Microsoft’s $50B Global South Push; Adani’s $100B AI Energy Bet; Meta’s $10B Indiana Buildout

Inside the capital, power, and sovereignty shifts reshaping AI infrastructure in 2026.

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

If you’re not a subscriber, here’s what you’ve missed so far:

Where the Next Gigawatt of AI Capacity Will Actually Be Built [Inside the New Global Hierarchy Shaped by Power Availability, Policy Alignment, and Platform Capital.]

How to Invest in Data Centers (And the Risks That Actually Matter) [An intelligence synthesis of the reports shaping AI-driven infrastructure, capital allocation, and market direction.]

9 Reports Shaping Global Data Center Strategy — Q4 2025 Intelligence Briefing [An intelligence synthesis of the reports shaping AI-driven infrastructure, capital allocation, and market direction.]

Q4 2025: The Quarter AI Infrastructure Became State Power [How power, capital, and policy fused to redefine the global AI buildout.]

Interested in sponsorship? info@globaldatacenterhub.com

In This Issue

Global Buildout at a Glance — From Meta’s $10B Indiana campus and Fleet’s $3.8B Reno financing to Adani’s $100B AI platform and Nscale’s $1.4B GPU loan, the hyperscale and sovereign players accelerated across major corridors.

Power + Capital = Control — Utah’s 280MW behind-the-meter structure, Japan’s 121MW solar hedge, and India’s vertically integrated AI-energy strategy confirm that power alignment is now the gating factor for AI capacity.

Sovereign Scale Emerges — Microsoft’s $50B trajectory across the Global South and Adani’s 2035 AI blueprint show emerging markets moving from demand centers to compute landlords.

Notable Transactions — GPU-backed lending in Europe to multi-billion-dollar U.S. secured notes and India’s Blackwell-anchored AI hub, the capital stack continues shifting from stabilized real estate to AI-specific infrastructure underwriting.

Dear Friends,

A new phase of AI infrastructure is emerging defined not by isolated data center announcements, but by synchronized capital deployment, energy control, and sovereign alignment across continents.

This week made the shift clear. Adani’s $100B AI platform reframes India as a compute landlord. Meta’s $10B Indiana campus and Nvidia expansion show hyperscalers industrializing chip and construction cycles. Fleet’s $3.8B Reno notes and Nscale’s $1.4B GPU-backed facility confirm capital markets are underwriting AI density. Microsoft’s $50B Global South trajectory signals compute geography is moving toward sovereign-aligned corridors.

The signal is structural: power is secured before tenants, hardware is financed alongside land, and governments are treating AI infrastructure as strategic industrial capacity.

Global Buildout at a Glance

A 1-minute scan of the week’s biggest moves — by region.

North America — Meta’s $10B Indiana campus and expanded Nvidia integration, alongside Fleet’s $3.8B secured notes in Reno, reinforced a defining U.S. pattern: hyperscale AI growth is concentrating where capital markets and grid positioning already align. In Utah, a 280MW behind-the-meter structure for a proposed 10GW campus shows developers underwriting generation before tenants. Firm power and interconnect certainty not financing depth are emerging as the decisive constraints.

Europe — Nscale’s $1.4B GPU-backed delayed draw loan marked a structural financing shift, bringing hardware into the collateral base for AI clusters. At the same time, UK political scrutiny over data center energy demand highlights that compute growth is now directly entangled with climate policy. Germany’s €1B+ investment momentum confirms capital appetite remains strong but planning speed and grid access are becoming core competitive advantages.

Asia-Pacific — Adani’s $100B renewable-powered AI data center platform and Yotta’s $2B Blackwell-anchored hub underscore that India is moving from tenant market to vertically integrated AI corridor. In Japan, Equinix’s 121MW solar commitment reinforces that power hedging is prerequisite to capacity expansion. Across APAC, national-scale coordination between developers, utilities, and sovereign capital is replacing incremental, tenant-led growth.

Middle East & Africa — Khazna’s launch of a national data center skills program reinforces the Gulf’s view of compute as sovereign infrastructure. By building domestic engineering and operations capacity, the UAE is signaling that workforce depth alongside power and capital is now critical to sustaining AI-scale expansion.

South America — Microsoft’s activation of two new data halls in São Paulo reinforces Brazil’s role as Latin America’s hyperscale anchor. However, Mexico’s growing talent gap reveals a structural risk: while demand and capital are present, technical labor constraints may determine whether the region captures AI-grade capacity or remains primarily an enterprise cloud market.

