Italy's 50-Gigawatt Grid Queue Is the Real Data Center Constraint

Terna's 50-gigawatt connection backlog, northern grid saturation, captive power and blue generation, the February 2026 permitting decree, why power access now prices the market

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Permitting Reform Exposed The Power Constraint

Italy has solved its data center permitting problem and exposed a larger one.

The February 2026 unified authorization decree compressed a multi-year, fragmented approval process into a single procedure with a 10-month statutory deadline.

Market coverage has read that reform as the green light for Italy’s buildout.

The reading is incomplete.

With permitting compressed, the binding constraint is now power.

Terna is holding more than 50 gigawatts of data center connection requests against a grid that can energize only a fraction of them in the near term.

The capital flooding into Italy will be sorted not by who can permit a campus but by who can power one.

The 50-Gigawatt Queue Is Mostly Virtual

The headline pipeline number overstates buildable capacity.

Terna recorded data center connection requests above 50 gigawatts across more than 300 projects by June 2025, up from 30 gigawatts six months earlier. Buildable near-term capacity is a fraction of that figure.

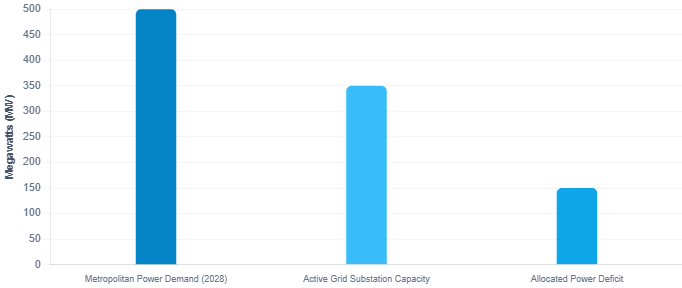

The substations serving Milan and Rome face a combined shortfall of roughly 150 megawatts by 2028 as metropolitan data center demand breaches 500 megawatts.

Terna has launched its Efficient Territorial Planning model specifically to screen out speculative and inactive requests and free saturated capacity for viable projects.

That tool exists because most of the 50 gigawatts is virtual.

Over the next 12 to 24 months, the queue will sort into projects with secured grid allocations and projects that were always speculative.

Investors underwriting Italian exposure should benchmark allocated and energized capacity, not announced pipeline.

The pipeline figure is a marketing number. The interconnection is the asset.

Investors should benchmark allocated and energized capacity, not announced pipeline. The pipeline figure is a marketing number. The interconnection is the asset the same delay now repricing data center markets across Europe.

Power Position Now Sorts The Market

Capital is not the scarce input in Italy. It is abundant and competing.

Microsoft has committed 4.3 billion euros to its Italian cloud region, Amazon Web Services 1.2 billion euros, and Gulf-backed capital has entered through the Eni and Khazna joint venture at Ferrera Erbognone.

The scarce input is a defensible power position.

Developers in congested northern zones now secure grid allocations 18 to 24 months before breaking ground and pre-fund substation upgrades that raise land costs by 10 to 15 percent.

Italy also carries among the highest wholesale electricity prices in Europe, which Polytechnic University of Milan has flagged as a direct risk to investment competitiveness.

The structural response is captive generation.

Eni is supplying its Ferrera Erbognone campus through gas generation paired with carbon capture. The utility A2A has dedicated 1.6 billion euros to data center development off the back of its own power capacity.

The market is bifurcating.

Projects with captive power or secured allocations will price and schedule on their own terms.

Grid-dependent projects carry a timing and cost discount the market has not yet applied.

The market is bifurcating. Captive-power and secured-allocation projects price on their own terms. Grid-dependent projects carry a timing and cost discount the market has not yet applied the pricing logic of clean power scarcity as the hidden constraint.

The Next Capacity Is Not In Milan

The geography of Italian data center capacity is about to shift.

Roughly 60 percent of grid connection requests are concentrated in Piedmont and Lombardy, the regions already in virtual saturation.

The buildable capacity is moving south and to the coast.

Southern Italy sits under the Single Special Economic Zone, which offers tax credits and expedited authorization across Campania, Sicily, Puglia, and other southern regions.

The Italian energy decree explicitly encourages southward distribution to access higher renewable and storage headroom.

The coastline carries the connectivity:

Sicily lands more than 20 submarine cables, and Genoa and Bari are emerging as carrier-neutral gateways to Africa, the Middle East, and India.

Terna is spending more than 23 billion euros through 2034 to lift cross-zone transfer capacity from 16 to 39 gigawatts, a plan built to move southern renewable power to northern demand.

Over 12 to 24 months, the investable Italian data center will increasingly sit outside Milan, in coastal and southern nodes with renewable headroom and subsea connectivity.

Capital that screens only the Milan market is screening the saturated half of the country.

The Investor Action Layer

Private capital should re-sequence diligence on Italian assets.

The first question is no longer the developer or the cost of capital. It is whether the asset holds a defensible power position, a secured grid allocation or captive generation.

Funds that screen on capital structure and yield before power access will allocate into projects that stall in the connection queue.

The cost of inaction is a portfolio of permitted-but-unpowered sites acquired at powered-site prices, and a southern opportunity ceded to faster movers.

Public markets hold several instruments tied directly to the constraint.

Eni, the utility A2A, and Terna are all listed. Terna’s 23 billion euro grid plan is itself an investable thesis on Italian data center growth, because the grid build is the gating input to the buildout.

Energy majors and utilities converting grid position into contracted data center revenue represent optionality not yet in consensus estimates.

Investors should benchmark which listed Italian operators hold powered land near demand, and which carry the grid mandate, rather than waiting for the revenue to surface in reported segments.

Operators should treat power partnership and geography as the first two decisions, not the last.

Entering the Milan or Rome corridor without an incumbent energy or utility partner means negotiating against the connection queue from the back of the line.

The February 2026 decree compresses permitting but does not resolve local zoning, and it does not add a megawatt of grid capacity.

Operators that sequence land first and power second will calibrate their delivery timelines to Terna’s queue rather than their own.

The Verdict On Italian Capacity

Italy has completed its transition from second-tier European market to a top destination for data center capital.

The capital is committed, the permitting is reformed, and the political alignment is in place. The constraint that remains is physical.

Power generation and grid interconnection now govern which announced projects become operational capacity and which stay on a connection list.

Italy is the clearest case in Europe because its queue is the most visibly saturated, but the same inversion is forming in every market where connection requests outrun buildable capacity.

The question for the next 24 months is not how much capital Italy can attract.

It is how much of the 50-gigawatt pipeline can actually be energized, and whether the capital now committing has underwritten the power, or only the campus.

Such constraints on access to energy will also force operators to design and deploy the most efficient systems to maximize productivity. Where every kilowatt counts, the initial designs will likely require higher capex to build the most productive IT compute capacity. This means optimizing cooling efficiencies to support high rack densities.