OpenAI’s $10B Raise; NextEra’s 10GW Power Play; Adani–Hyperscaler Push in India

Inside the capital, power, and policy shifts reshaping global AI infrastructure.

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

If you’re not a subscriber, here’s what you’ve missed so far:

Where Will the Next Wave of AI Data Centers Be Built? [January’s global data center deals show how power, capital, and national strategy are shaping where the next wave of AI infrastructure will scale.]

How to Invest in Data Centers (And the Risks That Actually Matter) [An intelligence synthesis of the reports shaping AI-driven infrastructure, capital allocation, and market direction.]

9 Reports Shaping Global Data Center Strategy — Q4 2025 Intelligence Briefing [An intelligence synthesis of the reports shaping AI-driven infrastructure, capital allocation, and market direction.]

Q4 2025: The Quarter AI Infrastructure Became State Power [How power, capital, and policy fused to redefine the global AI buildout.]

Interested in sponsorship? info@globaldatacenterhub.com

In This Issue

Global Buildout at a Glance — OpenAI’s $10B capital raise and SoftBank–AEP’s power-integrated campus to Thailand’s $6B financing push and Spain’s 4.35GW pipeline, every region is scaling AI-ready capacity with different constraints and advantages.

Power + Capital = Control — NextEra’s 10GW approval and utility-aligned campuses confirm that generation ownership, not capital availability, now determines which projects get built.

Hyperscalers Anchor Markets — Adani’s talks with Meta and Google and Southeast Asia’s expansion wave show that demand-backed development is replacing speculative builds.

Notable Transactions — From multi-billion debt raises in Thailand to platform financing and asset recycling in Europe, the capital stack is consolidating around fewer, larger players.

Dear Friends,

A new phase of AI infrastructure is emerging defined not by isolated announcements, but by execution across power, land, and permitting. This week made the shift explicit.

Hyperscalers are locking in future capacity before it exists, with OpenAI’s ~$10B raise reinforcing a forward-built demand pipeline. At the same time, capital is scaling around fewer platforms, as developers move toward larger, integrated financing structures to support multi-GW expansion.

Energy is now upstream of development. NextEra’s 10GW generation approval and the SoftBank–AEP model in Ohio show that control of power is determining which projects move forward. In parallel, Adani’s engagement with Meta and Google highlights that demand certainty is becoming the prerequisite for unlocking new markets.

The takeaway is clear: the next wave of AI infrastructure will not be defined by who builds the most capacity, but by who aligns power, demand, and capital into a coordinated system across regions.

Global Buildout at a Glance

A 1-minute scan of the week’s biggest moves — by region.

