Amazon Q4 2025 Earnings: The $200B Infrastructure Mandate

Inside AWS Reacceleration, 4GW Capacity Expansion, and the Strategic Bet on Vertical AI Infrastructure

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Amazon’s fourth quarter paired solid operating results with rising capital intensity. Revenue reached $213.4 billion, up 14% year over year and above expectations. Operating income was $25.0 billion, or roughly $27.4 billion excluding one-time charges, implying an underlying margin in the high-12% range versus the reported 11.7%.

Net income rose 6% to $21.2 billion, and diluted EPS of $1.95 was effectively in line with consensus. The more consequential development was embedded in cash flow and forward capital guidance rather than the marginal earnings variance.

Trailing twelve-month operating cash flow increased 20% to $139.5 billion, but free cash flow fell to $11.2 billion from $38.2 billion due to heavy investment. Amazon deployed $131.8 billion in capex in 2025 and guided to approximately $200 billion for 2026, a 53% increase that materially shifts its financial profile toward sustained infrastructure-scale capital deployment.

AWS Reacceleration at Gigascale

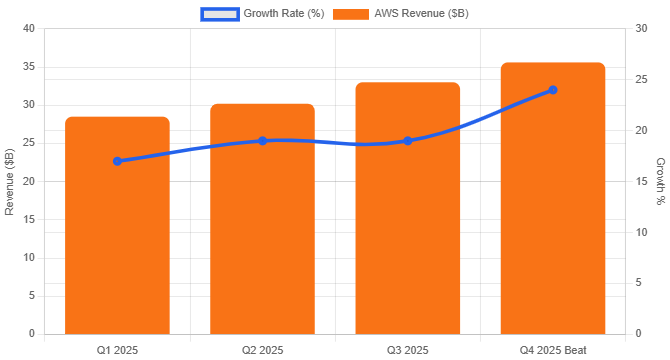

AWS delivered $35.6 billion in Q4 revenue, up 24% year over year and above consensus estimates around $34.9 billion. Operating income reached $12.5 billion, exceeding expectations and producing a 35% operating margin. On an annualized basis, AWS is now a $142 billion revenue run-rate business.

The scale matters. A 24% growth rate on a $142 billion base implies roughly $34 billion in incremental annual revenue if sustained. In the quarter alone, AWS added $2.6 billion of sequential revenue, its strongest growth cadence in nearly three years. This is not a stabilization story; it is a reacceleration story.

Backlog provides further evidence. AWS disclosed backlog near $200 billion, growing materially faster than reported revenue. That backlog represents multi-year contractual commitments from enterprises and AI-native firms, and it effectively underwrites the 2026 infrastructure buildout.

Custom Silicon and Vertical Integration

Amazon’s AI strategy is centered on vertical integration. Its Graviton and Trainium silicon families now exceed a $10 billion annualized revenue run rate, with triple-digit growth in AI accelerators. The company has deployed 1.4 million Trainium2 chips, including more than 500,000 in Anthropic’s “Project Rainier,” forming what it describes as the largest operational AI cluster built on proprietary silicon.

The strategic implication is margin control. If Amazon delivers 30–40% better price-performance versus merchant silicon, it captures more economics internally while reducing reliance on Nvidia’s stack. That cost advantage also enables more aggressive pricing for enterprise AI workloads.

The differentiation is structural, not incremental. Amazon is engineering cost leadership at the silicon layer while expanding data center capacity at hyperscale, reshaping its long-term competitive position in AI infrastructure.

Data Center Capacity: From Megawatts to Gigawatts

Amazon added roughly 4 gigawatts of capacity in 2025 and plans to double that by 2027, placing it on a path toward a double-digit gigawatt footprint. Management stated AWS deployed more data center capacity than any other operator globally in 2025.

The constraint has shifted from capital to power. Grid interconnection delays in parts of Europe highlight that transmission access and energy procurement now set the upper bound on capacity expansion. In the AI cycle, land control and power availability increasingly determine revenue growth ceilings.

Retail: Margin Discipline and Frequency Density

The North America segment generated $127.1 billion in Q4 revenue, up 10% year over year, with operating margin expanding to 9.0% from 8.0% a year earlier. Worldwide paid units grew 12%, the highest quarterly growth rate of 2025. Delivery speeds reached record levels, with billions of items delivered same-day or next-day to Prime members.

Category mix is shifting in economically important ways. “Everyday Essentials” grew nearly twice as fast as other categories, and roughly one-third of total units sold now fall into this group. High-frequency purchases increase route density and improve last-mile economics. In effect, Amazon is converting fulfillment scale into incremental margin expansion.

International revenue reached $50.7 billion, up 17% reported and 11% constant currency. Operating margin of 2.1% remains modest, but it reflects strategic pricing investments and international expansion rather than structural weakness. Amazon is prioritizing long-term share capture over short-term international profitability.

Advertising: The High-Margin Counterweight

Advertising revenue reached $21.3 billion in Q4, up 22% year over year, contributing more than $12 billions of incremental revenue for the full year. Prime Video ads are now active in 16 countries, reaching an average ad-supported audience of roughly 315 million viewers globally.

Advertising is strategically important because it carries structurally higher margins than first-party retail and monetizes traffic Amazon already controls. As AI enhances targeting and creative efficiency, the segment strengthens the platform’s cash generation, helping offset the capital intensity of AWS and satellite expansion.

The $200 Billion CapEx Inflection

The central disclosure was Amazon’s 2026 capex guide of approximately $200 billion.

Spending has risen from about $83 billion in 2024 to $131.8 billion in 2025, and now to a planned $200 billion in 2026, a roughly 140% increase over three years.

Amazon is reinvesting nearly 90% of operating cash flow into infrastructure, well above typical peer reinvestment levels. The capital is concentrated in AI data centers, networking, custom silicon, robotics, and the Leo satellite constellation, with management indicating new capacity is being absorbed as quickly as it is deployed.

Shares fell roughly 8–10% after the announcement, reflecting concern over margin pressure and return timing. The issue is not demand, but the duration and capital efficiency of this investment cycle.

Amazon Leo and Infrastructure Convergence

Amazon Leo, the company’s low-earth orbit satellite network, adds a space-based connectivity layer to its cloud platform. More than 180 satellites have been launched, and regulatory milestones are driving an accelerated deployment schedule, with roughly $1 billion of incremental year-over-year Leo-related costs reflected in Q1 guidance.

Strategically, Leo links connectivity and compute. Enterprise-grade terminals delivering gigabit speeds extend AWS beyond terrestrial fiber limits, particularly in underserved markets, reinforcing Amazon’s evolution into a vertically integrated infrastructure platform spanning data centers, silicon, logistics, and satellite broadband.

Strategic Interpretation

Amazon is shifting from quarterly free cash flow optimization to long-term infrastructure control. AWS growth reaccelerated to 24%, confirming demand, while the $200 billion capex plan signals sustained margin compression in favor of strategic positioning.

If AI workloads continue moving into production at current rates, the 2025–2027 investment cycle supports durable cloud growth anchored in proprietary silicon advantages. If demand moderates or monetization lags deployment, free cash flow pressure will extend.

The core issue for 2026 is not deployment capacity, but whether the AI economy can absorb that capital at acceptable returns.