The Hidden Risk Inside the Hyperscale Boom

A deep dive into the consolidation, pricing power, and policy pressures reshaping global hyperscale investing.

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

The Problem Hidden in the Boom

The dominant narrative in digital infrastructure is acceleration bigger campuses, denser racks, larger pre-leases, unprecedented capital commitments. Beneath that growth sits the sector’s most complicated structural problem: an extreme concentration of purchasing power in the hands of Amazon, Microsoft, Google, Meta, and Alibaba.

The research file shows these firms now command roughly 70% of global cloud infrastructure spending, with the five largest hyperscalers controlling about 60% of installed hyperscale megawatts worldwide.

That consolidation creates a market dynamic that is not merely competitive; it is gravitational. Hyperscalers now pull construction timelines, power allocation, land absorption, and pricing norms into their orbit. Where demand is surging, they benefit from scarcity. Where demand softens, they dictate terms. Investors are operating in a cycle where the strongest buyers set the rules and shift risk onto the capital providers building their infrastructure.

The challenge is not demand, demand is overwhelming. The challenge is the shape of that demand: large, concentrated, and structurally asymmetric.

The Causes: Why Power Converged So Quickly

1. The Scale Economics AI Created

AI is the single fastest accelerant of hyperscaler consolidation. According to the research file, AI-specific data center demand has been expanding at 100% annually since 2023, with GenAI cloud services jumping 140–180% year-over-year.

Training cycles for frontier models require thousands of accelerators operating continuously, pushing facility power densities far beyond enterprise norms. Hyperscalers are the only actors able to commit capital at the velocity and magnitude required. Between 2020 and 2024, they deployed more than $800 billion globally; between 2026 and 2030, projected spending exceeds $3 trillion, with almost $300 billion expected in 2025 alone.

AI did not merely increase demand. It rewired the competitive landscape by lifting the minimum viable scale of data center operations to a level only hyperscalers can reach.

2. Power Scarcity as an Entry Barrier

Infrastructure scarcity reinforced consolidation. Primary markets reached historic lows in available capacity. Research shows North America’s largest hubs fell to 1.6% vacancy in H1 2025, driven almost entirely by hyperscale pre-leasing.

Where grids are constrained Northern Virginia, Silicon Valley, Dublin utilities now prioritize the fastest, cleanest, most creditworthy load growth. Hyperscalers win those queues. Developers without long-term power commitments cannot compete for energized land at scale.

The scarcity of power didn’t just slow competitors. It advantaged hyperscalers that can secure multi-decade PPAs, negotiate directly with utilities, and self-finance on-site generation. The result is predictable: consolidation deepens.

3. Vertically Integrated Silicon and Procurement Pipelines

Data center capacity is no longer about real estate; it is about control of silicon supply chains. Hyperscalers purchase GPUs in quantities that saturate fabrication and packaging lines. They lock in long-term supply agreements with NVIDIA and other chipmakers that smaller operators cannot match.

This control over compute supply translates into pricing power over infrastructure providers. The uploaded research shows how hyperscalers’ bundled IaaS/PaaS/colo models allow them to price aggressively, push risk onto landlords, and enforce tight lease structures.

The Financial Impacts: Where Investors Feel the Squeeze

1. Revenue Concentration Risk

A small number of hyperscale customers can account for the majority of rental income across wholesale colocation platforms. Research from the file confirms that hyperscalers represent the largest revenue source for data center REITs, providing exceptional credit quality but severe concentration risk.

Credit quality is not the problem. Dependence is. When a single tenant occupies an entire building or campus, renewal becomes binary. A non-renewal event wipes out revenue at scale. Investors underwriting hyperscale-only portfolios are underwriting a cliff.

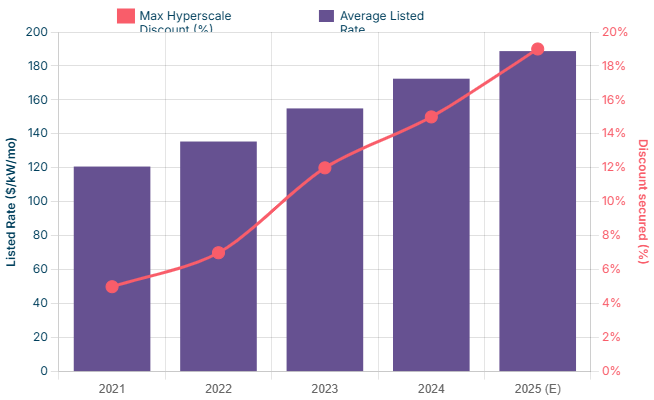

2. Asymmetric Lease Negotiations

Hyperscalers negotiate aggressively. The research file documents several shifts.

Rental rates increased from $120.76/kW/month in 2021 to $188.75 in 2025, yet hyperscalers secured double-digit MW deals with up to 19% discounts relative to listed pricing.

Hyperscalers have the leverage to demand longer free rent periods, stringent service levels, and operational control provisions. They increasingly negotiate 10–20-year terms with termination options or expansion rights that skew risk toward landlords.

