Why Blackstone's $2B BXDC IPO Is Not an AI Bet?

Blackstone BXDC structure, hyperscaler lease mechanics, QTS and Rowan pipeline dynamics, DLR and EQIX cap rate compression, allocation conflict risk, public-private yield arbitrage

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Blackstone is not taking an AI infrastructure bet public. It is creating a permanent exit for stabilized hyperscaler-leased data centers while keeping development economics private. BXDC investors are not buying AI growth. They are underwriting hyperscaler credit spreads at 5.75 to 7 percent gross asset yield.

The Form S-11 filed on April 10, 2026 triggered immediate analyst upgrades framing BXDC as “retail-accessible AI infrastructure.” The prospectus itself says nothing of the sort.

No ground-up development. No construction risk. No lease-up exposure. Stabilized assets only. 10 to 20 year triple-net leases to investment-grade hyperscalers. 2 to 3 percent fixed annual escalators. That is long-duration triple-net real estate priced against corporate bond yield. It is not AI growth.

Eight Years of Private Pipeline

Blackstone has been building the private pipeline that feeds BXDC since 2018. The sequencing is deliberate. 2021: QTS Realty Trust taken private at $10 billion. The foundational hyperscale platform. 2024: AirTrunk acquired at $16 billion. The APAC footprint.

Early 2026: 49 percent stake in Rowan Digital Infrastructure at approximately $3.8 billion excluding debt. Control rights over 3.5 GW across 20 sites. April 10, 2026: BXDC S-11 filed.

QTS, AirTrunk, and Rowan generate target IRRs of 15 percent plus on development. Those returns stay private. BXDC acquires what those platforms produce after stabilization. Public capital buys the post-leaseup yield.

What the S-11 Defines

The mandate is precise. Acquisition targets sit between $250 million and $1.5 billion per facility, typically 20 to 100 MW. Geographic focus: Northern Virginia, Phoenix, Austin, Ohio, and Maryland. Gross asset yields target 5.75 to 7 percent initially.

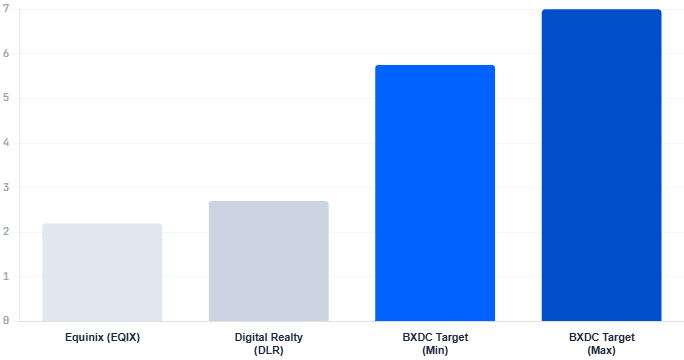

Compare the incumbents. Equinix trades at 2.0 to 2.5 percent dividend yield on a $107 billion market cap. Internally managed. Diversified exposure. Digital Realty trades at 2.4 to 3.1 percent on $70 billion. Also internally managed. Both have been net sellers of stabilized assets through joint ventures for three years.

BXDC enters with roughly twice the yield. Pure-play hyperscaler concentration. External management by BX REIT Advisors. Priority acquisition rights over qualifying Blackstone-sourced stabilized assets for 24 months post-IPO. A $25 billion near-term pipeline already under review. Target leverage approximately 40 percent long-term LTV.

The elevation of hyperscaler leases to quasi-credit instruments aligns with the broader shift in how infrastructure risk is underwritten, as examined in Why Is Meta Spending $21 Billion on CoreWeave Instead of Its Own US Data Centers?.

The Market Is Reading the Instrument Wrong

Mainstream coverage frames BXDC as retail access to AI infrastructure. That framing does not survive contact with the prospectus.

Blackstone is monetizing its data center platform at two distinct layers. Layer one captures 15 percent plus target IRRs on greenfield development inside private funds. Layer two routes stabilized post-leaseup cash flows into a public vehicle at 5.75 to 7 percent gross asset yields. Public BXDC investors are not participating in AI compute growth. They are underwriting the spread between investment-grade hyperscaler lease obligations and treasury yields.

The escalator math confirms the structure. Data center market re-leasing spreads have often run 15 to 30 percent on renewal. BXDC investors get 2 to 3 percent. Blackstone keeps mark-to-market upside in the private vehicles.

This disconnect between perceived growth exposure and actual infrastructure risk is part of a broader misalignment across the sector, as examined in Infrastructure Misalignment: The Hidden Crisis Collapsing Data Center Deals.

Three Investor Lenses

For data center operators, the binding constraint is exit repricing. BXDC is a permanent institutional bidder in the $250 million to $1.5 billion stabilized segment. Independent operators building toward a mid-tier exit must now diligence BXDC as a direct comparable. Exit cap rates tighten on the buy side. Development underwriting must calibrate to a lower terminal cap rate than 2024 assumptions supported.

For private equity and infrastructure investors, the decisive constraint is auction dynamics. BXDC’s 24-month priority acquisition rights narrow the auction funnel for large stabilized trades. Combined with the reviewed $25 billion pipeline, BXDC is a permanent marginal bidder in the mid-tier stabilized band. Funds that underwrote 2024 to 2025 exit cap rates need to rerun their terminal assumptions. The Blackstone ecosystem is now a structural competitor in stabilized trades, not only a seller.

For public equity investors, the competitive shift is multiple compression. Equinix and Digital Realty face a pure-play hyperscaler credit vehicle yielding double their dividends. Retail liquidity rotates on the margin over 18 to 24 months as BXDC seasons. The incumbents hold diversification, interconnection density, and operational track record as defensive moats. BXDC holds yield and focus. Over time, the category reprices.

Where the Capital Moves Next

Cap rate compression in Northern Virginia and Phoenix stabilized trades accelerates through 2026. The $250 million to $1.5 billion band now has a permanent institutional bidder backed by Blackstone’s sourcing advantage. Secondary hubs including Ohio, Maryland, and Austin follow as BXDC deploys IPO proceeds.

Tenant concentration remains the key governance gap. If the seed portfolio exceeds 50 percent exposure to AWS, Microsoft, or Meta, BXDC becomes three-name credit risk with real estate optics. Related-party pricing on asset transfers from Blackstone affiliates is the largest unknown in the S-11.

Investors positioning now face an information asymmetry they cannot close. Those waiting for disclosure will pay prices that reflect Blackstone’s edge. BXDC is not the start of institutional capital in AI infrastructure. It confirms stabilized data centers as the third pillar of institutional real estate.

Great post! Very intriguing play here with BDXC