Amazon Q1 FY2026: The Silicon Pivot Behind $200B in Capex

How a $20B Chip Business, $364B AWS Backlog, and Collapsing Free Cash Flow Are Reframing AWS as an Industrial Infrastructure Platform

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

Amazon’s Q4 2025 disclosure of a ~$200 billion 2026 capex plan set the forward commitment.

Q1 FY2026, reported April 29, 2026, clarified the demand side and exposed a misread: custom silicon is now a standalone strategic asset, not just a cost lever.

Revenue reached $181.5 billion, up 17 percent year over year and above guidance.

Operating income rose 30 percent to $23.9 billion, with a 13.1 percent margin.

AWS grew 28 percent to $37.6 billion, its fastest pace in fifteen quarters. Net income was $30.3 billion, including a $16.8 billion non-cash gain from the Anthropic stake revaluation.

Excluding that, operating performance is clear. Capital allocation remains the open question.

AWS Reacceleration on a $150 Billion Base

The reacceleration matters in absolute terms, not relative ones. AWS runs at roughly $150 billion annually, with 28 percent growth adding over $34 billion. Google Cloud’s ~63 percent growth on a ~$20 billion base and Azure’s ~40 percent growth are smaller in absolute terms.

The question is not growth rate leadership, but whether AWS’s incremental scale compounds faster than competitors can close the silicon and integration gap.

The demand signal sits in remaining performance obligations. AWS RPO reached $364 billion, up 93 percent year over year, excluding a new $100 billion OpenAI commitment on top of an existing $38 billion contract.

Bedrock spend rose 170 percent quarter over quarter, with Q1 token volume exceeding all prior periods combined. AI services now exceed a $15 billion annualized run rate within three years.

Segment operating margin fell to 37.7 percent from 39.1 percent, a 140-basis-point decline reflecting early AI infrastructure depreciation. With capex at ~$200 billion levels, margins will absorb the lag between deployment and monetization.

The issue is not compression in 2026, but where margins stabilize once depreciation aligns with contracted revenue.

Custom Silicon as a Standalone Business

The underpriced disclosure is in silicon. Graviton, Trainium, Inferentia, and Nitro now run at ~$20 billion annually with triple-digit growth. At market pricing, management implies a ~$50 billion equivalent. It is imputed, not external revenue, but directionally places Amazon alongside Nvidia and AMD as a top-tier data center chip supplier.

Product progression supports the claim. Trainium2 is fully committed. Trainium3, shipping in early 2026 with 30–40 percent better performance, is nearly fully subscribed. Graviton5 on 3nm is used by 98 percent of the top 1,000 EC2 customers, delivering up to 40 percent better price-performance than x86. Each cycle displaces external silicon spend.

The vendor flip occurred in Q1. Meta, committing $115–$135 billion to AI infrastructure, signed a multi-billion-dollar deal to deploy tens of millions of Graviton5 cores. A direct competitor became a customer. Silicon shifts from captive cost lever to a horizontal supplier in a market still framed as a duopoly.

The financial impact is two-sided. Internally, Trainium reduces hardware spend, saving “tens of billions” in capex over time. Externally, third-party silicon carries margins closer to chip vendors than cloud services. As external share grows, silicon becomes margin-accretive rather than purely cost-saving.

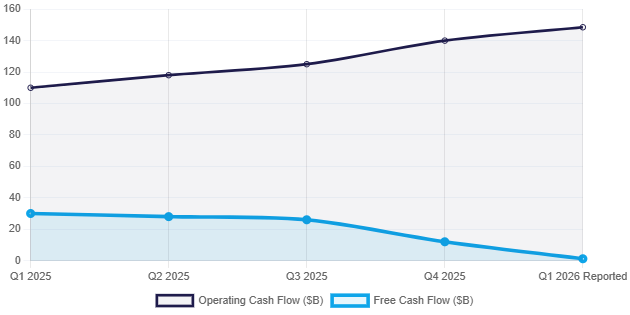

$200 Billion and the Free Cash Flow Collapse

Q1 capex was $44.2 billion, up 77 percent year over year, with a ~$200 billion 2026 plan focused on AI data centers, silicon, networking, robotics, and the Leo constellation. Assets are long-duration ~30 years for shells, five to six for servers with spend tied to contracted backlog, not speculative build.

