Is CoreWeave’s $8.5B Deal the GPU Asset Class Moment?

How investment-grade debt, hyperscaler contracts, and power constraints are redefining AI infrastructure as institutional-grade assets

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

How the Deal Is Structured

CoreWeave closed an $8.5 billion delayed draw term loan on March 31, 2026, with $7.5 billion initial capacity, expandable to $8.5 billion, maturing in 2032. Pricing is SOFR plus 2.25 percent floating and about 5.9 percent fixed. Morgan Stanley, MUFG, Goldman Sachs, and JPMorgan arranged the facility, with Blackstone Credit and Insurance anchoring.

The structure is non recourse and ring fenced to a dedicated entity. Repayment is tied solely to that vehicle, secured by GPU clusters and contracted revenue, including an estimated $19 billion backlog from Meta. Proceeds fund delivery of contracted services and expansion of high performance compute capacity.

This is CoreWeave’s fourth DDTL facility, and the progression across these deals represents one of the fastest cost-of-capital compressions in technology infrastructure finance. DDTL 1.0 in 2023 priced at around 15% floating on $2.3 billion, secured primarily by GPU hardware. By July 2025, DDTL 3.0 priced at SOFR + 4.00% on $2.6 billion, supported by OpenAI contracted revenue.

DDTL 4.0 now prices at SOFR + 2.25% on $8.5 billion, carries an investment-grade rating, and is anchored by Meta. In under three years, CoreWeave has moved from high-yield equipment financing to A-rated institutional infrastructure debt. That level of compression is not driven by negotiation, but by a fundamental reclassification of the asset by lenders.

This rapid compression in cost of capital reflects the broader financialization of AI infrastructure as an asset class, as explored in CoreWeave: The Financialization of AI Infrastructure.

What the Rating Actually Means

The rating is the event. The size is secondary. It shifts AI infrastructure into institutional portfolios and resets pricing, risk, and eligibility.

Before March 31, 2026, AI infrastructure financing was the domain of private credit and tactical funds accepting risk premiums of 10–15%. High-yield ratings reflected two genuine concerns: GPU hardware depreciates faster than traditional infrastructure assets, and AI demand was not yet proven to be durable contracted revenue rather than speculative enterprise spending. Both concerns were reasonable. Both have now been adjudicated by Moody's and DBRS in the opposite direction.

Investment grade status unlocks a different capital pool. Pension funds, insurers, and sovereign wealth funds require long duration, A rated instruments. CoreWeave’s DDTL 4.0 meets that requirement, backed by hard assets and contracted demand. Insurance capital participation signals a structural shift in who finances AI infrastructure and at what cost.

For PE and infrastructure funds, the primary mechanism to internalize is this: CoreWeave now deploys capacity at a borrowing cost that no non-investment-grade competitor can match. At SOFR + 2.25%, the cost of capital advantage compounds directly into deployment speed. Faster deployment captures contracts faster. Larger contract backlogs support larger future financing facilities at tighter spreads. The moat is self-reinforcing and it began on March 31, 2026.

This transition into institutional portfolios mirrors the wider repricing underway across U.S. AI infrastructure financing, as examined in Is $121B in U.S. Data Center Lending Justified by AI Demand?.

The Structural Consequences for Institutional Capital

Three underwriting shifts follow from this transaction and apply to every infrastructure allocation in this category going forward.

The first is offtaker primacy. Rating agencies are underwriting the hyperscaler customer, not the GPU hardware. Long-term take or pay agreements from Meta or Microsoft function as near sovereign credit support. The A3 rating on CoreWeave reflects offtaker strength as much as operating performance. The correct framework is project finance, where the contract is the primary credit instrument and the asset is the recovery floor.

The second is execution-linked borrowing. DDTL 4.0 ties draw capacity to operational deployment milestones rather than hardware acquisition. Borrowing scales as assets reach stabilization, removing pre-funding drag and aligning lender and borrower incentives. This structure improves on traditional revolving credit or term loan B models and is quickly becoming the standard for institutional AI infrastructure debt. Funds evaluating similar opportunities should expect this, not treat static-draw facilities as equivalent.

The third is energy embedded in covenant terms. Power availability is explicitly written into the facility structure. The lending syndicate has identified energy, not GPU supply or capital, as the binding operational constraint. This reflects a fundamental reality: infrastructure investors must treat power access as a first-order diligence variable. Any AI infrastructure allocation that does not prioritize energy in underwriting is incomplete.

Where Capital Moves Next

The next inflection point is not in the United States. It is the first investment-grade AI infrastructure financing in an emerging market geography.

DDTL 4.0 is built on offtaker backed credit, execution linked borrowing, and power covenants, and is transferable. In emerging markets, sovereigns, telecom operators, and hyperscalers can replicate Meta’s role by anchoring revenue, but execution remains constrained by sovereign, currency, and regulatory risk.

Development finance institutions can catalyze the first transactions. Funds structuring alongside DFI credit enhancement gain early access to scalable deal flow, as seen with CoreWeave. The current window will compress as capital converges.

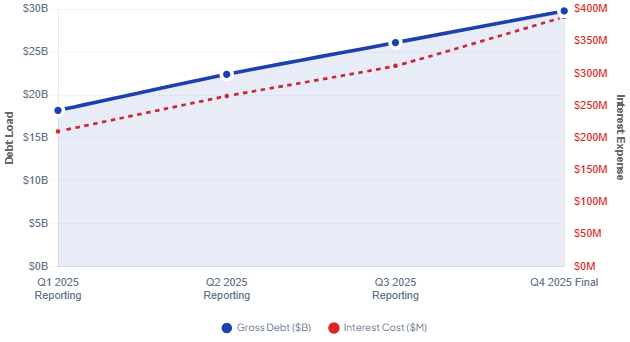

CoreWeave’s risk profile remains material. Customer concentration underpins the rating. A slowdown or insourcing by Meta weakens the credit base. Interest expense reached $388 million in Q4 2025, with total debt near $29.8 billion. Achieving positive free cash flow depends on sustained GPU utilization and backlog execution. These risks define underwriting discipline. They do not negate the structural shift.