Meta’s Nuclear Pivot; BlackRock’s $30B AI Push; Thailand Approves $3.1B in Data Centers

Inside the capital, power, and policy shifts redefining global AI infrastructure

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

If you’re not a subscriber, here’s what you’ve missed so far:

Where the Next Gigawatt of AI Capacity Will Actually Be Built [Inside the New Global Hierarchy Shaped by Power Availability, Policy Alignment, and Platform Capital.]

How to Invest in Data Centers (And the Risks That Actually Matter) [An intelligence synthesis of the reports shaping AI-driven infrastructure, capital allocation, and market direction.]

9 Reports Shaping Global Data Center Strategy — Q4 2025 Intelligence Briefing [An intelligence synthesis of the reports shaping AI-driven infrastructure, capital allocation, and market direction.]

Q4 2025: The Quarter AI Infrastructure Became State Power [How power, capital, and policy fused to redefine the global AI buildout.]

Interested in sponsorship? info@globaldatacenterhub.com

In This Issue

Global Buildout at a Glance — Meta’s nuclear-backed compute strategy, BlackRock’s $30B AI infrastructure push, Thailand’s approval surge, and Australia’s 720MW powerbank show AI capacity is advancing fastest where both power and capital are secured.

Power + Policy = Advantage — Nuclear PPAs in the U.S., grid-cleared approvals across Southeast Asia, and pre-banked generation in Australia signal a clear shift: access to firm megawatts and permitting certainty now outweigh land availability in driving AI deployment.

Institutional Capital Takes Control — BlackRock’s accelerating AI fundraising and Vantage’s EMEA securitization mark the move from project-level financing to balance-sheet and platform-driven capital, favoring operators with regional scalability.

Notable Transactions — ERCOT approvals surpassing 800MW, Europe’s reopened data-center credit markets, and Brazil’s largest renewable power deal illustrate how AI infrastructure financing is becoming deeper, more structured, and increasingly tied to available power.

Dear Friends,

A new phase of AI infrastructure is emerging characterized less by standalone data center projects and more by coordinated capital deployment, secured power, and execution at global scale.

This week made that shift explicit. Meta’s move to anchor AI compute to nuclear generation reframed energy strategy as a competitive moat, while BlackRock’s advance toward a $30B AI infrastructure platform confirmed that institutional capital is consolidating around scale, not assets. At the same time, governments moved from signaling to execution: Thailand approved billions in new capacity, Australia locked in 720MW ahead of demand, and ERCOT continued absorbing AI load at gigawatt scale.

The implication is straightforward: The next decade of AI infrastructure will be decided not by the best models, but by who can coordinate megawatts, land, and long-term capital across regions.

Global Buildout at a Glance

A 1-minute scan of the week’s biggest moves — by region.

North America — Meta’s “Meta Compute,” anchored by nuclear agreements with Oklo, TerraPower, and Vistra, embeds cost stability and uptime directly into AI infrastructure, signaling a shift away from market-based power. Alongside this, BlackRock’s $12.5B raise toward a $30B AI platform confirms that capacity is now being financed at platform scale, while Galaxy Digital’s additional 830MW approval in ERCOT reinforces Texas’s power-first advantage even as future headroom tightens.

Europe — Blackstone’s potential $4.65B investment in German data centers signals renewed institutional appetite for markets with industrial-scale power, even as regulatory complexity persists. In parallel, Vantage’s £200M EMEA securitization tap shows European data center credit reopening selectively for stabilized portfolios, while Amazon’s acquisition of a former UK power-station site highlights how brownfield, power-adjacent land is emerging as the fastest path to AI-ready capacity.

Asia-Pacific — Thailand’s approval of $3.1B in new data center projects marked a transition from pipeline formation to grid-backed execution, positioning the country as a credible alternative to Singapore and Johor for hyperscale growth. In Australia, Keppel’s securing of a 720MW powerbank site near Melbourne underscored the region’s embrace of power-first AI campuses, with generation locked in ahead of construction.

Middle East & Africa — Batelco and Qareeb’s launch of an edge data center in Bahrain highlighted a regional focus on latency-sensitive and enterprise workloads, led by telecom operators rather than hyperscalers. Separately, Bahrain-based Arcapita’s acquisition of a U.S. data center asset reflected continued outward deployment of Gulf capital into mature AI infrastructure markets.

South America — Casa dos Ventos and Ascenty’s renewable deal shows power procurement is now the key driver of large-scale AI data center growth in Brazil, solidifying its status as Latin America’s most bankable market. Meanwhile, Hive Digital’s Buzz Cloud in Paraguay signals early-stage, enterprise-driven edge compute expanding alongside hyperscale development.

Notable Transactions

Key shifts, structures, and risks across this week’s global deal tape.

This week reinforced a central reality: AI-scale growth is now portfolio-driven, anchored by firm power, institutional balance sheets, and sovereign-aligned capital rather than standalone projects.

