Meta Q1 2026: The $145B Reset and the Repricing of Free Cash Flow

How Component Inflation, $107B in Locked Commitments, and the Compute-vs-Payroll Tradeoff Are Reshaping Meta's Capital Structure

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Meta’s first quarter of 2026 delivered the strongest revenue growth in nearly five years, and the market responded by selling the stock down 8.6 percent. That gap is the analytical story.

Earnings beats are no longer pricing hyperscaler equities. Capital intensity, free cash flow trajectory, and the duration of the infrastructure cycle now are.

The structural signal is that 2026 hyperscaler capex has shifted from predictable capacity growth to a function of component pricing and long-term commitments.

Meta’s $10B capex raise, driven by memory costs, confirms what Microsoft first flagged: component inflation is now a distinct driver separate from expansion.

The market is starting to price AI infrastructure as an industrial cycle with longer duration and higher cash conversion risk.

The Three Disclosures That Repriced the Quarter

The defining shift in Q1 2026 is not the 33 percent revenue print. It is that Meta raised its full-year capex guidance to $125–145 billion from $115–135 billion and signed about $107 billion in new multi-year infrastructure commitments in a single quarter.

It also announced an 8,000-person workforce reduction explicitly framed as a shift from labor to compute. Each data point alone is material, but together they describe a fundamentally different company.

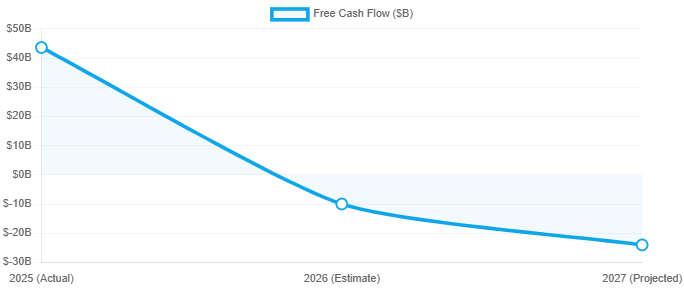

Q1 free cash flow compressed to $12.4 billion against $19 billion of quarterly capex. The full-year capex implication points to back-half acceleration that will sharpen the FCF compression curve.

Sell-side projections now anticipate Meta’s free cash flow turning negative in 2026 and reaching approximately negative $24 billion in 2027. For a business that generated $43.6 billion in free cash flow in 2025, that is a step-change in capital posture, not an incremental shift.

Silicon, Power, and Locked Commitments

The composition of the infrastructure build now spans three structurally distinct layers: proprietary silicon, third-party accelerator procurement, and energy supply.

On silicon, Meta is deploying more than 1 gigawatt of custom MTIA accelerators co-developed with Broadcom on a 2-nanometer process node. The strategic objective is to dilute exposure to NVIDIA’s pricing while preserving optionality across AMD and NVIDIA platforms.

On energy, the company has secured up to 1 gigawatt of prospective space solar capacity and 100 gigawatt-hours of long-duration storage an indication that terrestrial grid procurement is no longer sufficient for the planning horizon Meta is operating against.

On compute commitments, the $107 billion single-quarter increase in non-cancelable purchase obligations is the most consequential disclosure. Total contractual commitments have reached approximately $238 billion. These are locked-in cash outflows for hardware, cloud capacity, and energy infrastructure spanning multi-year durations.

The capex line in the income statement is now the visible expression of an obligation that is already contractually fixed.

Compute as a Tradeoff Against Payroll

Meta entered Q1 2026 with $81.2 billion in cash and marketable securities and $58.75 billion in long-term debt. The balance sheet remains strong, but the financing posture is evolving. Operating cash flow of $32.2 billion in the quarter remains substantial, yet it is increasingly insufficient to cover capex without drawing on liquidity or expanding debt.

The implicit policy is to fund the infrastructure cycle through a combination of operating cash flow, balance sheet liquidity, and incremental long-term debt issuance, while maintaining a modest dividend program of $1.35 billion paid in the quarter.

