean site.

If you have not repriced your underwriting timeline, you are deploying into deals that hit target returns only on paper.

The fix is mechanical. You run Power feasibility before LOI. Not after. Not at closing. Before.

For public equity, the framework explains why brownfield site control is now the new REIT acquisition currency. Decommissioned coal plants. Retired industrial sites with intact substations.

These are not real estate transactions. They are power asset transactions wrapped in real estate. Equinix, Digital Realty, and the rest of the public REIT cohort are no longer competing primarily against each other. They are competing against hyperscaler self-build for the same brownfield substations.

Expect 2026 and 2027 REIT M&A to be priced on power assets first. Building portfolios second.

What Comes Next

The framework decides which capital clears at scale through 2030.

Operators who run it in parallel will keep underwriting sites that pass the model and fail the financing. Operators who run it sequentially will keep buying assets the market is still pricing as commodities.

In emerging markets, the inversion sharpens. Africa now treats captive generation as the baseline. The grid is the backup. Up to 33 outages per month in some markets means the utility is no longer the primary procurement channel.

Southeast Asia is splitting in two. Singapore at $178 per megawatt-hour for grid reliability. Indonesia at $60 with intermittent supply. Malaysia holds 60 percent of the regional pipeline at 3.4 gigawatts.

The framework still applies. Power filters first. Everything else is downstream.

If you are running the old playbook in 2026, you are buying 2018-priced sites at 2030 cost. Reorder the diligence sequence now. Or pay the spread later.

Part 3 examines the six stakeholders who make or break a development: How Hyperscale Data Centers Move From Site Discovery to FID