France Won the Capital Race. The Grid Decides the Rest.

RTE connection queue, deliverable versus announced capacity, nuclear cost advantage, Hauts-de-France corridor, SoftBank and Brookfield exposure

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

The signal in France is not the €93 billion announced at the June 2026 Choose France summit.

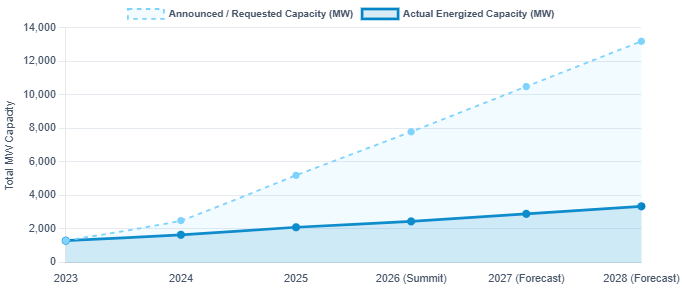

The real signal is the 11 GW of data center capacity sitting in RTE’s connection queue, against a transmission network where unrestricted connection capacity is already close to exhaustion.

Mainstream coverage interpreted the summit as France securing a lead in the European AI infrastructure race.

A more precise reading is that France has now committed more capacity than its grid can energize on the timelines investors are underwriting.

The widening gap between announced megawatts and deliverable megawatts is where capital will be made or lost over the next 24 months.

Power Access Is the Moat, Not the Headline Capital

France’s structural advantage is real and often misread.

The advantage is not the capital flowing into the market, but the electricity underpinning it.

Nuclear power provides more than two-thirds of French generation, with low-carbon sources accounting for roughly 95% of the total mix.

Grid carbon intensity sits at about 42 gCO₂e/kWh, compared to a global average of 472.

Electricity in France costs roughly one-sixth of Germany’s, creating a rare combination of low operating cost and low Scope 2 emissions for always-on AI compute.

The market is pricing the capital commitments, but it is underpricing the underlying driver that makes those commitments rational: cheap, low-carbon baseload power at scale.

Baseload matters because data center demand is highly stable, varying by only about 5% intraday.

France’s flat nuclear output matches that load profile, a pairing no other FLAP market can consistently replicate.

The Grid Connection Is the Constraint the Capital Cannot Buy Past

Power generation is not power access. This is the read the announced-capital coverage misses.

France generates abundant low-carbon electricity, but the transmission system that connects a data center to that electricity is the binding constraint, and capital does not clear it.

RTE’s unrestricted connection capacity is nearly exhausted. Connection lead times extend in some cases to a decade.

From 1 August 2025 the regulatory framework changed: RTE gained authority to reduce allocated capacity where actual usage falls below agreed levels, which imposes new dispatch and utilization obligations on developers who previously treated an allocation as a fixed asset.

The result is a two- to five-year lag between announcement and energization that no amount of committed capital compresses.

The 11 GW queue is not a measure of demand strength. It is a measure of the bottleneck. Every megawatt in that queue is a megawatt not yet earning.

Power Secured at Commitment Separates the De-Risked From the Merchant

The deals that matter structurally are the ones that solved the grid problem before announcement, not after.

SoftBank’s Dunkirk program embeds EDF as a direct partner for the Bouchain site, with power purchase and connection negotiated at the investment-commitment stage.

The MGX-Bpifrance-Mistral-NVIDIA Paris campus is structured with RTE as a direct partner.

These projects are de-risked on the one variable that cannot be bought in the open market.

Set them against the precedent the report carries: Amazon abandoned a French self-build after failing to secure local support.

The differentiator across the entire pipeline is no longer capital, land, or demand.

It is whether the developer holds a secured connection.

Operators with confirmed RTE agreements hold a durable advantage that compounds as the queue lengthens.

Merchant developers holding headline commitments and no connection hold a liability dressed as a pipeline.

Investor Action

Private Capital. Underwriting French data center exposure should focus on grid connection, not project commitments. The key test is whether RTE or EDF capacity is secured and at what allocation, as the 1 August 2025 rule adds utilization risk even to allocated power.

Favor operators with confirmed connections like Digital Realty, Data4, and RTE-partnered campuses, and discount MW pipelines without verified grid access to deliverable capacity.

The cost of inaction is underwriting announced capacity at announced timelines and discovering the two-to-five-year energization lag after the capital is committed.

Public Markets. Public equity and credit investors holding the named actors Brookfield, SoftBank, the listed operators, EDF, Schneider Electric should benchmark exposure against deliverable capacity, not announced capacity.

The structural winners are the grid-adjacent names: EDF as the power counterparty embedded in the largest programs, Schneider Electric as the supply-chain partner SoftBank localized in Dunkirk to defeat the equipment bottleneck.

The cost of waiting is that the deliverable-versus-announced repricing is not yet in consensus estimates. It will be once the first announced timelines slip.

Operators. Developers and hyperscalers acting as buyers should sequence French entry around connection availability, which points to Hauts-de-France over Paris for new hyperscale.

The northern corridor combines brownfield industrial land, RTE pre-qualified connection zones, and government fast-track permitting. Paris remains the enterprise and colocation market but offers less new connection headroom.

The cost of inaction is competing for the same exhausted Paris-region capacity that is already forcing pre-leasing before construction completion.

The Verdict

France has won the capital race and has not yet won the energization race, and the second race is the one that determines returns.

The market inflection is the point at which announced timelines begin to slip against grid reality, which the connection queue and the RTE rule change place inside the next 24 months.

Investors who treat secured grid connection as the primary underwriting variable will price French assets correctly. Those who instead anchor on capital commitments risk overpaying for megawatts without a viable path to energization.

The open question is which announced projects hold real connections and which hold press releases, and the report does not answer it for every name.

That disaggregation is the work, and it is the work that separates deliverable return from stranded commitment.