3. Margin Compression from Utility Risk

Utilities across the US are raising capacity prices significantly. PJM’s auction cleared at $329/MW-day, a 22% increase, generating $16.1 billion in total procurement. The Independent Market Monitor linked this directly to data center load growth.

Where lease structures limit the landlord’s ability to pass through power cost increases which the research notes is common in hyperscale contracts margin erosion becomes unavoidable. Energy volatility becomes the landlord’s problem, not the tenant’s.

4. Structural Liquidity and Refinancing Risk

The research highlights a pattern of “roundabouting” interwoven equity stakes and cloud commitments across hyperscalers that creates systemic exposure for lenders. The asset-liability mismatch is clear: developers carry long-term debt; hyperscalers’ AI revenues remain unproven at industrial scale.

A slowdown in AI consumption or a pivot in model architecture could leave developers with stranded high-density assets requiring costly retrofits.

The Policy Responses: Governments React to Concentration

Regulators are no longer focusing solely on consumer pricing or cloud switching costs. They are increasingly targeting the infrastructure footprint behind cloud dominance.

1. Europe’s Digital Markets Act Investigations

The European Commission has opened multiple investigations to determine whether AWS and Azure should be classified as gatekeepers even if they do not meet standard DMA thresholds. The issue is not just cloud dominance; it is infrastructure dominance. Research shows US hyperscalers hold over 65% of the EU cloud market, while European providers have fallen to about 10%.

Europe now views infrastructure consolidation as a sovereignty problem.

2. US Scrutiny of AI Partnerships

The FTC issued compulsory orders to Alphabet, Amazon, Microsoft, Anthropic, and OpenAI. The concern is that hyperscaler–AI developer partnerships may entrench control over compute, data, and model training pipelines.

Investigators are examining whether exclusive access to accelerators and proprietary training environments creates structural barriers to competition.

3. Utility-Level Pushback

Utilities are attempting to shield ratepayers from the cost of hyperscale expansion. Some regulators are considering large-load tariffs or take-or-pay structures to force hyperscalers to internalize the cost of unfinished or abandoned infrastructure.

Hyperscalers are no longer just tenants. They are increasingly treated as quasi-industrial operators with system-level externalities.

The Investor Response: What the Smartest Capital Is Doing

Top investors are no longer treating hyperscale builds as real estate deals. They are treating them as capital-intensive infrastructure projects with energy exposure, technology risk, and sovereign-scale policy implications.

1. Diversification Across Demand Models

Leading funds separate hyperscale, wholesale colocation, and interconnection-centric assets into distinct risk buckets. Research notes that REITs with diversified tenant bases such as Equinix with more than 650 clients retain pricing power even as hyperscalers absorb more megawatts globally.

Wholesale-only portfolios are increasingly viewed as structurally brittle.

2. Power Control as the Primary Hedge

The most sophisticated platforms are shifting from “find land, get a PPA, build a shell” to “secure power first, build second.”

This includes long-term PPAs with inflation protection, on-site generation or microgrids, transmission-adjacent land banking, and direct utility partnerships. Operators with locked-in power capacity capture outsized pricing leverage in power-scarce markets.

3. Structured Joint Ventures to Share Exposure

Institutional money is pooling capital to manage hyperscaler risk. Research documents multi-billion-dollar JV structures BlackRock–Microsoft–NextEra, GIC–Equinix, and others that enable hyperscaler buildouts without concentrating debt risk on a single balance sheet.

These structures improve optionality. If a hyperscaler exits a market, ownership is diversified across entities better equipped to reposition the asset.

4. Design Specialization for AI Workloads

Smart capital is underwriting AI-ready design rather than retrofitting legacy colo stock. Operators now prioritize high-density cooling, optimized grey-to-white-space ratios, flexible electrical topologies, and GPU-ready thermal envelopes.

Research shows hyperscalers designing for rack densities far beyond enterprise standards, making retrofit-only strategies untenable.

5. Portfolio-Level Exposure Management

The most advanced investors treat hyperscale dependence as its own asset class. They model tenant concentration thresholds, renewal cliff exposures, power price sensitivity, GPU generation obsolescence timelines, and stranded megawatt probability.

In other words, they run hyperscale infrastructure the way energy funds run commodity exposure.

What This Means for the Next Five Years

The data shows hyperscaler consolidation is not cyclical; it is structural. Power scarcity, chip supply control, and AI-driven compute intensity will continue pulling the sector toward concentration.

However, that same scarcity is beginning to shift selective pricing power back to landlords if they control power, interconnection ecosystems, or strategically constrained land.

For investors, this is the core strategic truth:

The market is dominated by hyperscalers, but the leverage point has shifted from tenant relationships to resource control.

Those who own power win. Those who own interconnection win. Those who own single-tenant shells will increasingly rely on hyperscaler goodwill.

The boom will continue but only the investors who treat hyperscaler exposure as a systemic risk, not a trophy tenant, will keep real pricing power.