OpenAI’s $122B AI Surge; Nordics’ 500MW+ Buildout; Southeast Asia’s Hyperscale Push

Inside the capital, power, and geopolitical shifts redefining global AI infrastructure

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

If you’re not a subscriber, here’s what you’ve missed so far:

Q1 2026: The Quarter AI Infrastructure Became Energy-Constrained [How power, capital, and compute converged to redefine the global AI buildout.]

Where Is Capital Flowing in the Global AI Data Center Buildout? [February’s 2026 global data center deals reveal how capital, power, and platforms are determining where the next wave of AI compute capacity will scale.]

19 key takeaways from Jensen Huang’s NVIDIA GTC 2026 keynote [Inside Jensen Huang’s GTC 2026 keynote: how AI factories, inference economics, and system design are reshaping data centers and shifting value to compute productivity.]

9 Reports Shaping Global Data Center Strategy — Q4 2025 Intelligence Briefing [An intelligence synthesis of the reports shaping AI-driven infrastructure, capital allocation, and market direction.]

Interested in sponsorship? info@globaldatacenterhub.com

In This Issue

Global Buildout at a Glance — OpenAI’s $122B capital raise, Texas’ 2GW campus wave, Finland’s 300MW+ AI factories, and Microsoft’s Southeast Asia expansion signal capacity scaling across every major region.

Power + Capital = Advantage — Texas reinforces the power-first model, Nordic markets absorb Europe’s overflow demand, and Southeast Asia captures hyperscale expansion through policy and grid access.

Geopolitics Meets Infrastructure — Strikes impacting Amazon-linked infrastructure in Bahrain highlight a new reality: data centers are entering the geopolitical risk perimeter.

Notable Transactions — CoreWeave’s $8.5B GPU-backed facility, Digital Realty’s $3.25B fund, and Nxtra’s $1B raise show capital formation shifting toward compute-driven and platform-level financing.

Dear Friends,

A new phase of AI infrastructure is emerging defined not by linear scaling, but by capital pulling capacity forward faster than grids can respond. This week made the shift explicit.

Model-driven demand is now setting the pace of capacity expansion. OpenAI’s $122B raise establishes a new ceiling for AI infrastructure demand, while CoreWeave’s $8.5B GPU-backed financing shows capital markets adapting to fund compute directly. Gigawatt-scale development in Texas and large deployments across the Nordics signal a shift toward power-first, regionally concentrated buildouts.

Energy strategy is evolving in parallel. Grid constraints in Europe are shifting demand to energy-abundant regions like Finland and Denmark, while Microsoft’s Southeast Asia expansion highlights how policy and power access guide deployment. Geopolitical risks such as attacks on Amazon-linked infrastructure in Bahrain add a new layer of complexity to infrastructure planning.

The takeaway is clear: the next decade will be won not by those with the largest facilities, but by those who align power, land, and capital to build AI infrastructure across regions over the long term.

Global Buildout at a Glance

A 1-minute scan of the week’s biggest moves — by region.

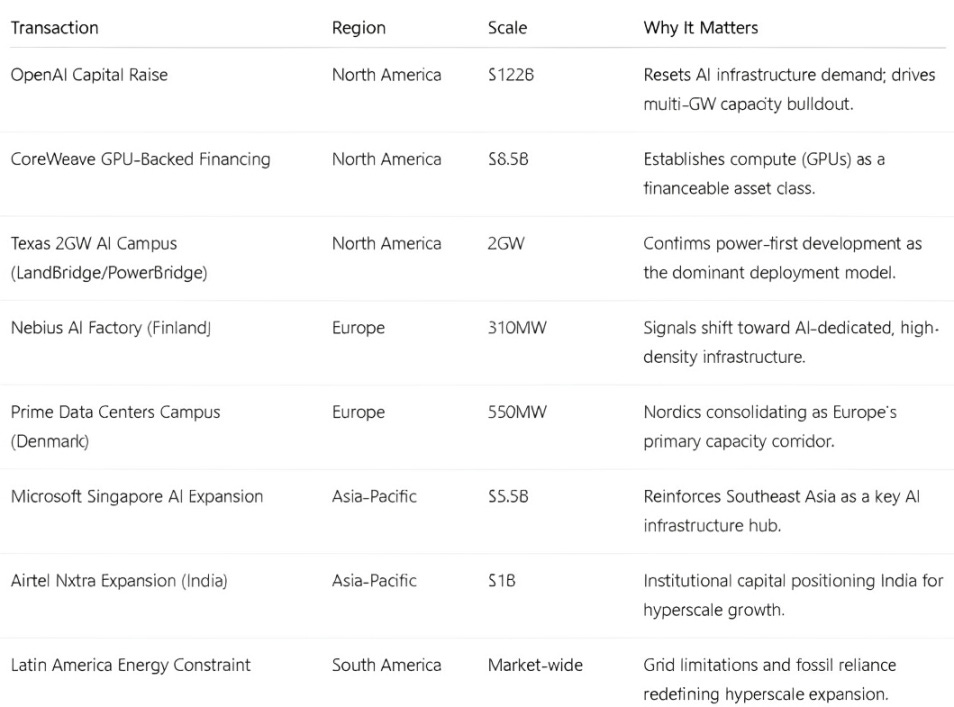

North America — The U.S. is reinforcing its role as the global AI infrastructure core, driven by capital and power-first execution. OpenAI’s $122B raise expands compute demand, while CoreWeave’s $8.5B GPU-backed facility signals a new financing model tied to compute assets. Texas remains the epicenter, with a 2GW campus and large-scale builds reinforcing the ERCOT model, alongside energy-integrated strategies from gas to nuclear-adjacent development.

Europe — Growth is accelerating but constrained by power, land, and policy friction. Projects like the 310MW Nebius AI factory in Finland and Prime’s 550MW campus in Denmark reinforce the Nordics as the primary capacity corridor, supported by renewable and cooling advantages. Germany’s 500MW pipeline highlights continued demand in core markets, but grid constraints and execution timelines are becoming the limiting factors shaping where projects can scale.

Asia-Pacific — Growth is accelerating through hyperscale expansion and institutional capital. Microsoft’s $5.5B investment in Singapore reinforces its role as a regional AI hub despite power constraints, supported by strong policy alignment. India continues to attract capital through Airtel Nxtra’s $1B raise, positioning for hyperscale and AI workloads, while Thailand’s 250MW True IDC project signals emerging capacity hubs driven by improving power access and regional demand.

Middle East & Africa — Infrastructure growth is increasingly shaped by geopolitical risk. Damage to Amazon-linked assets in Bahrain highlights rising physical and political exposure. Meanwhile, markets like Morocco are emerging as digital hubs, leveraging proximity to Europe and improving connectivity.

South America — Latin America’s data center market is being reshaped by a structural energy gap between renewable capacity and reliable power delivery. While demand is increasing, continued reliance on fossil fuels and constrained grid infrastructure are redefining where hyperscale projects can scale.

Notable Transactions

Key shifts, structures, and risks across this week’s global deal tape.

This week reinforced that AI-scale growth is increasingly platform-driven, with capital deployed through repeatable programs anchored by secured power, hardware access, and institutional credit depth.

If you’re enjoying this newsletter, share it with a colleague.

Have a great week.

Global Data Center Hub