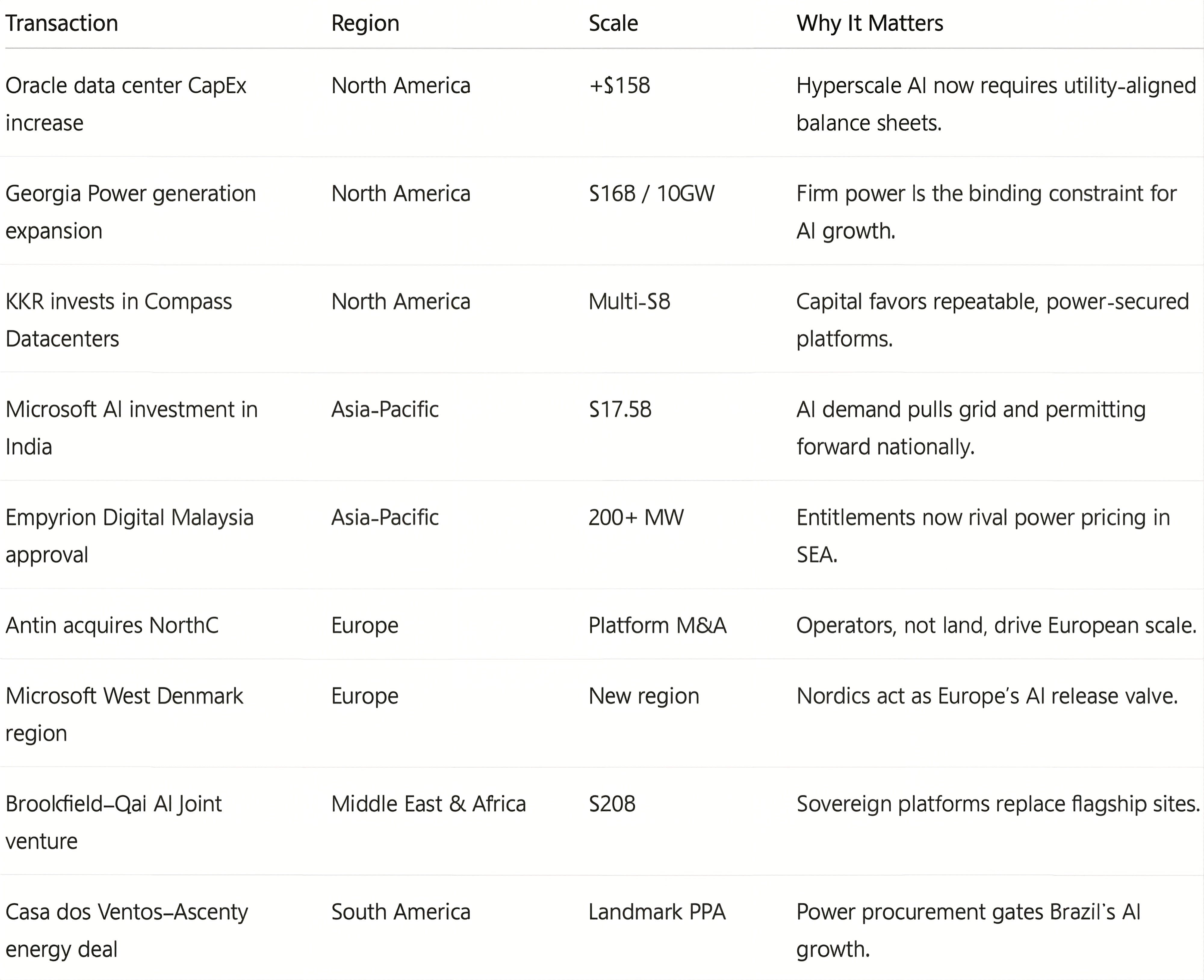

Meta’s nuclear-backed compute deals, Oracle’s additional $15B North America data center capex, and Georgia Power’s $16B, 10GW generation plan reinforced that firm power not land or capital is now the gating variable for hyperscale growth, while KKR’s investment in Compass Datacenters highlighted investor preference for repeatable, power-secured platforms.

Across Asia-Pacific, Microsoft’s $17.5B India commitment, Empyrion Digital’s 200+MW Malaysia clearance, Thailand’s $3.1B approvals, and Keppel’s 720MW Melbourne site showed AI demand accelerating grid, entitlement, and construction decisions at national scale.

In Europe, Antin’s NorthC deal and Microsoft’s West Denmark launch underscored the Nordics as power release valves, while Blackstone and Vantage signaled a cautious return of institutional credit. In the Middle East & Africa, Bahrain’s edge launch, Arcapita’s U.S. acquisition, and Brookfield–Qai’s $20B JV highlighted latency-driven builds and the rise of sovereign-backed global AI platforms.

Across South America, Casa dos Ventos–Ascenty’s landmark renewable deal confirmed power procurement as the gating factor for Brazil’s AI growth, while Hive Digital’s Buzz Cloud launch in Paraguay illustrated early-stage, enterprise-led edge deployments driven by local demand, latency, and regulatory clarity.

If you’re enjoying this newsletter, share it with a colleague.

Have a great week.

Global Data Center Hub