Australia's Data Centers Just Pulled A$6B in One Week

NEXTDC hybrid raise, La Caisse commitment, Stockland Western Sydney campus, ESR equity injection, 2030 pipeline

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Australia is not approaching Tier 1 status as a global data center market.

It achieved it.

The institutional allocators still running a monitor-and-assess posture are not waiting for confirmation.

They are paying 2026 prices for decisions that should have been made in 2024.

In the week of April 7 to 14, 2026, three transactions landed inside five trading days:

NEXTDC raised A$1 billion in subordinated hybrid securities, backed by a binding commitment from La Caisse de dépôt et placement du Québec.

Stockland and Fife Capital filed for a 168 MW hyperscale campus in Western Sydney, with total investment approaching A$3.94 billion.

ESR raised US$850 million in new equity from existing shareholders to accelerate its APAC data center platform, naming Australia as a priority market alongside Japan and South Korea.

Over A$6 billion in committed capital directed at one national market in one week.

The question is not whether Australia is investable.

That question was resolved.

The question now is what risk tranche, what entry structure, and whether you have the platform relationships to access the deals that will not be publicly announced.

How the Position Was Built

The structural case for Australian data centers formed between 2021 and 2023, when hyperscaler demand began outrunning the available power and land supply in Singapore and Hong Kong.

Sydney emerged as the alternative.

An OECD-jurisdiction market with subsea cable connectivity to the US West Coast and Southeast Asia.

Available land in the western growth corridor. A federal government prepared to classify data centers as critical national infrastructure rather than planning liabilities.

By 2023, the principal operators had established their positions.

NEXTDC, CDC, Equinix, and AirTrunk built the operational foundation. Melbourne core sub-markets were running at approximately 97 percent pre-commitment.

Sydney’s western corridor was absorbing the hyperscale demand that Singapore’s land constraints had displaced.

The institutional product was taking shape.

Contracted cash flows.

Long-tenor tenants.

Government-backed grid coordination.

What followed was the capital formation phase, and the week of April 7 is its clearest single expression to date.

The Market Is Wrong

The dominant narrative has positioned Australia as a growth market with execution risk.

Abundant land. Supportive policy. Uncertain power delivery and cost escalation that limits institutional conviction.

That framing is structurally outdated by at least 18 months.

The narrative misses the demand-pull dynamic.

In January 2025, the US Bureau of Industry and Security implemented the AI Diffusion Rule.

Australia received Tier 1 designation.

Unrestricted access to Nvidia H100, H200, and Blackwell-class GPUs.

Singapore, India, and Malaysia were placed in Tier 2, subject to quotas and Total Processing Performance caps.

That regulatory asymmetry redirected AI cluster deployment toward Australia at exactly the moment hyperscalers were scaling their most compute-intensive workloads.

NEXTDC reported a 30% surge in its forward order book in 2025, driven by AI deployment wins that the Tier 2 market structure displaced from elsewhere in the region.

The capital reality is that institutions are not underwriting a speculative growth story.

They are underwriting contracted demand that has nowhere else in the region to go.

Three Investor Lenses

Independent operators face a qualification problem the market has not fully priced.

AI workloads require liquid-first thermal systems as rack densities approach 80 kW and exceed 135 kW in ultra-high-density setups.

Direct-to-chip cooling, immersion systems, and rear-door heat exchange are now baseline requirements.

Operators without the capital or technical capacity to certify AI-ready environments at scale cannot qualify for hyperscale or NeoCloud tenants.

The constraint is not land or power it is delivery capability at speed.

Private equity and infrastructure investors are underwriting a demand profile that is no longer traditional real estate.

Melbourne’s core markets are near 97% pre-commitment, and NEXTDC’s 297 MW forward order book runs through FY29, providing strong contracted visibility.

The key risk is execution labour, grid connection, and regulatory complexity in NSW. Capital is concentrating in scaled platforms for this reason.

The NEXTDC hybrid reflects this structure: subordinated, 100-year maturity, and outside senior covenants, matching long-duration infrastructure exposure with contracted demand confidence.

Public equity investors are seeing consolidation around a small number of dominant platforms.

NEXTDC’s A$5.2 billion pro-forma liquidity supports multi-year expansion through FY29, while smaller operators face capital constraints.

Stockland’s allocation and ESR’s equity raise reinforce the same trend.

Data center capacity is being treated as utility-scale infrastructure, and the capital required to compete is concentrating in fewer hands.

The window for pre-consolidation exposure is narrowing.

The 2030 Position

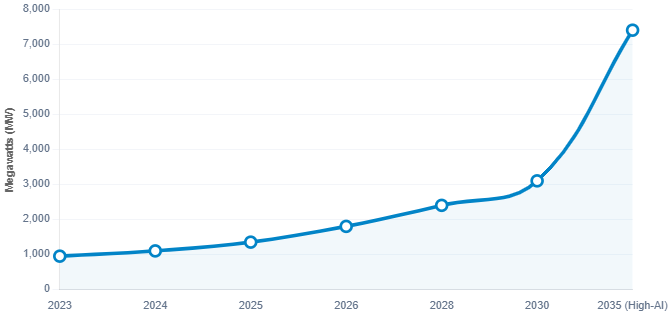

Australia’s deployable capacity stands at approximately 1,350 MW today, with consensus forecasts projecting 3,100 MW by 2030–2031 and 4.7 to 7.4 GW by 2035 under AI-driven scenarios, where data centers could consume up to 11 percent of national electricity.

NSW has endorsed 15 projects worth A$51.9 billion through its Investment Delivery Authority while rejecting about A$40 billions of proposals deemed speculative or underprepared.

This effectively turns infrastructure approval into partner selection, where grid coordination, planning support, and renewable integration flow only to qualified, capitalized operators rather than underprepared entrants regardless of stated capital.

The institutions that allocated in 2023 and 2024 are receiving contracted returns on assets that did not exist when they underwrote them.

The institutions moving now are entering a market where platform positions are established, pre-commitment rates are high, and deal structures are sophisticated enough to match the asset class profile.

The institutions that wait for further confirmation will find that the 2026 entry points were the last opportunity to price Australian digital infrastructure below its 2030 value.

The week of April 7 did not create this market. It confirmed what the capital had been indicating for two years.