Does Eaton’s $9.5B Thermal Push Signal the Next $1 Trillion Buildout in the US AI Data Center Market?

A breakdown of how Eaton’s $9.5B thermal pivot reshapes power, cooling, and deployment strategy across the US AI buildout.

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Eaton’s $9.5B acquisition of Boyd Thermal signals that power management alone no longer suffices in the AI data center era.

The company is buying the one constraint hyperscalers cannot bypass: chip-level heat, with the 22.5× EBITDA price justified only if liquid cooling becomes mandatory and integrated electrical-thermal platforms win.

The deal positions Eaton as more than a traditional power vendor. It makes the company an energy-density gatekeeper.

With its “chip-to-grid” strategy, Eaton aims to control everything from the campus substation to the cold plates on each GPU, spanning 50 MW to 1 GW AI facilities.

The Hard Economics of the Deal

Boyd Thermal’s 2026 revenue is forecast at $1.7B, with $1.5B from liquid cooling, making it essentially a pure-play AI thermal platform.

The premium valuation reflects the scarcity of hyperscaler-qualified, scaled liquid cooling manufacturers and Boyd’s durable installed base across North America, Europe, and Asia.

Eaton expects earnings accretion in year two, paying a high multiple now to position its portfolio for the faster structural growth of AI infrastructure versus traditional electrical equipment.

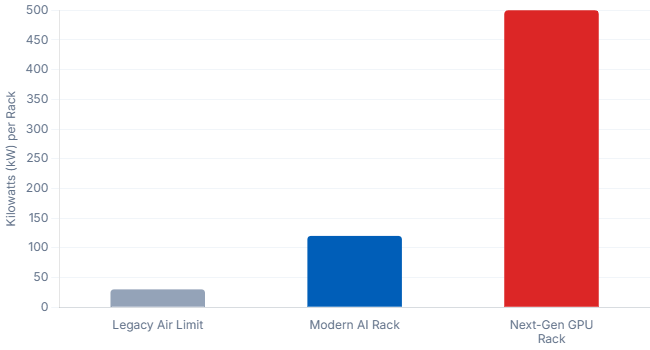

Why Liquid Cooling Is Not Optional Anymore

AI has pushed rack densities beyond the limits of air cooling. Traditional air-cooled racks plateau around 20–30 kW, while modern AI racks reach 80–120 kW and next-gen GPUs push 300–500 kW.

No airflow system can handle this heat without high energy use, noise, vibration, and reduced PUE. Physics makes liquid cooling mandatory, not optional.

Liquid cooling is currently a mid-single-digit-billion-dollar market, growing 20–30% annually toward 2030.

Most deployments serve hyperscale AI facilities, making liquid cooling a base-case requirement for any realistic AI infrastructure model.

Boyd’s Practical Value

Boyd is one of the few suppliers able to produce high-volume, leak-free, hyperscaler-qualified direct-to-chip cold plates, manifolds, loops, and Coolant Distribution Units that manage heat from chip to row or hall scale.

This is advanced thermal engineering, not HVAC, focused at the GPU and CPU package level where performance and uptime are defined.

Manufacturing at hyperscale tolerances is a rare metallurgical and process-control capability, and Boyd’s installed base of millions of plates is a strategic moat Eaton could not replicate quickly.

Eaton’s Chip-to-Grid Stack Comes Into Focus

Eaton already controls the electrical backbone of data centers, providing switchgear, transformers, UPS systems, PDUs, busway, and pre-integrated power blocks that accelerate deployment. Acquisitions like Fibrebond expand its modularization capabilities, compressing timelines further.

With Boyd, Eaton now also captures the thermal chain, connecting GPU cold plates to facility loops with the same level of engineering and system control it brings to power distribution.

This end-to-end control unifies the energy equation: every watt delivered to the chip becomes a watt that must be removed. Eaton’s thesis is that owning both ends creates a coordinated system advantage unmatched by standalone electrical or cooling vendors.

The Capital-Formation Lens

AI infrastructure is shifting from cash-funded modest builds to hyperscalers using record debt for industrial-scale campuses, renewables, and transmission, rewarding vendors who can de-risk deployment and deliver standardized capacity quickly.

Investors now favor power and cooling platforms as proxies to gain AI exposure without chip-level cyclicality. Eaton’s acquisition reflects a broader trend of industrial strategics repositioning as AI enablers, alongside Vertiv, Schneider, Modine, and nVent.

The deal positions Eaton within the asset class that LPs, infra funds, and sovereigns are targeting: critical components of 50–500 MW AI campuses with repeatable capex, defensible roadmaps, and high attach-rate visibility.

The Risk Profile That Investors Must Underwrite

Eaton faces a heavy integration burden, managing global plants, diverse customers, and hyperscaler-quality standards, with leak-free manufacturing as a key operational risk.

Technology risk is real: direct-to-chip liquid cooling dominates, but immersion and two-phase approaches are emerging, requiring Boyd to stay on the winning roadmap.

Customer concentration and valuation risks are central, as AI thermal designs shift with each GPU cycle and the 22.5× EBITDA price assumes high growth and smooth integration.

Policy and supply-chain constraints will shape Eaton’s footprint, requiring careful capex sequencing across regions while meeting redundancy, local manufacturing, and regulatory requirements.

Vendor Strategy Shift

The industry is shifting to integrated power-and-cooling blocks. Vertiv, Schneider, and Modine are consolidating or expanding thermal capabilities, while smaller specialists must partner or be acquired.

Developers are favoring pre-engineered AI blocks with guaranteed thermal and electrical performance, cutting complexity and deployment risk.

For investors, value lies with the few OEMs controlling both sides of the energy equation, making vendor ecosystem stability critical for underwriting AI infrastructure.

Key Signals Next 24–48 Months

The signals to watch are clear. Eaton must integrate Boyd into modular, factory-built AI infrastructure, with hyperscaler standardization across multiple campuses as the strongest proof of advantage.

Boyd’s roadmap versus immersion and two-phase cooling will show whether Eaton’s bet stays structurally right.

Manufacturing choices where new cold-plate lines go and how production is split across the US, Europe, India, and Asia will reveal Eaton’s strategy for meeting hyperscaler demand under geopolitical constraints.

Competitor moves, from further consolidation to OEM–hyperscaler design partnerships, will define the next wave of industry realignment.

Strategic Takeaways

Thermal management is now a primary driver of site selection, power planning, and the economics of AI campuses. Power without thermal headroom becomes stranded capex, and cooling without electrical integration creates inefficiency and delays.

Eaton’s acquisition of Boyd marks a shift in the AI buildout: the next decade will be defined by companies that control the interfaces where energy enters the campus and where it leaves the chip.

Investors, developers, and policymakers must treat thermal-power integration as a core diligence factor, because the owners of these interfaces will shape the economics of AI infrastructure.