Did U.S. Data Center Leasing Surpass All of 2024 in a Single Quarter?

A record 7.4 GW was leased in Q3 2025 revealing how AI demand, power scarcity, and trillion-dollar capital flows are reshaping U.S. infrastructure.

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Something historic happened in Q3 2025.

U.S. hyperscalers leased 7.4 gigawatts (GW) of data center capacity, more than the entire 7 GW leased in all of 2024.

That single quarter didn’t just set a record.

It redefined how capital, power, and compute now flow through the U.S. economy.

Analysts at TD Cowen call it “The Great Acceleration.” And they’re right.

The story isn’t just about how much space was leased.

It’s about what those leases signal: that the AI buildout has outgrown real estate and become an energy-linked infrastructure cycle unlike anything in modern history.

Oracle’s 5.4 GW Shockwave

The quarter’s surge was driven largely by Oracle’s 5.4 GW lease, the biggest single hyperscale deal ever recorded.

Almost all of it supports OpenAI’s Stargate initiative, a $30 billion-a-year partnership to build AI-optimized data centers across Texas, New Mexico, Wisconsin, and Missouri.

For Oracle, it was a strategic leap. Instead of competing head-to-head with hyperscalers for cloud market share, the company locked in decades of infrastructure revenue by becoming the landlord of AI compute.

For investors, it revealed a new asset class forming in real time long-duration, power-backed digital infrastructure contracts that behave more like utility offtakes than traditional tech leases.

When Leasing Becomes Infrastructure Finance

Leasing 7.4 GW in one quarter would have been unthinkable two years ago. But in 2025, hyperscalers are no longer renting space they’re pre-purchasing time-to-power.

Each contract now bundles land, substations, transformers, and cooling systems into a single deliverable: energized capacity, ready to host GPUs. These agreements are being securitized into asset-backed structures, allowing developers to raise cheaper capital against locked-in revenue streams.

In short, data center leasing has evolved into infrastructure debt. Power certainty now drives valuation more than location or tenant mix.

The Market Runs Out of Slack

Vacancy across North America fell to 2.3 percent, and in major markets like Northern Virginia, it’s below 1 percent.

Nearly nine out of ten megawatts under construction are already pre-leased, forcing enterprises to commit 18–24 months before delivery.

Developers are racing to add capacity 7.8 GW is currently under construction but grid connection delays stretch up to four years in many regions.

As a result, the first projects to energize enjoy scarcity pricing, with rental rates for 10 MW+ blocks climbing 15–20 percent year-on-year in primary markets.

Power Becomes the Gatekeeper

The constraint isn’t capital or land it’s electricity.

Interconnection queues now contain 1,570 GW of generation projects waiting to connect more than the total installed capacity of the U.S. grid. Data centers account for a growing share of that backlog, pushing operators to find alternatives.

By the end of 2024, 19% of U.S. data centers had already deployed some form of behind-the-meter (BTM) generation, from natural gas turbines to battery systems. Bain & Company expects a quarter of all new capacity by 2030 to rely on on-site or dedicated power.

This isn’t optional it’s survival. Without firm power, even a fully financed data center is just concrete and fiber.

The Geography of Scarcity

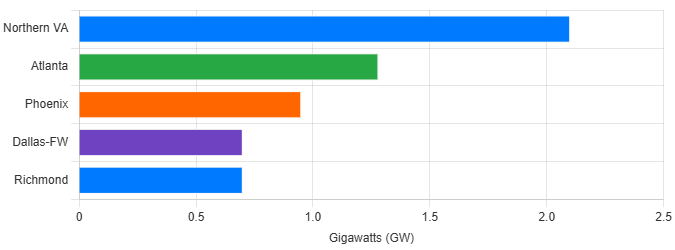

Northern Virginia remains the world’s largest data center market, with 5.6 GW of active capacity and another 5.9 GW planned. But growth is migrating toward Atlanta, Dallas–Fort Worth, Phoenix, and Richmond, where utilities can still allocate multi-hundred-megawatt blocks.

Atlanta tripled its inventory year-over-year to 1.28 GW, leading the country in net absorption. Richmond, once peripheral, jumped from 100 MW to over 800 MW in just six months as developers sought spillover capacity.

The pattern is clear: power-rich secondary markets are becoming the new Tier-1s. Site selection now starts with the substation map, not the fiber map.

The Trillion-Dollar Buildout Ahead

JLL projects that North America alone will require nearly $1 trillion in new data center investment between 2025 and 2030. McKinsey’s global model pushes that figure to $5.2 trillion, with the U.S. commanding about 40 percent of total spend.

Hyperscalers are leading the charge. Amazon, Microsoft, Google, Meta, and Oracle together will deploy more than $340 billion in capital expenditure in 2025 a 50 percent increase from last year.

Each dollar of capex cascades through a supply chain of transformers, turbines, chips, and cooling systems. For investors, the key metric isn’t server utilization it’s megawatts delivered per month.

Why This Quarter Changed Everything

The Q3 2025 numbers mark a structural break, not a one-off surge. AI workloads have turned compute into a hard-infrastructure asset tied directly to national power grids. Developers with firm interconnects are now as strategically valuable as energy producers.

Oracle’s 5.4 GW commitment showed that leasing can scale faster than construction, and that financing can precede physical capacity. For the first time, the data center sector operates on a pre-sold model, with future revenue already locked into long-term contracts.

What It Means for Each Player

Investors should view these leases as infrastructure bonds stable, yield-anchored, and backed by power rights. Expect a surge in securitized structures and private-credit vehicles funding hyperscale developments.

Operators must now control energy. Co-locating generation, negotiating directly with utilities, and upgrading to liquid cooling are competitive necessities, not optional upgrades.

Policymakers need to accelerate transmission build-outs and modernize permitting. Without grid reform, the AI buildout will stall behind power bottlenecks.

Tech buyers like the Oracles, Metas, and OpenAIs must navigate long lead times and local opposition. Securing multi-GW capacity has become a geopolitical act.

The New Definition of Scale

Q3 2025 confirmed what the past year foreshadowed: the AI era is measured in gigawatts, not gigabytes.

Leasing 7.4 GW in three months re-prices every assumption about growth, risk, and valuation in digital infrastructure. For decades, developers chased tenants. Now, tenants chase electrons.

The Great Acceleration isn’t a metaphor. It’s the moment data centers became the grid’s newest and hungriest sector.