Did Anthropic's $100B AWS Commitment Just Reset AI Infrastructure Capital?

Ten-year spend anchor, 5GW compute ceiling, Trainium2 through Trainium4 validation, Project Rainier multi-site expansion, hyperscaler anchor book competition, emerging market inference corridors

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Anthropic’s $100 billion pledge to spend on AWS over the next decade is the signal.

Amazon’s $33 billion equity commitment is the distraction.

The market fixates on the check but misses the contractual demand Anthropic agreed to deliver in return.

Capital allocators underwriting AI infrastructure on speculative demand will pay later for capacity already absorbed.

On April 20–21, 2026, Amazon and Anthropic announced the largest compute commitment in AI history: $5B in new equity, with up to $20B more tied to commercial milestones.

A $100 billion Anthropic commitment to AWS spend over ten years.

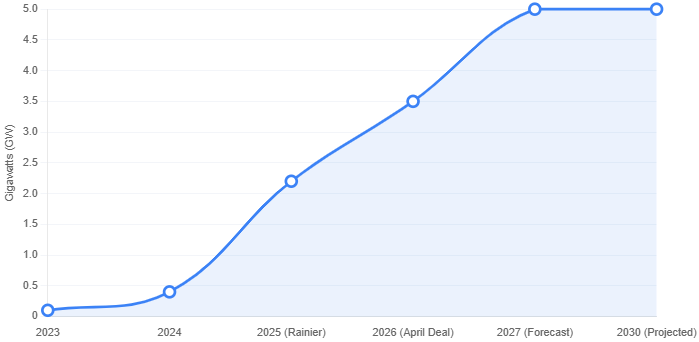

Up to 5 GW of compute capacity secured for Claude training and inference.

The question is not what Amazon bought.

The question is what Anthropic agreed to pay for.

That pricing commitment resets every underwriting assumption in the sector.

Project Rainier Was The Template

Amazon has been building toward this deal since 2023, deploying about $8B in staged equity through 2025.

Project Rainier reached full operation in mid-2025, with nearly 500,000 Trainium2 chips across U.S. data centers.

Claude workloads are already running at scale. The Indiana campus spans 1,200 acres across seven buildings, scaling toward 2.2 gigawatts.

The valuation structure is explicit.

Anthropic’s February 2026 round closed at $380B, while Amazon’s April 2026 investment came in at a $350B pre-money valuation below February levels and far under reported bids above $800B. The discount reflects secured long-term demand.

The April 2026 deal expands Project Rainier into a multi-site, decade-long buildout.

Trainium2 capacity ramps by Q2 2026, with nearly 1GW of Trainium2 and Trainium3 online by end-2026. Claude infrastructure also expands into Asia and Europe.

The stack includes Trainium2, Trainium3, Trainium4, future silicon, and tens of millions of Graviton CPUs.

Trainium4 is not yet commercial, and key chips are still in fabrication. Power, cooling, networking, and facilities remain forward-built infrastructure.

The 5GW figure is a contractual ceiling, not deployed capacity.

Anthropic’s annualized revenue moved from $1 billion to $5 billion during 2025, driven largely by enterprise Claude deployments on AWS.

AWS customers using Claude now exceed 100,000.

Anthropic Anchored AWS

The market has framed Amazon as the investor and Anthropic as the portfolio company.

That framing misses the structural inversion.

The capital reality runs the other way.

Anthropic is the anchor tenant. AWS is the landlord.

The anchor tenant is underwriting the buildout.

A $100 billion dollar contractual spend commitment over ten years functions as a co-investment in the infrastructure stack that defines competitive position through 2036.

That is a capital stack relationship and not a procurement relationship.

The economics map directly to class A real estate. The anchor signs first. The developer builds against the signed lease. Speculative capacity follows at pricing calibrated against the anchor rent.

What has changed is the identity of the anchor. A frontier AI lab now occupies the role retailers and law firms held in prior cycles.

Counterparty Access Now Binds The Sector

Independent operators face a qualification problem. Hyperscalers are building at a scale and tenor single-asset developers cannot match.

The five gigawatt multi-site commitment presumes contractual demand spanning a decade.

Operators competing on spec-built capacity without anchor tenant coverage will not be evaluated on AWS underwriting terms.

The specification question is concrete. An independent operator must secure a frontier lab, a hyperscaler, or a sovereign as an anchor before a site breaks ground.

Without that signature, the asset trades at a discount to hyperscaler-anchored comparables.

Power is solved. Land is solved. Capital is solved. Counterparty access is the remaining constraint.

Anchor Book Depth Replaces Model Performance

Private equity and infrastructure investors now face an underwriting question the sector has not resolved.

Anchor tenant models compress the return profile: lower risk, lower yield, longer duration.

The Anthropic-AWS structure resembles a triple-net lease with a ten-year term and chip-generation escalators.

For infrastructure funds targeting GDP-plus returns, this is attractive; for PE funds targeting mid-teens IRRs, it is structurally misaligned.

The key constraint is mandate fit.

Winning capital in AI infrastructure will increasingly resemble core infrastructure rather than opportunistic real estate. Funds that do not adapt will be priced out.

Public equity investors are seeing a parallel shift among hyperscalers.

Amazon’s ~$200B 2026 capex is largely AI-driven, with the Anthropic deal de-risking spend at a scale competitors struggle to match.

The comparison is sharp.

Microsoft and Nvidia committed $15B to Anthropic against $30B in Azure spend. Amazon committed up to $33B against $100B AWS spend. Google, despite early equity in Anthropic, has not structured a comparable anchor model.

The competitive question has moved. Model performance is a secondary question. Anchor book depth is the primary question.

Trainium silicon validation is a second-order consequence.

Claude training and inference at scale on Trainium strengthens AWS’s broader enterprise pitch against Nvidia pricing power. That is material upside layered on top of the anchor tenant structure.