Hyperscaler Dominance: The Real Threat to Fiber Investor Returns

Wholesale price collapse, vertical integration, IRU compression, emerging-market scarcity, route selectivity discipline

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

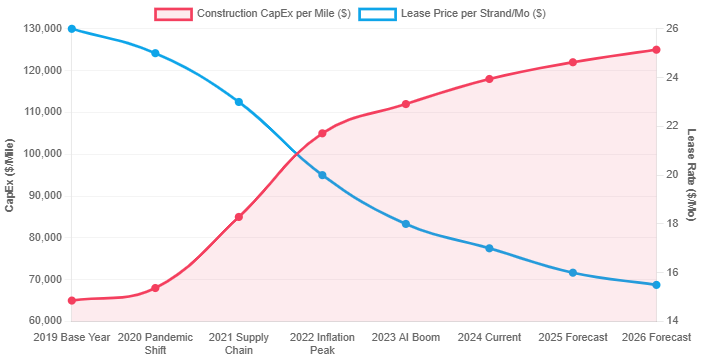

Fiber pricing power has collapsed in every primary corridor where hyperscalers have decided to build.

The old underwriting paradigm assumed the largest buyers would stay buyers.

They have become builders. Capital deployed against the old paradigm now sits in an asset class that cannot reset its price.

The compression is being driven by three converging forces.

AI training has restructured east-west traffic in a way that rewards owned fiber over leased fiber.

Hyperscalers have moved from procuring third-party capacity to building proprietary capacity at scale.

Alternative network operators have aggressively overbuilt the same primary corridors hyperscalers are now bypassing.

Supply expands faster than addressable third-party demand.

The buyers setting the price can credibly walk.

This shift where hyperscaler capital moves upstream and rewrites the economics of underlying infrastructure layers aligns with the broader pattern outlined in How Private Capital Is Rewriting The Data Center Playbook.

The Mechanism

The mechanism is straightforward.

AI workloads pushed traffic off the public-facing front door of the data center, moving it into the back end where server-to-server synchronization across GPU clusters depends on deterministic latency.

Leased bandwidth cannot guarantee it. Owned fiber can. So hyperscalers stopped renting.

Meta committed up to $6 billion to Corning for fiber-optic cable through 2030, while Microsoft locked in over $8 billion of dark-fiber contracts for its campus interconnect.

Meta’s Project Waterworth, a 50,000-kilometer subsea system spanning five continents, is structured as a sole-owner asset, where the consortium model that once gave telecom operators a share of intercontinental capacity no longer applies.

Google has invested in over thirty subsea cables.

These are not opportunistic deals.

Together they form one program that removes third-party fiber from the stack at every layer.

When the largest buyer in a market becomes its largest builder, the buyer-seller relationship inverts.

Routes that hyperscalers self-build are now priced against their internal cost of construction, not against what the market would bear if they were still leasing.

This vertical integration of compute, hardware, and network layers mirrors the strategic control shift described in Open Compute Project: The Hardware Moat Facebook Built and Gave Away.

What the Market Has Wrong

The industry has long assumed that fiber demand growth and fiber pricing power move together.

That assumption held when fiber was a contestable supply layer. It held when the largest buyers needed third-party operators to build the routes they could not. It does not hold now.

The largest buyers can build. They are building. They have made the decision public.

Demand has never been higher. Pricing power has never been weaker.

The variables have decoupled. They will not recouple.

If your model still links them, you are pricing against a market that no longer exists.

Time Is the Binding Constraint

Supply-side friction has compounded the problem. It has not relieved it.

Fiber cable lead times have stretched to levels not seen since the early 2000s buildout.

Construction costs have moved meaningfully higher. Municipal approvals run six to nine months at the floor. Urban make-ready engineering routinely runs over a year. A single railroad crossing can take more than twelve months per easement.

Time is the binding constraint. Not just cost. Time.

A regional operator committed to a campus four miles from existing fiber. The dual-diverse build pushed seven figures of capex. It added two years to the schedule before the first customer was lit. By the time the route was deliverable, the anchor tenant had restructured the footprint. They signed a long-duration IRU with the hyperscaler that arrived first.

The fiber got built. The economics did not.

Hyperscalers face the same supply constraints. They absorb them differently. Multi-year planning cycles let them commit capital before counterparties close financing. In a constrained environment, that timing advantage wins allocation.

The third-party operator is not just competing on price. They are competing on time. They are losing on time.

Three Investor Lenses

For independent operators, the binding constraint is route selection.

The two-mile rule has hardened into law. Sites beyond two miles of existing fiber generate build-out costs and timeline risks that destroy returns before any other variable matters.

Physical verification of route diversity is non-negotiable. Two paths that look separate on a map frequently share the same duct. The discovery, made late, kills the project.

Operators that win in this market have stopped underwriting sites. They underwrite fiber. The site selection follows.

For private equity and infrastructure investors, the decisive constraint is the gap between debt service and stabilization.

Lead times that run over a year at the long end stretch the period of negative carry well beyond what 2021-vintage models priced in. IRR compression follows mechanically.

Multi-billion-dollar joint-venture structures across operators and infrastructure funds spread balance-sheet exposure. They do not solve the underlying margin problem on commoditized routes.

The discipline that survives this cycle is route-level scarcity underwriting. Duct exclusivity. Right-of-way control. IRU positions taken before the market reprices the constraint.

For public equity, the dispersion is widening.

Fiber operators with concentrated exposure to Tier 1 corridors that hyperscalers are bypassing trade as commodity assets, regardless of route mileage. Operators with carrier-neutral platforms and interconnection ecosystems carry valuation premiums that mileage cannot replicate.

Investment-grade credit spreads on hyperscaler-tenanted data centers have widened. Industrial spreads have tightened.

Debt capital is pricing concentration risk into the cost of funding before equity markets have caught up.

Resilient Underwriting Disciplines

Reorder your site selection filters.

Fiber availability and route diversity precede land, power, and tax. The two-mile rule applies. Anything beyond is a project-defining risk, not a manageable one.

Verify route diversity physically.

Two networks that look separate on a map often share duct. The diligence cost of verifying separation is trivial. The underwriting cost of discovering shared duct after closing is not.

Consider replacing open-market exposure with IRU positions and equity stakes in regional fiber carriers.

Twenty-to-thirty-year strand-level rights function economically as ownership. They preserve pricing leverage on routes that would otherwise be commoditized.

Underwrite carrier-neutral facilities and interconnection ecosystems differently from single-carrier or captive-route assets.

Facilities that attract fiber carry pricing resilience. Facilities that depend on fiber do not.

Reroute capital toward markets with genuine scarcity.

Emerging market fiber-to-data-center positions sit where altnet competition is limited and infrastructure deficits create real scarcity rents. The risk-adjusted return profile is materially better than crowded Tier 1 corridors. The execution capability requirement is real. So is the premium.

Model stranded-asset risk explicitly.

Powered land without secured fiber is a stranded asset in formation. Fiber on a route a hyperscaler has already claimed is capital deployed into a margin that no longer exists.

Scarcity now determines fiber returns. Volume does not.

You are either underwriting against scarcity, or you are deploying capital against a margin the market has already taken.