Heat Is the New Bottleneck: Why AI Density Is Stranding Air-Cooled Assets

Thermal density inflection, liquid-cooling economics, retrofit stranding risk, PUE and water exposure, tenant-market bifurcation, emerging-market cooling penalty

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Cooling has become the variable that decides which data center assets hold value and which become liabilities.

The old underwriting paradigm treated cooling as an operational line item, a fixed percentage of facility energy that varied little across deals.

That paradigm is now wrong, and continuing to apply it means buying stranded assets at prices that assume they can host the workloads they cannot.

The Density Inflection

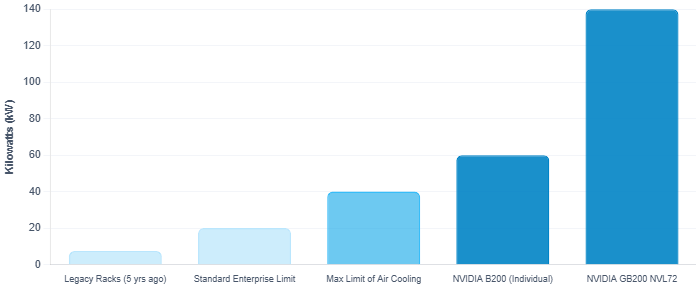

The driver is thermal density. Each generation of AI compute dissipates more heat per rack than the last, and the step-change is not incremental.

A standard enterprise rack five years ago drew 5–10 kilowatts. A modern AI training rack built on NVIDIA’s current architecture draws an order of magnitude more.

The NVIDIA B200 carries a thermal design power up to 1,200 watts per GPU in liquid-cooled configuration. The GB200 NVL72 rack system approaches 140 kilowatts.

That is roughly ten times the heat load of the enterprise rack that legacy facilities were engineered to absorb.

Air cannot move that heat. This is physics, not preference.

Air has low specific heat capacity, while AI rack heat is concentrated directly on the chips, not dispersed across room airspace.

Standard air-cooled infrastructure tops out near 40 kilowatts per rack before throttling and thermal failure begin.

Liquid is approximately four times more thermally conductive than air for the same volume.

Some manufacturers have already abandoned air-cooled variants of their newest hardware entirely.

The market has not finished absorbing what that means.

The Retrofit Trap

The industry has long assumed that cooling architecture is a retrofit decision that an air-cooled facility can be upgraded when demand arrives.

That assumption held when rack densities crept up slowly and air handled the load with margin to spare. It does not hold now.

Converting an existing air-cooled facility to liquid runs on the order of two to three million dollars per megawatt. That is a stranding cost, not an upgrade cost.

It compresses returns on every legacy asset in a portfolio, and it arrives precisely when the highest-value tenants are walking past those assets.

Here is the counterintuitive part. Liquid cooling does not carry a structural capital premium at high density.

Capital cost analysis of comparable air and liquid designs shows that at high rack densities, liquid-cooled builds come in at or below air-cooled cost.

Eliminating chillers, room air handlers, and containment offsets the cost of pumps, piping, and coolant distribution.

The premium is not in building liquid-ready. The premium is in not building it, then paying to convert later.

Consider a regional operator that built a high-quality air-cooled facility on a twenty-year asset life assumption. The building is sound, power is contracted, and the location is strong.

Then the tenant pipeline shifts to AI workloads requiring 100-kilowatt racks, and the facility cannot host them without a multi-million-dollar-per-megawatt conversion that was never in the model.

The asset did not fail. The underwriting did.

Time Is the Binding Cost

Supply-side friction makes this worse, and time is the binding cost.

Hardware refresh cycles run 12 to 18 months. Physical facilities are underwritten on twenty-to-thirty-year lives.

The mismatch is structural.

A facility designed for 30–50 kW racks cannot easily host the next generation without a cooling retrofit, and traditional real estate underwriting does not capture this obsolescence curve.

The constraint is not whether liquid cooling works.

It is whether the asset was designed before the demand it now has to serve.

Three Lenses on the Same Constraint

For independent operators, the binding constraint is qualification. Can the facility certify support for 100-kilowatt-plus racks with liquid cooling? If not, the highest-density tenant category is closed, and the question is no longer electrical capacity alone.

Hyperscale customers now ask for water usage effectiveness numbers and liquid-cooling certification as core leasing criteria. An operator who cannot answer is structurally excluded.

For private equity and infrastructure investors, the decisive variable is stranding risk priced against schedule. A legacy air-cooled asset acquired at a multiple that assumes AI-tenant optionality is mispriced if that optionality requires undisclosed retrofit capital.

You must underwrite the conversion cost explicitly, model the schedule risk of executing it in a live facility, and discount the assets that cannot make the transition at any reasonable cost.

For public equity, the divergence is already forming between operators positioned for liquid-cooled density and those carrying air-cooled portfolios into an AI-tenant market.

The dispersion will widen as efficiency standards tighten and as regulatory water exposure converts into operating-license events.