OpenAI’s $600B Compute Reset; Amazon’s $12B Gulf Coast Build; Hyundai’s $7.5B AI Campus Push

Inside the capital, power, and sovereignty shifts accelerating global AI infrastructure.

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

If you’re not a subscriber, here’s what you’ve missed so far:

Where the Next Gigawatt of AI Capacity Will Actually Be Built [Inside the New Global Hierarchy Shaped by Power Availability, Policy Alignment, and Platform Capital.]

How to Invest in Data Centers (And the Risks That Actually Matter) [An intelligence synthesis of the reports shaping AI-driven infrastructure, capital allocation, and market direction.]

9 Reports Shaping Global Data Center Strategy — Q4 2025 Intelligence Briefing [An intelligence synthesis of the reports shaping AI-driven infrastructure, capital allocation, and market direction.]

Q4 2025: The Quarter AI Infrastructure Became State Power [How power, capital, and policy fused to redefine the global AI buildout.]

Interested in sponsorship? info@globaldatacenterhub.com

In This Issue

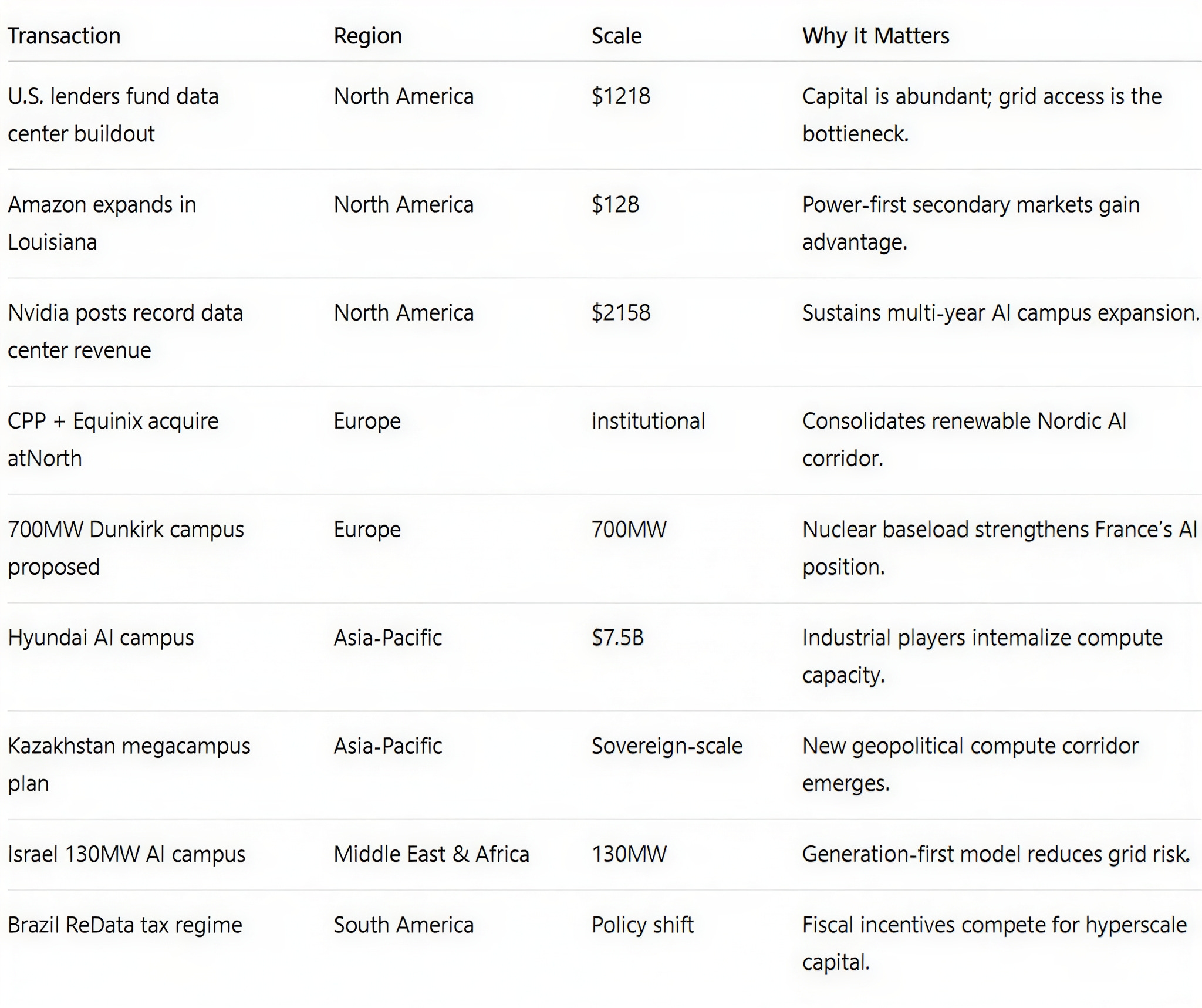

Global Buildout at a Glance — OpenAI’s $600B compute target, $121B in U.S. data center debt, Hyundai’s $7.5B campus in Korea, and France’s 700MW Dunkirk proposal signal that AI-scale capacity is moving beyond ambition into execution.