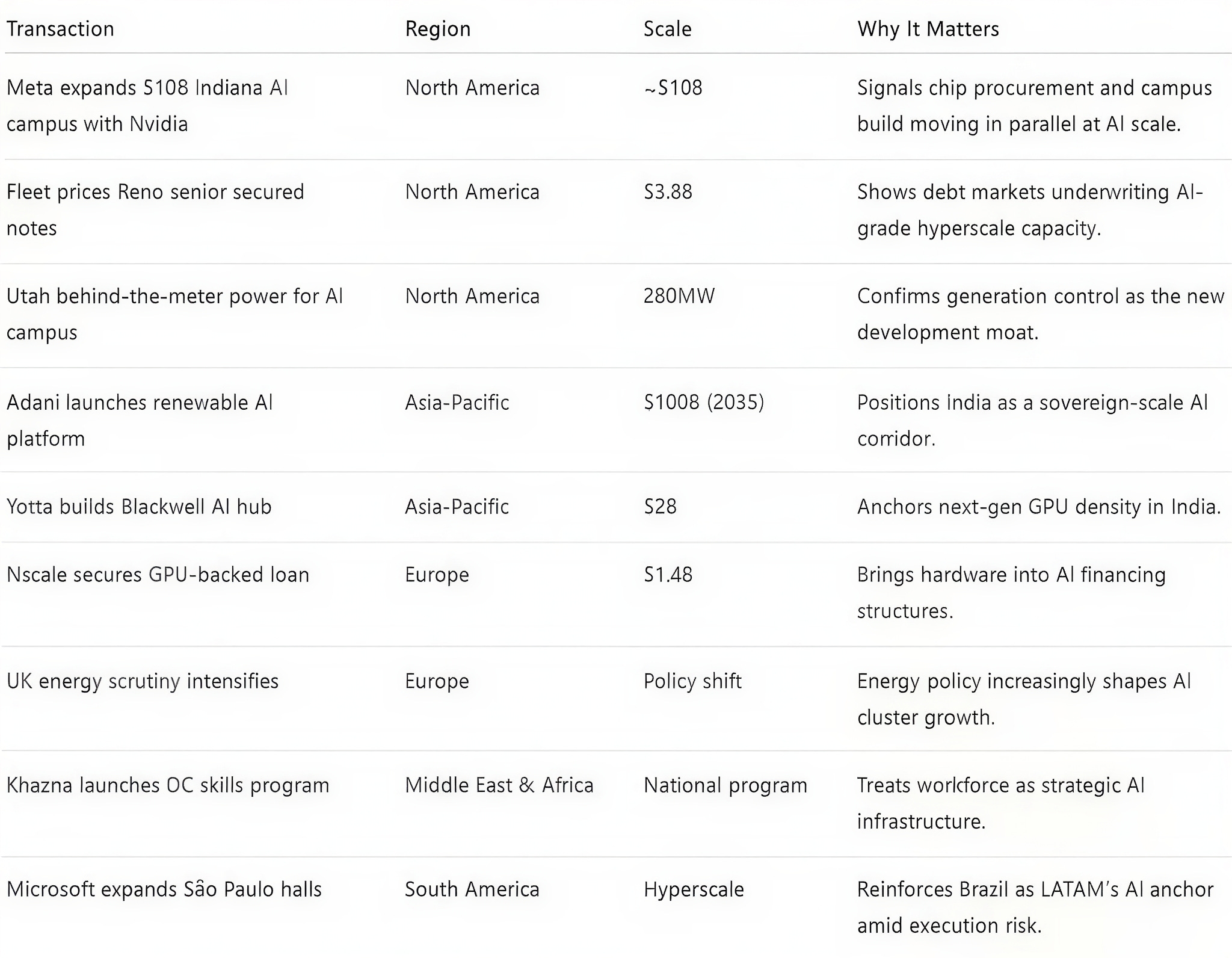

Notable Transactions

Key shifts, structures, and risks across this week’s global deal tape.

This week reinforced that AI-scale growth is increasingly platform-driven, with capital deployed through repeatable programs anchored by secured power, hardware access, and institutional credit depth.

Meta’s $10B Indiana campus and Nvidia expansion show chip procurement and campus construction moving in parallel. Fleet’s $3.8B Reno notes confirm debt markets are underwriting AI-grade facilities, while Utah’s 280MW behind-the-meter project highlights generation control as a primary development moat.

In Asia-Pacific, Adani’s $100B renewable-powered AI blueprint and Yotta’s $2B Blackwell-anchored hub signal national-scale coordination between capital providers, utilities, and silicon supply chains. These are long-horizon platforms designed to internalize energy risk and absorb hyperscale workloads over decades.

In Europe, Nscale’s $1.4B GPU-backed delayed draw loan brings hardware into the collateral base, expanding the capital stack beyond real estate. UK scrutiny over energy use underscores that policy now shapes where AI clusters can scale. In Middle East and Africa, Khazna’s workforce programs signal talent is treated as strategic infrastructure.

Across South America, Microsoft’s São Paulo expansion and Mexico’s emerging talent constraints reflect a pragmatic model: targeted hyperscale growth tempered by execution risk in grid and labor markets.

If you’re enjoying this newsletter, share it with a colleague.

Have a great week.

Global Data Center Hub