Infrastructure Misalignment: The Hidden Crisis Collapsing Data Center Deals

Site Control vs. Development Viability, Power Queue Timelines, Fiber Build-Out Sequencing, Pre-Construction Capital Stack Collapse, IRR Compression Mechanics, What Disciplined Capital Does Differently

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

The primary failure mode in global data center development is pre-construction collapse. Sponsors have long treated site control, power availability, and fiber connectivity as sequential workstreams: confirm the land, then the power, then the connectivity. That model held when timelines were shorter and infrastructure constraints were local and manageable. Every dollar of misalignment between those three constraints now lands on the capital stack before a foundation is poured.

The scale of that failure is visible in the pipeline data. The global development pipeline reached 241 gigawatts of electricity-equivalent demand by late 2025. That figure rose 159 percent within a single year. Fewer than one third advanced into active construction. U.S. construction capacity under active development fell from 6,350 megawatts to 5,994 megawatts. Primary market vacancy hit 1.4 percent an all-time low. Capital is present. Tenant demand is present. The infrastructure evaluation model that should govern capital deployment is not.

The Constraint Nobody Is Pricing

Fiber is the constraint most consistently absent from early-stage underwriting and most likely to surface catastrophically late in the development process. AI-grade workloads require roughly ten times the fiber capacity of legacy compute environments. U.S. data center bandwidth consumption tripled between 2020 and 2024. Fiber prices rose approximately 70 percent between 2021 and 2024. The infrastructure reality is not matching the underwriting assumption.

Underground fiber construction costs between $60,000 and $120,000 per mile. Civil engineering, trenching, and rights-of-way account for up to 45 percent of total expenditure. A regional operator advancing a secondary market site discovered that the nearest dark fiber infrastructure required multi-mile construction across railroad easements and several municipal jurisdictions. The permitting timeline extended project delivery more than a year beyond the original schedule. The underwritten return did not survive the revision.

A second fiber risk is structural. Many sites that appear fiber-served in standard connectivity databases connect only at the manhole level. Fiber meets at the street rather than entering the building. For colocation operators whose return economics depend on cross-connect revenue, that distinction determines asset quality and it is invisible to sponsors relying on standard infrastructure maps.

What the Market Has Gotten Wrong

The industry has long assumed fiber would follow the data center. That assumption held when compute density was moderate and secondary markets had sufficient routes within economical proximity. It does not hold now because hyperscalers specify dual diverse fiber routes as a condition precedent to lease execution, not as a lease addendum. The negotiation happens at site selection. The site either satisfies the specification or it does not.

How the Constraints Compound

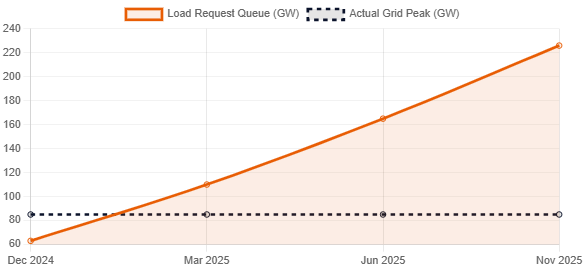

Power interconnection queues apply pressure at a different layer. The average wait from application to commercial operation across major U.S. markets now runs approximately five years. In ERCOT, the large load interconnection queue expanded from 63 gigawatts in December 2024 to 226 gigawatts by November 2025. That expansion occurred against a grid that has never sustained peak demand above 85 gigawatts. Formal approvals covered 7.5 gigawatts of that total. The timeline mismatch between developer expectations and infrastructure reality is the market’s operating condition.

Site entitlement adds a third layer of compounding risk. Community opposition has blocked an estimated $18 billion in U.S. data center projects and delayed a further $46 billion over two years. In Home Rule jurisdictions, a planning commission recommendation is reversible by a council vote. That veto mechanism does not appear in standard zoning analysis. It has terminated projects with committed land and signed letters of intent at advanced development stages.

Cable procurement lead times reached sixty weeks during the most recent supply cycle. Dark fiber indefeasible rights of use offer total cost-of-ownership savings exceeding 60 percent relative to managed carrier services at AI-grade bandwidth thresholds. Those savings are accessible only to sponsors who secure the route before the development thesis is committed to paper.

Three Investor Lenses

Independent operators face this constraint at site selection. The binding variable is fiber path diversity and carrier-neutral on-site access not the existence of fiber in the general market area. Operators who defer fiber diligence past site control will consistently acquire properties that cannot serve the tenant profile the project was designed to attract.

Private equity and infrastructure investors face IRR compression as the direct financial consequence. One month of construction delay on a 60-megawatt facility costs an estimated $14.2 million in foregone revenue and $1.8 million in monthly interest carry. A three-month delay compresses development IRR from approximately 17.1 percent to 12.6 percent. That compression eliminates the return premium that justified development risk over investment-grade alternatives.

Public equity investors face valuation dispersion the market has not yet priced. Platforms with proactively secured dark fiber routes and on-site carrier-neutral infrastructure are a different asset class from platforms relying on managed carrier services. The difference appears in lease execution rates, tenant quality, and pipeline reliability. Analysts evaluating this sector through a generalized infrastructure lens will consistently misattribute the source of that dispersion and misprice the assets accordingly.

Six Disciplines That Separate Positioned Capital

Move fiber assessment to the site filter stage. Before site control is established, commission an engineering-grade fiber path analysis that confirms carrier-neutral access, route diversity, and clear easement conditions. Sites that fail this filter are eliminated before capital is committed.

Require a dark fiber path inventory as a condition precedent to investment committee approval. The inventory must confirm whether routes are lit or dark, ownership structure, easement profile, and activation timeline. Carrier representations without independent engineering verification do not satisfy this condition.

Model fiber build-out cost and timeline as the base case for every secondary market site. The working assumption is that no usable dark fiber exists within required proximity. Sites with confirmed access are underwritten at a premium to that base not the reverse.

Structure acquisition agreements to include infrastructure milestones as conditions precedent to closing. A site with clear title and clean zoning is not a viable development site if fiber path diversity has not been confirmed.

Apply a minimum 20 percent infrastructure contingency to any project requiring new substation construction or fiber build-out. The five percent soft cost contingency was calibrated for a market that no longer exists.

Pursue dark fiber rights of use as pre-development capital allocation, not a construction-phase expenditure. Long-term access secured before lender engagement produces cost advantages that compound over the life of the asset.

You either confirm the infrastructure constraint before capital is committed or you absorb it after. The investors who rebuilt their underwriting sequence around that principle made the decision early, before the constraint was widely understood. That window is narrowing. The sequencing decision is the edge.