How Can Fiber Investors Thrive in a Market Full of Competition?

Fiber demand is booming, but returns are shifting. In this piece, we discuss how smart investors are adapting to margin pressure with strategic routes, bundled value, and hyperscaler alignment.

Welcome to Global Data Center Hub. Join 1400+ investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

In This Issue

Global Data Center News Roundup — The biggest AI infrastructure moves in North America, Europe, APAC, and MEA.

The Fiber Illusion — Why fiber-to-data center plays are losing pricing power across hyperscale corridors.

Margin Compression, Market Saturation — How hyperscalers, altnets, and marketplaces are crushing legacy IRRs.

Strategic Forecast — What investors, operators, and lenders must do now to avoid value traps in 2025.

Dear Friends,

Fiber has long been the quiet backbone of the digital economy.

But in 2025, that backbone is bending, under the weight of increased capacity, margin compression, and hyperscaler bypass.

From Virginia to Dublin, from Seoul to São Paulo, the routes that once promised high returns are now under pressure. Pricing is collapsing. Competition is relentless. And hyperscalers are building faster than the market can react.

This isn’t just a temporary dip. It’s a structural reset.

In this issue, we break down why the fiber-to-data center thesis is cracking and what disciplined capital must do next to avoid stranded assets, disappearing margins, and obsolete plays.

Global Perspective: What’s Happening in Data Centers Around the World

North America

EdgeCore to Invest $17B+ in 1.1GW Virginia Campus. EdgeCore’s massive hyperscale build signals that Northern Virginia remains central to the AI infrastructure race. Despite grid headwinds, land and fiber access are keeping Ashburn’s dominance alive.

11GW Campus Planned Outside Amarillo, Texas. Former Texas Governor Rick Perry backs an 11GW data center campus, potentially the world’s largest. It marks the fusion of energy, politics, and next-gen AI compute ambitions in the U.S. heartland.

Crusoe and Redwood Power Data Center with Old EV Batteries. Crusoe and Redwood Materials are repowering data centers using second-life EV batteries, a radical shift in energy strategy. This isn’t just sustainability theater. It’s a glimpse into how alternative storage, circular energy systems, and edge-aligned innovation are reshaping the economics of AI compute.

Europe

Amazon’s £40 Billion Investment in the UK. Amazon’s largest European play ever is a landmark commitment to UK cloud and AI infrastructure. The investment will anchor GPU-powered campuses and create thousands of jobs across the UK.

Ark + Nebius + NVIDIA Collaboration in Surrey. The deployment of NVIDIA processing units at Ark’s UK campus reflects the emerging GPU cluster trend and strategic alignment with sovereign and enterprise AI infrastructure needs.

Ravenscraig AI Campus (Scotland). A £3B plan to transform a former steelworks into an AI data center campus reveals how data center growth is driving industrial site reactivation and economic revival.

Asia-Pacific

Thailand’s $15.4 Billion AI Infrastructure Push. Thailand is placing a bold $15.4B bet on AI infrastructure to position itself as Southeast Asia’s AI hub. The move shows growing sovereign interest in compute sovereignty and economic leadership.

Alibaba Cloud to Launch Second Data Center in South Korea. Alibaba’s second data center in South Korea reflects the intensifying competition among cloud providers in Northeast Asia. It also hints at increasing demand for localized AI and digital services across the Korean peninsula.

ST Telemedia Launches Japan Data Center. STT’s entrance into Japan demonstrates growing demand for sovereign-neutral, multi-region cloud and AI infrastructure in the APAC region.

Middle East & Africa

Middle East and Africa DC Growth Heats Up. From Saudi Arabia’s AI zone investments to UAE and African builds, MEA is seeing a surge in state-supported data center development. Energy abundance and sovereign ambition drive the shift.

South America

Enegix Mulls 100MW Crypto DC in Brazil. Even as the crypto boom softens, Brazil’s energy advantage is drawing attention from AI and compute investors looking for low-cost, high-capacity sites.

Sponsored By: Global Data Center Hub

Your trusted source for global AI infrastructure analysis. Every week, we break down the trends shaping the future of data centers, cloud, and AI, from emerging markets to hyperscale battlegrounds.

Subscribe to get expert insights delivered to your inbox.

What’s the Smartest Way to Invest in Fiber as AI Demand Surges?

Executive Summary

Fiber-to-data center markets are saturated with competitors, from telcos to hyperscalers to altnets.

Pricing power is eroding as supply outpaces demand in key interconnection corridors.

High inflation, inflated valuations, and slower-than-expected take-up rates are shrinking margins.

Asset quality and differentiation (not scale alone) are becoming the key investment filters.

Smart capital is shifting away from undifferentiated fiber plays and toward dark fiber, bundled services, and hyperscaler-aligned corridors.

Why This Matters

The fiber buildout story has long been a growth narrative: fast lanes to the cloud, 100G to the rack, and dark fiber deals that promised steady, scalable income.

But in the AI era, that story is breaking down.

As hyperscalers insource capacity and new entrants flood metro and long-haul markets, the core economics of fiber are under pressure. Many routes are overbuilt. Most markets are overcompeted. And nearly every player is competing on price instead of value.

The result?

Fiber-to-data center connectivity, a historically defensive, high-margin asset class, is quietly becoming a commodity.