The cash impact is severe. Trailing free cash flow fell to $1.2 billion from $25.9 billion, a 95 percent drop. Operating cash flow rose 30 percent to $148.5 billion, but nearly all incremental cash is being reinvested. Amazon has shifted from free-cash-flow optimization to infrastructure control.

The market reaction was muted, with shares up ~0.8 percent. Investors are discounting the Anthropic mark, accepting operating leverage, and reserving judgment on capital efficiency. The lack of repricing despite a 95 percent FCF collapse reflects confidence in contracted demand visibility.

Backlog Concentration and Counterparty Quality

The backlog quality question is real. AWS RPO at $364 billion provides visibility but is concentrated among a few frontier labs. The OpenAI extension $100 billion over eight years on top of $38 billion and up to $25 billion of additional investment in Anthropic deepen commercial dependency, alongside equity-linked earnings.

This creates two risks. First, counterparty quality: model labs are capital-intensive and loss-making, reliant on continued financing to honor contracts. Second, equity mechanics: mark-to-market gains tie earnings to private AI valuations, themselves linked to cloud capex sentiment. A retracement would reverse the $16.8 billion Q1 gain and pressure backlog conversion.

The structural risk is not that any single contract fails. It is that the AI infrastructure financing flywheel hyperscalers funding model labs, model labs committing to multi-year cloud contracts, mark-to-market gains supporting reported earnings depends on private-market liquidity remaining accommodative across the build cycle.

Amazon Leo and the Connectivity Stack

Amazon Leo, the low-earth-orbit constellation formerly Project Kuiper, advanced in Q1 with ~302 satellites in orbit and commercial launch targeted for mid-2026. The strategy is to extend AWS connectivity beyond terrestrial fiber into underserved markets and direct-to-device use cases.

Two moves reset positioning. Amazon agreed to acquire Globalstar for $11.6 billion, securing mobile spectrum and D2D rights. It also partnered with Apple to power satellite features on iPhone and Apple Watch, including Emergency SOS, anchoring a flagship D2D customer.

Execution risk is regulatory. The Federal Communications Commission requires 1,618 satellites by July 30, 2026; current deployment is well below. Amazon has requested a two-year extension and secured 100+ launches via United Launch Alliance, Arianespace, SpaceX, and Blue Origin.

Approval is likely but not assured; denial would affect spectrum rights tied to the Apple agreement. Costs are rising, with ~$1 billion of incremental Q2 spend guided for the constellation.

The Hyperscaler Frame

The competitive landscape is no longer converging on growth rates but fragmenting by workload type, silicon stack, and integration depth. Google Cloud’s 63 percent growth and ~$462 billion backlog reflect AI-native workload capture.

Azure’s 40 percent growth reflects enterprise AI adoption via Microsoft’s distribution. AWS’s 28 percent growth on a $150 billion base reflects scale-driven execution at industrial cadence.

The combined 2026 AI infrastructure capex across Amazon, Microsoft, Alphabet, and Meta is now estimated near $725 billion, up from ~$650 billion. The cost of remaining a top-tier AI platform has reset higher, narrowing the field of viable players.

Power access, advanced packaging, and grid interconnection timelines are now the binding constraints across all four.

Strategic Forecast

The next two earnings cycles test three variables.

First, whether silicon sustains momentum as third-party demand scales, measured by Trainium3 deployment, hyperscaler customer wins like Meta, and evidence of external pricing power.

Second, whether free cash flow stabilizes as capex compounds, requiring operating cash flow growth to outpace depreciation.

Third, whether Leo meets Federal Communications Commission milestones or runs under extension, shaping spectrum certainty for the Apple partnership and the connectivity layer.

The forward signal is not AWS growth but the external share of silicon revenue. If the implied $50 billion converts to real third-party revenue at chip-like margins, Amazon establishes a defining vertical-integration position. If silicon remains captive, the outcome is cost leverage, not category redefinition.

Power, packaging, and grid interconnection remain binding constraints. Demand is funded and contracted. Execution determines the outcomehow quickly Amazon can energize, deploy, and monetize capacity built over the past