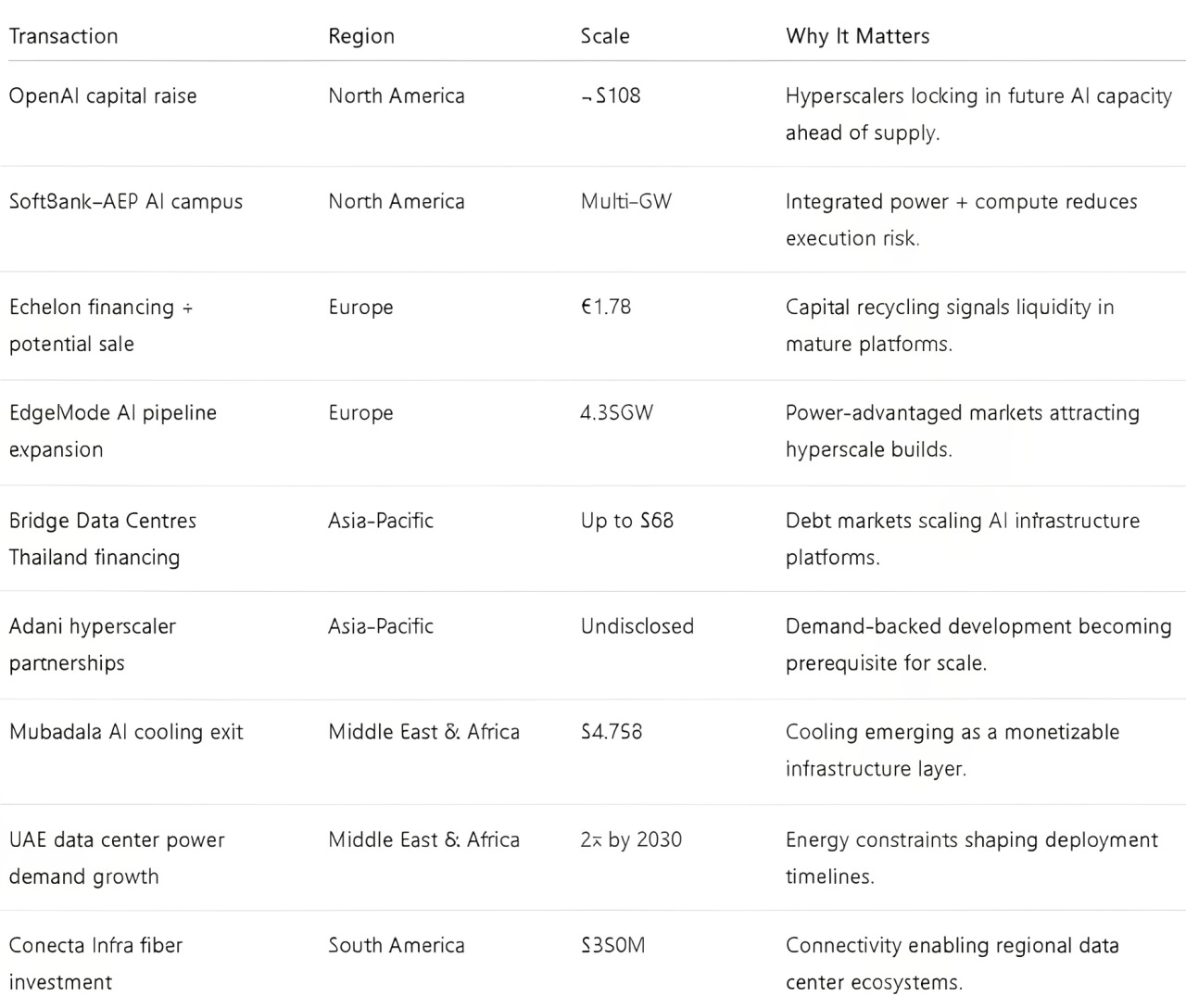

North America — OpenAI’s planned ~$10B raise signals hyperscalers are securing multi-gigawatt capacity pipelines before infrastructure is delivered. NextEra’s approval to develop up to 10GW of gas-fired generation confirms power is now the primary gating constraint. Meanwhile, the SoftBank–AEP partnership in Ohio highlights a model where utilities and capital providers align to deliver power-secured AI campuses, accelerating deployment and shifting advantage toward integrated developers.

Europe — Spain is emerging as a major AI infrastructure hub, with EdgeMode expanding its pipeline to 4.35GW, driven by relative power availability and land access. In the UK, the government’s move to bypass local councils for AI data center approvals signals a shift toward centralized, strategic permitting frameworks. At the same time, Echelon’s €1.7B financing alongside potential sale discussions highlights increasing liquidity and institutional capital rotation across European data center platforms.

Asia-Pacific — Asia’s expansion is increasingly anchored in demand-backed development. Adani’s discussions with Meta and Google reflect India’s transition toward hyperscaler-aligned infrastructure, while Bridge Data Centres’ pursuit of up to $6B in financing positions Thailand as a breakout AI market amid Singapore’s constraints. Princeton Digital Group’s 210MW expansion further reinforces the shift toward multi-campus, hyperscale-driven capacity across the region.

Middle East & Africa — The UAE data centre power demand to double by 2030 as regulatory gaps constrain clean energy procurement | Wood Mackenzie, highlighting energy procurement regulations as a key growth constraint. Meanwhile, Mubadala’s $4.75B exit from an AI cooling firm signals growing investor focus on specialized infrastructure, with thermal management becoming a critical component of AI data center economics.

South America — Conecta Infra’s $350M initiative to connect regional data center hubs underscores that fiber infrastructure is enabling distributed growth across the continent. As connectivity improves, South America is positioning for a more interconnected, multi-node data center ecosystem rather than reliance on single-market concentration.

Notable Transactions

Key shifts, structures, and risks across this week’s global deal tape.

This week confirmed a structural reality: AI infrastructure is consolidating around platforms that align capital, power, and demand, with execution increasingly dependent on securing energy and financing at scale rather than standalone asset development.

If you’re enjoying this newsletter, share it with a colleague.

Have a great week.

Global Data Center Hub