Fragmentation Is the Fiber Bottleneck Your Underwriting Model Misses

Geopolitical route risk, hyperscaler capacity withdrawal, regulatory divergence, insurance gaps, open-market scarcity, and the redundancy discipline that protects IRR

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Cross-border fragmentation now sets the ceiling on returns for global fiber, and most capital still underwrites the asset as if borders were neutral.

The old paradigm treated subsea and terrestrial cable as a defensive utility: stable demand, light regulation, low correlation to geopolitics.

That assumption is now the single most expensive error in the asset class.

The Bottleneck Moved to the Statute Book

The shift is structural, not cyclical.

Subsea cable carries the overwhelming majority of intercontinental traffic and clears trillions of dollars in transactions daily, so the routing of that infrastructure has become an instrument of statecraft.

The US-China rivalry has cleaved the supplier market into competing blocs. Regulators on both sides delay, deny, and reroute.

The question for capital is no longer where demand is growing.

The question is which routes will still be legal, insurable, and commercially open when the asset energizes.

One Route, Many Regulators

Start with how the constraint actually works.

A fiber route is not one asset. It is a chain of permits, landing rights, vendor approvals, and maintenance agreements, each governed by a different jurisdiction.

Every border the route crosses introduces a new regime that can veto, delay, or reverse the others.

AI-grade demand intensifies this because the highest-value routes are also the most contested corridors.

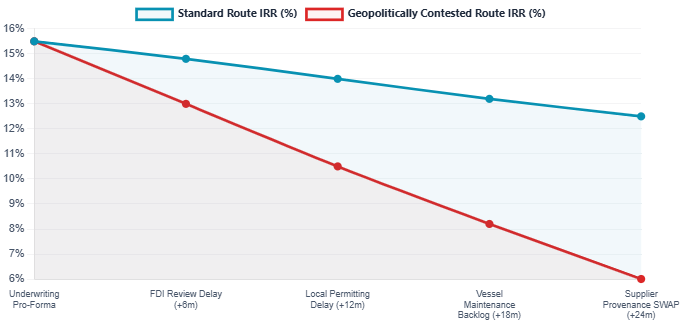

Consider a transpacific system that secured demand and financing, then lost two years to permitting friction across a single intermediate jurisdiction and a national-security landing review.

The capital was committed, but the revenue never arrived.

The IRR was set by the slowest regulator on the route, not by the strength of the offtake.

Engineering Risk Was Never the Real Risk

The industry has long assumed that fiber risk is engineering risk: lay the cable, qualify the route, collect the toll.

That assumption held when the network was governed by commercial peering and a broadly open permitting environment.

It does not hold now because the binding variable has moved from the seabed to the statute book.

A perfectly engineered route through a contested exclusive economic zone is a stranded asset if the landing license is denied.

Underwriting that prices construction risk while ignoring jurisdictional risk is mispricing the asset.

Time Is the Cost That Kills the Return

The supply side compounds the problem, and time is the cost that matters more than capital.

Cross-border projects carry longer lead times and higher overruns than domestic builds because each government approval is a serial dependency.

Right-of-way acquisition alone drives a large share of project delay in some markets.

The repair layer is thinner than the market assumes: a constrained global cable-ship fleet means a single cut in a contested corridor can suspend revenue for months, not days.

Insurance is contracting at the same moment exposure is widening, with some political-risk providers now excluding politically motivated sabotage entirely.

The investor without a contingency plan is watching risk-adjusted returns fall below hurdle through no failure of the underlying demand thesis.

Three Lenses, One Binding Variable

For the independent operator, the binding constraint is vendor and landing-station provenance. The qualification problem is no longer technical. It is whether the chosen supplier and landing partner will clear the regulatory screens in every jurisdiction the route touches, because one disallowed vendor can void approvals across the entire system.

For private equity and infrastructure investors, the decisive variable is schedule risk priced into the IRR. A route through contested water now demands a higher hurdle rate, scenario-based downside models, and explicit assumptions on rerouting cost, insurance gaps, and policy-reversal probability.

The deal that models bandwidth and demand but omits disruption timelines is underwriting a different, more optimistic asset than the one it is buying.

For public equity, the dispersion is between positioned and exposed cable holders. Capital is flowing overwhelmingly into hyperscaler-owned systems. Hyperscalers now hold stakes in dozens of operational cables, and a single one of them had more than thirty projects in or approaching service late in 2025.

As that capacity is built for private use, it withdraws from the open market. Several transatlantic systems approach retirement while new transatlantic investment is almost entirely hyperscaler-led.

The result is a capacity premium for independent buyers and an accelerated-obsolescence risk for legacy systems on routes a hyperscaler cable is about to overbuild.

The market has not fully repriced the legacy holders that lack contractual protection against route substitution.

Five Rules That Separate Resilient Capital

Translate this into discipline. Five rules separate resilient capital from exposed capital.

First, re-order your site and route filters. Jurisdictional and geopolitical screening moves to the front of the funnel, ahead of demand modeling. A route that fails the legal screen never reaches the financial model.

Second, model schedule and availability risk explicitly. Price the delay distribution, the rerouting scenario, and the repair-vessel wait as line items, not footnotes. Time-to-service is the dominant driver of fiber IRR, so underwrite it directly.

Third, secure access ahead of the market through long-term structure. Long-dated IRU agreements with creditworthy counterparties, with CPI escalators and regulatory cost pass-throughs written in, convert compliance cost into a recoverable expense rather than a margin leak.

Fourth, build redundancy into the asset itself. Diverse landing points, mixed submarine-terrestrial paths, and a satellite continuity hedge for high-value corridors reduce single-corridor exposure. Route diversity is an investment imperative, not an engineering preference.

Fifth, treat government relationship capital as an underwritable moat. Sustained access to permitting authorities and security reviewers buys early warning on policy shifts and faster approval timelines. In fragmented markets, that intelligence is a direct input to allocation timing.

You Are Underwriting the Map, Not the Cable

You are no longer underwriting a cable. You are underwriting a route through a contested regulatory map.

The engineering is the easy part now, and the market still prices it as if it were the hard part.

The discipline that wins screens the map first. It prices jurisdiction, delay, and repair wait before demand, then secures the route through long-dated structure.

That is not risk mitigation. That is the return.

The investors who move now own the resilient routes at today’s basis. The ones who wait will pay 2030 prices for decisions that belonged in 2026.