Is $121B in U.S. Data Center Lending Justified by AI Demand?

Power Certainty, Capital Structure Discipline, and Sponsor Scale Will Determine Whether the AI Infrastructure Cycle Can Sustain $121.9 Billion in Committed Lending

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

In 2025, lenders committed roughly $121.9 billion in credit to U.S. data centers, one of the largest single-year capital allocations into digital infrastructure in the country.

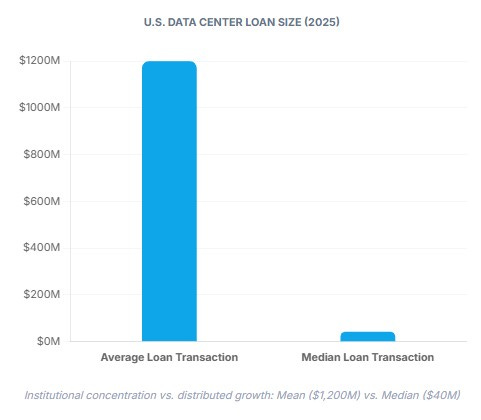

With an average loan of $1.2 billion and a median of just $40 million, the market is dominated by a few very large transactions rather than broad small-scale financing, signaling institutional concentration over distributed growth.

This is more than a cyclical uptick it reflects a structural repricing of data centers as critical AI and cloud infrastructure. The underwriting bar has shifted, raising the key question: is AI demand durable and bankable enough to support this scale of credit without refinancing or delivery risk?

The Demand Case: AI Is Real, Not Theoretical

AI training workloads require multi-hundred-megawatt campuses with high-density GPU clusters, advanced liquid cooling, and redundant power far larger and more intense than prior cloud-era builds.

Hyperscalers are pre-leasing significant capacity before delivery. Vacancy in North American markets is near historic lows, and much of the under-construction supply is already contracted. Absorption is outpacing energization in major hubs.

Expansion remains credible, anchored by large capital programs from highly creditworthy companies. Still, strong demand alone doesn’t justify aggressive credit timely energization, lease-up, and sustained pricing power are essential for the capital structure to hold.

The Credit Structure: Commitment vs. Deployment

The $121.9 billion reflects committed credit, not fully drawn proceeds. Much of it sits in revolving facilities or expandable programs, letting sponsors phase construction with tenant ramp.

This structure gives flexibility sequencing builds, reducing idle capital, and aligning debt with leasing milestones. But it also exposes lenders to timing risk: delays in lease-up or power delivery complicate the transition from construction financing to stabilized debt.

Mini-perm loans remain the cycle’s stress point. These short-duration construction loans assume refinancing at stabilization, and shifts in rates or market sentiment can quickly erode equity.

Investors must model draw schedules, tenant concentration, and maturities carefully committed versus deployed capital defines the risk profile.

The Power Variable: The Real Underwriting Constraint

Capital allocation is increasingly guided by grid certainty. States with available generation capacity, faster interconnection timelines, and clearer permitting pathways are attracting a disproportionate share of lending.

Where power is limited, project delivery risk escalates. Interconnection queue uncertainty, transformer procurement delays, transmission bottlenecks, and water availability for cooling are now central to lender diligence, not secondary operational details.

AI demand cannot monetize megawatts that cannot be energized. A signed lease without guaranteed power delivery produces no cash flow, making utility agreements and energy strategies as critical as tenant credit quality.

Power availability has become the key gating variable in this credit cycle. Simply put, capital now follows the electrons.

The Concentration Effect: Scale Wins Capital

The gap between the $1.2B average loan and $40M median shows capital is concentrated among mega-campus developers. A few large operators capture most syndicated credit.

Syndication spreads risk across banks, but execution remains with scaled sponsors who benefit from lender ties, procurement leverage, and multi-phase land control.

Expandable credit has become a competitive moat. Experienced sponsors secure bigger, cheaper, and more flexible financing, while smaller developers face higher barriers. Scale drives preference for repeatable platforms over isolated projects.

The Bottom Line

AI demand is strong enough to justify elevated construction volumes. The underlying tenant base is credible, and the structural shift toward AI-driven workloads is durable.

Whether that demand justifies $121 billion in committed lending depends on disciplined underwriting. Power certainty, sponsor execution capability, and refinancing resilience will determine whether commitments translate into stable long-term infrastructure assets.

The demand thesis is robust. The delivery constraints will determine whether this credit cycle proves durable or exposed.