Power + Capital = Control — U.S. lenders deployed $121B in construction financing, Amazon expanded into Louisiana’s power-abundant corridor, and Israel advanced a 130MW utility-led campus. The constraint is no longer capital. It is grid certainty.

Sovereign and Industrial AI — Kazakhstan’s megacampus plan, Hyundai’s vertically integrated push, and Brazil’s ReData tax regime show governments and industrial leaders positioning as long-term compute landlords.

Notable Transactions — CPP and Equinix expanded in Nordic renewable corridors, Yondr advanced European ABS financing, and Nvidia posted a record $215B revenue year, signaling a deeper, more diversified AI infrastructure capital stack.

Dear Friends,

A new phase of AI infrastructure is taking shape defined not by isolated data center builds, but by programmatic capital deployment, power security, and multi-continent scale.

This week crystallized the shift: OpenAI’s ~$600B compute reset reframed long-term demand, $121B in U.S. construction debt confirmed record institutional backing, and Amazon’s $12B Louisiana expansion tied hyperscale growth to power-rich corridors, while Nvidia’s $215B revenue underscored sustained silicon demand. Globally, scale is aligning with energy from France’s 700MW nuclear-backed proposal and Hyundai’s $7.5B vertically integrated campus to emerging-market pushes in Kazakhstan, Brazil, and Israel, where policy, power, and compute are converging.

The message is clear: success in the next decade won’t go to the smartest model, but to those who command megawatts, land, and long-dated capital in unison.

Global Buildout at a Glance

A 1-minute scan of the week’s biggest moves — by region.

North America — OpenAI’s ~$600B compute reset and $121B in U.S. construction lending confirm AI infrastructure has entered the institutional capital era, where financing is abundant but grid access is the constraint. Amazon’s $12B Louisiana expansion strengthens the Gulf Coast as a power-first corridor, while Nvidia’s $215B annual revenue including $62.3B in quarterly data center sales underscores sustained silicon demand driving multi-year campus growth.

Europe — CPP Investments and Equinix’s acquisition of atNorth consolidates renewable-heavy Nordic corridors under sovereign-backed ownership, reinforcing hydro- and wind-powered regions as Europe’s AI release valve. France’s proposed 700MW Dunkirk campus leverages nuclear baseload and port access to anchor continental AI capacity, while Yondr’s London ABS financing reflects Europe’s shift toward securitized structures that recycle capital and accelerate expansion.

Asia-Pacific — Hyundai’s planned $7.5B AI campus in South Korea reflects industrial conglomerates internalizing compute capacity, aligning manufacturing, energy, and AI workloads under one strategy. Kazakhstan’s ambition to build Central Asia’s largest data center campus introduces a new geopolitical compute corridor between Europe and Asia, while India’s $2B Nvidia-backed AI hub underscores silicon access as the decisive factor for domestic AI scale.

Middle East & Africa — Israel’s 130MW Dalia Energy campus shows a generation-first model, while Saudi Arabia’s capital recycling signals consolidation around sovereign-backed platforms. Across the region, energy and state capital are increasingly shaping AI capacity, positioning compute as strategic infrastructure rather than conventional real estate.

South America — Brazil’s ReData tax framework reframes fiscal policy as a competitive lever for hyperscale attraction, pairing renewable-heavy generation with targeted tax incentives to draw AI capital. Meanwhile, Uruguay’s Antel data center partnership with Google highlights how national telecom operators can function as sovereign gateways for global cloud expansion across Latin America.

Notable Transactions

Key shifts, structures, and risks across this week’s global deal tape.

This week confirmed that AI-scale growth is now credit-deep and power-constrained: infrastructure is being financed at institutional scale, but execution hinges on grid certainty and long-dated energy alignment.

$121B in U.S. data center construction lending underscores that capital is no longer the bottleneck. OpenAI’s ~$600B compute horizon resets demand expectations for the decade, while Amazon’s $12B Louisiana expansion reinforces investor preference for power-secured, secondary-market corridors over congested legacy hubs. Nvidia’s $215B revenue year anchors underwriting confidence across the stack, from GPU supply to multi-GW campus development.

Across Europe, CPP and Equinix’s atNorth acquisition consolidates renewable Nordic corridors as structural AI moats. France’s 700MW Dunkirk campus brings nuclear baseload into AI planning, while Yondr’s London ABS issuance highlights Europe’s shift to securitized capital for faster expansion.

In Asia-Pacific, Hyundai’s $7.5B AI campus signals industrial groups entering direct compute ownership, while Kazakhstan’s megacampus and India’s $2B Nvidia hub highlight sovereign ambition and silicon access. In the Middle East & Africa, Israel’s 130MW utility-led project reflects a generation-first model, as the region shifts from isolated builds to energy-aligned compute platforms.

Across South America, Brazil’s ReData tax regime links fiscal policy with renewable grids to drive infrastructure investment, while Uruguay’s Antel-Google partnership shows sovereign telecom assets as entry points for hyperscale capital.

If you’re enjoying this newsletter, share it with a colleague.

Have a great week.

Global Data Center Hub