Alphabet Chose Dilution Over Debt, And That Is The Signal

Equity over debt as conviction signal, Berkshire as validation not capital, power and land race, the slow-monetization risk

Welcome to Global Data Center Hub. Join investors, operators, and innovators reading to stay ahead of the latest trends in the data center sector in developed and emerging markets globally.

The Financing Choice Is The Signal, Not The Size

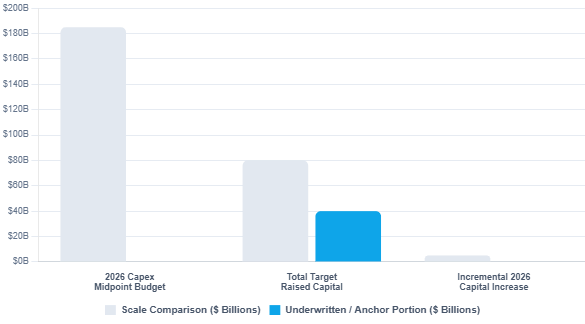

The number that matters in Alphabet’s $80 billion raise is not $80 billion.

It is the decision to fund it with equity.

A company sitting on one of the largest cash positions and strongest balance sheets in the world elected to dilute its shareholders rather than lever up to finance its AI infrastructure buildout.

The market read the headline as a capex story and discounted the stock on dilution.

The structural read is different.

Alphabet is signaling that the AI infrastructure cycle is large enough and long enough that it wants permanent capital against it, not refinanceable debt.

That choice tells you how Alphabet underwrites the duration and the risk of this cycle, and it should reset how every other allocator underwrites the same exposure.

Equity Funding Prices The Cycle As Structural, Not Cyclical

The first signal sits in the instrument selection.

Alphabet is layering equity on top of an earlier debt program that included very long-dated paper.

Management has stated the objective is to preserve balance sheet flexibility while still funding capex at the top of the hyperscaler range.

Read the choice through the lens of what equity costs versus what debt costs.

Debt is cheaper when you believe the asset will throw off contracted cash flow on a predictable schedule.

Equity is the instrument you choose when you want to absorb timing risk, obsolescence risk, and demand risk without a fixed repayment obligation hanging over the asset.

Alphabet is telling the market it is not certain enough about the timing of AI monetization to want hard debt service against it, but it is certain enough about the direction to commit permanent capital.

That is a structural bet financed with structural capital.

Over the next 12 to 24 months, expect peers to be benchmarked publicly on the same question.

Are they funding AI capex with instruments that match the risk profile of the asset, or are they borrowing against revenue that has not arrived?

The Berkshire Placement Is Validation, Not Capital

The second signal is the Berkshire Hathaway tranche and its function is not the $10 billion.

Berkshire deploying capital into a large-cap technology name at negotiated terms, priced slightly below market, is a public validation of Alphabet’s decision to finance capex through dilution.

Berkshire built its initial position in the third quarter of 2025 and chose to deepen it through a private placement rather than buying in the open market.

A negotiated private placement with a long-term anchor signals conviction in the duration of the thesis, not a trade.

For the market, this lowers the perceived governance risk of the equity strategy.

When the most patient large-cap capital in the world underwrites your dilution at negotiated terms, it becomes materially harder for other shareholders to argue the equity raise is a sign of distress rather than ambition.

Expect this to compress the dilution discount over the next several quarters as the validation is priced in.

Power And Land Are The Real Constraint The Capital Is Chasing

The third signal is what the capital is actually for, and it is not GPUs.

The binding constraint in this cycle is power and the contiguous land to site it.

Leading markets are already strained.

The competitive frontier has shifted to who can secure large, contiguous tranches of power and land in markets that can still accommodate them.

Alphabet’s equity war chest is a pre-commitment instrument.

It funds long-lead power procurement, grid upgrades, and large campus development before the demand is fully contracted.

Most new capacity in leading markets is pre-leased or self-developed before construction begins.

A larger pool of permanent capital lets Alphabet crowd out smaller buyers in constrained nodes and pre-commit to power that second-tier players cannot match.

The signal for the next 24 months is that capital access is converting directly into power access, and power access is converting into market position.

The allocators who treat this as a compute race are mispricing it.

It is a power and land race financed by capital markets.

Investor Action

Private equity, infrastructure funds, and family offices should reprice the cost of competing with hyperscaler capital in constrained power markets. The opportunity is to avoid direct competition in strained primary nodes and instead focus on secondary markets, alternative regions, and the power-development layer before hyperscaler capital arrives.

The cost of inaction is being outbid on every contiguous power tranche in primary markets by buyers with a structurally lower cost of capital.

Public equity investors should benchmark every hyperscaler on the match between financing instrument and asset risk, not on capex magnitude alone.

The action is to diligence whether peers are funding AI capex with equity, debt, or revenue that has not yet materialized, and to treat instrument selection as a leading indicator of management’s own confidence in monetization timing.

The cost of inaction is mistaking a dilution-driven price dip for a deterioration in fundamentals and selling into a validated structural commitment.

Data center developers and operators should read this as confirmation that hyperscaler self-development and pre-leasing will tighten further in constrained markets.

The action is to lock power and land positions in markets the hyperscalers have not yet saturated, and to structure offtake conversations before the largest buyers pre-commit the available capacity.

The cost of inaction is watching contiguous power get absorbed by self-developing hyperscalers and being left to compete for the fragments.

The Verdict

Alphabet’s raise is the moment the AI infrastructure cycle was publicly repriced as a structural asset class rather than a capex line item.

The instrument choice, equity over debt, says management is underwriting a multi-year buildout with permanent capital because the duration and the demand timing do not fit a fixed repayment schedule.

The Berkshire placement says the most patient capital in the world agrees. The use of proceeds says the contest will be won on power and land, not chips.

Market inflection is the normalization of ultra-high, equity-funded capex as the price of staying in the top tier.

The open question is the one Alphabet itself cannot fully answer.

If the monetization of AI in search and cloud arrives slower than the build curve assumes, does permanent capital protect Alphabet or simply lock in the loss?

The allocators who answer that question first will position correctly.

The ones who wait for the answer to be obvious will pay for it.

Berkshire has a nice 6% discount to where this priced. It's not Goldman, crisis era discount territory, for sure. I think the equity choice is also a reflection of where the stock is trading now. It is fun to see the corporate finance tool chest being brought to bear, though...instead of just cash!