What’s Driving the Margin Collapse?

1. Hyperscalers Are Rewriting the Rules

Amazon, Google, and Microsoft aren’t just buying capacity, they’re building it. In 2025 alone, the big four are expected to spend more than $300 billion on infrastructure, much of it bypassing third-party fiber altogether.

Rather than lease metro or long-haul routes, they’re:

Acquiring IRUs at aggressive rates

Building proprietary interconnect rings

Leveraging their scale to drive prices down across entire markets

In short: they’re removing intermediaries. And when your biggest customers become your biggest competitors, margin erosion is inevitable.

2. Metro Networks Are Getting Overbuilt

In cities like Northern Virginia, Dublin, and Singapore, multiple providers are laying redundant fiber within the same corridors.

In Spain, 65% of premises now have coverage from more than one FTTP provider.

In the U.S., over 2 million fiber passings in 2023 overlapped with existing infrastructure.

While this improves redundancy, it devastates pricing.

The result? Utilization rates below 50% in many Tier 1 corridors, even as capex and route mileage continue to climb.

3. Pricing Power Is Disappearing, Fast

Wholesale pricing for long-haul and metro connectivity has collapsed:

55% drop in U.S. intercity fiber prices year-over-year

49% decline in Europe’s metro market

25–30% average reduction in global transport pricing

This is not a cyclical dip. It’s a structural reset.

With lit services increasingly indistinguishable across providers, customers are choosing the lowest cost. RateXchange and other fiber marketplaces have only accelerated the race to the bottom.

4. Costs Are Up. Returns Are Down.

Fiber builds aren’t getting cheaper.

Labor costs are up 20–30% since 2020.

Equipment lead times are still volatile post-COVID.

Interest rates are pushing the cost of capital well above historic averages.

Meanwhile, expected IRRs are being squeezed by:

Delayed take-up due to slower enterprise adoption

Shorter lease terms from hyperscaler tenants

Price competition from municipally backed or open-access networks

Many fiber providers are finding that their original investment theses are being impacted as a result.

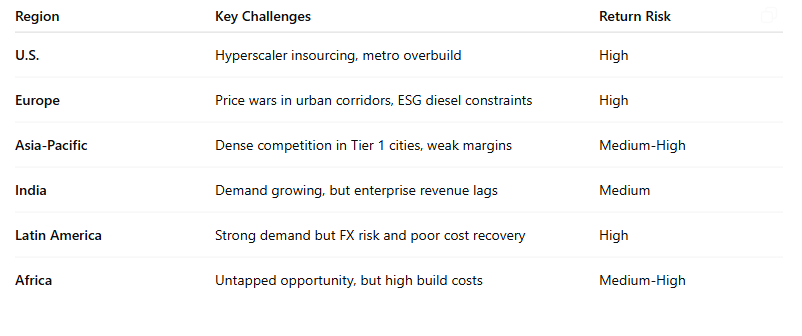

Global Risk Hotspots: Where Compression Bites Hardest

Where the Legacy Playbook Fails

Too many investors are still using old rules:

Assume long-haul scarcity = pricing power

Underwrite based on take-up forecasts that assume low competition

Chase route mileage without evaluating overlap or market density

Price deals based on 2021–2022 EBITDA multiples

This thinking doesn’t hold in 2025.

Valuations are disconnected from cash flow realities. Multiples over 20x are common in markets where margin compression is accelerating and competition is intensifying.

In this environment, volume isn’t the answer.

Rethinking the Fiber Investment Playbook

1. Prioritize Control, Not Coverage

Strategic routes—those that enable hyperscaler campus interconnects, cross-border cloud regions, or low-latency trading paths—are still high-value. But only if you:

Control the duct and rights-of-way

Own IRU terms that allow escalation and route exclusivity

Can bundle power, edge compute, or cloud interconnect

In a commoditized market, exclusivity is the last remaining moat.

2. Bundle to Defend Margins

Fiber-only offerings are dead weight in high-density metros.

Top-performing platforms are:

Integrating cross-connect, edge compute, and managed services

Offering differentiated SLAs for enterprise and fintech clients

Monetizing uptime, not just bandwidth

One high-quality enterprise customer with security and latency needs is often worth 10 unmanaged dark fiber routes.

3. Focus on Future-Proof Segments

Some segments still offer strong returns:

Rural markets backed by government funding (e.g., BEAD in the U.S.)

Hyperscaler corridor densification where real estate is constrained

Edge markets in AI cluster zones where capacity is scarce

And across all segments, long-term IRUs beat short-term lit leases every time.

Final Take: Scarcity No Longer Guarantees Return

Fiber still matters.

But in 2025, it no longer guarantees differentiation, profitability, or investor alpha.

The winners in this wave aren’t the biggest builders.

They’re the most disciplined underwriters. The best route strategists. The ones who know that in a world where everyone is selling glass, the real power lies with those who own the lanes hyperscalers must use and can’t build fast enough on their own.

If you’re still investing in fiber like it’s 2018, the margins won’t just disappoint. They’ll disappear.

Tell us what you thought of today’s email.

Good?

Ok?

Bad?

Hit reply and let us know why.

PS... If you're enjoying this newsletter, share it with a colleague.

Have a great rest of your weekend.

Talk to you tomorrow,

Obi