Buybacks did not appear as a focal point of the call. Alphabet’s complete pause on share repurchases earlier in 2026 is now being mirrored, in directional terms, by Meta’s prioritization of capex over discretionary returns.

The compute-versus-payroll framing is the most consequential capital allocation signal of the quarter. Zuckerberg positioned compute and people as the two dominant cost categories, where investing in one requires moderating the other, collapsing opex and capex into a single optimization problem.

Headcount is now a variable in capital allocation, not a separate decision. The May 20 reduction of 8,000 employees is the direct financial expression of this shift.

Concentration as Both Strength and Risk

Against peers, Meta occupies a distinct position. Microsoft and Alphabet deploy $185–190B capex across enterprise cloud and platforms, and Amazon’s $200B spans AWS, retail, robotics, and satellites. Meta’s $135B is concentrated almost entirely on AI infrastructure for ads and AI assistants in its apps.

This focus is both advantage and risk. The ad platform is showing real-time AI ROI, with impressions up 19 percent and average price per ad up 12 percent. AI ranking improved conversion rates and engagement, while 8 million advertisers now use generative AI tools, doubling year over year. The monetization engine is working.

The fragility sits in the absence of a diversified revenue base. Microsoft can offset depreciation with Copilot seat expansion and Azure backlog conversion. Alphabet has Cloud, Search, and YouTube as parallel monetization layers. Meta’s $135 billion infrastructure base is underwritten by a single monetization vehicle, however effective.

The Muse model family and Meta Superintelligence Labs represent the strategic optionality on AI agents as a future revenue stream. Business AIs on WhatsApp and Messenger have reached 10 million weekly conversations, but those interactions are not yet monetized. The bull case requires this surface to convert to subscription or per-conversation revenue at scale. That conversion is not yet observable in the disclosed numbers.

The Cohort Patterns Forming

Three patterns now extend across the hyperscaler cohort.

First, component inflation has been confirmed as a distinct capex driver. Microsoft flagged hardware component pressure at its fiscal Q2 disclosure. Meta has now attributed its midpoint capex raise specifically to memory pricing.

The implication is that capex guidance is no longer purely a forecast of capacity. It is a forecast of capacity plus an unhedged exposure to memory, advanced packaging, and accelerator pricing.

Second, multi-year contractual commitments are scaling faster than capex itself. Meta added $107 billion in single-quarter commitments. Microsoft’s remaining performance obligations stand at $625 billion.

These obligations represent forward cash flow commitments that constrain optionality and shift the analytical frame from quarterly capex to multi-year capital duration.

Third, the labor-versus-compute swap is now an explicit framework. Meta has articulated this most directly, but Amazon’s $200 billion capex profile combined with selective hiring discipline reflects the same logic.

The hyperscaler P&L is becoming a continuous reallocation problem between human capital and compute infrastructure.

What Determines the Cycle’s Return Profile

Three forward signals will determine whether Meta’s $135 billion midpoint converts into durable return on invested capital.

The first is Q2 2026 capex disclosure. Q1 spending of $19 billion implies sharp back-half loading. Whether actual cash deployment tracks the guidance range or extends beyond it will determine the 2027 free cash flow trajectory.

The second is the monetization profile of Meta AI and Business AIs. Ten million weekly conversations is a usage signal. A revenue line tied to those conversations would be a thesis confirmation. The absence of one through 2026 would compress the valuation multiple further.

The third is the depreciation curve from 2027 forward. The combined effect of $135 billion in 2026 capex, $107 billion in single-quarter commitments, and similar trajectories at Microsoft, Alphabet, and Amazon implies a multi-year wave of AI infrastructure depreciation hitting income statements simultaneously. That accounting expression of the current cycle has not yet been priced.

Meta’s Q1 2026 disclosure marks the point at which the AI infrastructure cycle stops being primarily a growth story and becomes primarily a capital structure story.

Advertising remains a high-margin engine, but the engine is now financing an industrial-scale capital program with deteriorating short-term free cash flow metrics, locked-in multi-year obligations, and explicit labor reallocation.

The question is no longer whether the AI capex cycle is real. It is whether the hyperscaler cohort can convert that capital into return durable enough to justify the duration risk.